Regulatory Landscape - Overview

Brachytherapy Regulatory Landscape: Product Overview

Brachytherapy, also known as internal radiation therapy, is a specialized form of radiation treatment for various cancers. This approach involves surgically placing radioactive seeds, capsules, or other implants inside or near a tumour, allowing for high doses of radiation to target the cancer while minimizing exposure to surrounding healthy tissue.

Centre for devices and radiological health (CDRH), division under U.S. food and drug administration (FDA) is responsible for regulation of brachytherapy related medical devices for ensuring safety and efficacy of the treatments to patients.

Brachytherapy treatments are of two types, it can be either temporary Brachytherapy or permanent Brachytherapy.

Temporary brachytherapy involves placing radioactive material inside a catheter for a specified duration, after which it is removed. It can be delivered as low-dose rate (LDR) therapy, providing lower intensity over a longer period, or high-dose rate (HDR) therapy, offering higher intensity in a shorter timeframe.

Permanent brachytherapy, also known as seed implantation, involves inserting radioactive seeds—about the size of a grain of rice—into or near the tumour for long-term treatment. Over several months, these seeds gradually lose their radioactivity. Occasionally, active seeds may trigger radiation detectors at security checkpoints. Inactive seeds are harmless and typically do not trigger metal detectors.

Based on Product, Brachytherapy has been segmented into After loaders & Applicators, Radioactive Seeds, Electronic Brachytherapy, Imaging Systems, and Others.

Radiotherapy material used in Brachytherapy:

The type of radioactive material used in brachytherapy—such as iodine, palladium, cesium, or iridium—depends on the treatment type, with all sources encapsulated in a non-radioactive "seed" to prevent migration. Permanent implants place these seeds directly into the tumour using ultrasound or x-ray imaging for accuracy. Temporary implants involve inserting radiation sources through needles, catheters, or applicators after confirming their position, a process called "after loading." This can be done manually or via a computer-controlled machine, with medical imaging ensuring effective placement and a computer calculating the necessary dose and duration.

Brachytherapy Administration Overview:

In permanent brachytherapy, needles pre-filled with radioactive seeds are inserted directly into the tumor. After placement, the doctor removes the needles, leaving the seeds behind. Alternatively, seeds can be implanted individually at regular intervals using a specialized device. Medical imaging is often employed to ensure accurate seed positioning, and additional imaging tests may be conducted later to verify their placement.

Temporary brachytherapy involves placing a delivery device, such as a catheter or needle, near or into the tumor, guided by medical imaging. This can be done intravaginally, intrauterinely, interstitially, or on the skin for surface tumors. High dose rate (HDR) treatments deliver radiation in 10 to 20-minute sessions, typically as an outpatient procedure, though some patients may stay in the hospital for one to two days for multiple treatments. HDR uses a remote after loading machine to store radioactive isotopes like Iridium-192, minimizing staff exposure. Low-dose rate (LDR) treatments provide continuous radiation over one to two days, requiring an overnight hospital stay. Pulsed dose-rate (PDR) treatments deliver radiation in periodic pulses, often hourly. After treatment, the delivery device is removed.

Afterloaders, which automate the placement of radioactive sources in brachytherapy, enhance treatment precision and patient safety, making them a preferred choice in clinical settings. Additionally, the demand for various applicators tailored for different types of cancer, such as prostate and cervical cancer, is rising as healthcare providers seek effective, localized treatment options. Key players are focusing on innovative product offerings and strategic partnerships to enhance their market presence. Varian has introduced the Bravos™ after loader system for high-dose-rate (HDR) brachytherapy. Bravos is an integrated system developed to simplify brachytherapy treatment, increase workflow efficiency, and improve the experience of patients and physicians.

Radioactive seeds, used primarily for prostate brachytherapy, allow for precise, localized treatment with minimal impact on surrounding tissues. Increasing awareness among healthcare providers and patients about the benefits of this minimally invasive approach is propelling market demand. Additionally, ongoing research and innovation in seed technology are enhancing treatment efficacy and safety. Isoray Inc., a national isotope-based medical company, has created Cs-131 seed, which has a shorter half-life and faster delivery of radiation dose compared to other seeds on the market. As the healthcare sector continues to focus on personalized medicine and improved cancer care solutions, the brachytherapy radioactive seeds market is expected to expand significantly, offering promising prospects for both manufacturers and patients alike.

Electronic brachytherapy has benefits such as improved safety profiles and reduced radiation exposure for both patients and healthcare personnel, which contributes to its increasing acceptance. Electronic brachytherapy is used to treat cancers of the breast, skin, keloids, spinal metastases, gastrointestinal, endometrial, cervix, and rectum. Because of their unique architecture, certain existing electronic brachytherapy devices, such as Esteya and Photoelectric Therapy, can only treat small skin cancers. Ongoing research, advancements in treatment delivery technologies, and increased knowledge of the benefits of localized radiation therapy all contribute to the market's growth. Furthermore, strategic alliances and investments in healthcare infrastructure are improving the accessibility and implementation of electronic brachytherapy solutions, preparing the market for sustained growth in the next years.

Imaging technologies are crucial for accurate tumor localization and dosimetry in brachytherapy procedures, ensuring optimal placement of radioactive sources. The rise in cancer cases, particularly in developing regions, is driving healthcare providers to adopt advanced imaging solutions for enhanced treatment outcomes. Moreover, innovations such as real-time imaging and integration with planning software are improving the efficiency and effectiveness of brachytherapy.

Brachytherapy treatment Product development

Under centre for devices and radiological health (CDRH) there is a office of product evaluation and quality (OPEQ) which is responsible for approval, manufacturing and quality control of medical devices including brachytherapy equipment’s. Under OPEQ there is subdivision of office of health technology 8 (OHT 8), which has office of radiological health, responsible for regulation of radiological devices, including brachytherapy products.

For product development in brachytherapy, manufacturers should consider following aspects:

Various submissions required as per the class of medical devices in which the manufactured product is falling, are as follows;

The regulatory control rate increases from class I of medical devices to class III. Every Regulatory class of medical devices comprises different regulatory controls. (i.e., general controls, special controls, and premarket approval [PMA]).

-

General controls are baseline requirements must be fulfilled by all classes of medical devices like class I, II, III, and it includes device registration and listing, labelling requirements, good manufacturing practices- quality system regulation (GMP-QSR), medical device reporting MDR.

-

Some devices need special controls which include labelling and post market studies. Device labels must include date of manufacturing, directions to use, intended use, place of business.

-

510(k) premarket notification, it is a premarket submission made to FDA to demonstrate that the device to be marketed is as safe and effective, that is, substantially equivalent, to a legally marketed device. Class II medical devices posing moderate risk, need to get this from FDA.

-

Premarket approval (PMA), all medical devices under class III, posing high risk, must get PMA from FDA. PMA gives enough valid scientific evidence which assure device safety and effectivity for its intended use. If device fails to fulfil PMA needs, it is considered to be adulterated under section 501(f) of the FD&C Act and not allowed to be marketed.

Some of the recent brachytherapy product launched are as follows;

-

In July 2024, HealthCare’s MIM software launched MIM Symphony HDR Prostate to support high dose-rate (HDR) brachytherapy. This innovative solution aims to increase clinician confidence and help improve patient outcomes by providing direct tumor visualization from magnetic resonance imaging (MRI) scans during live ultrasound procedures for HDR prostate treatments.

-

In June 2022, RaySearch Laboratories AB announced the launch of RayStation 12A, the latest version of the company’s advanced treatment planning system. RayStation 12A supports brachy planning for Elekta Flexitron afterloaders. The dedicated brachy planning module allows rapid creation of optimal and accurate high-dose rate brachytherapy treatment plans.

-

April 2020: Elekta launched the Geneva brachytherapy applicator, a groundbreaking instrument designed to improve the precision of gynaecological cancer treatment This innovative applicator utilizes Elekta’s “outside-in” approach, ensuring that its design meets the real-world clinical requirements of healthcare providers, thereby addressing specific challenges faced in gynaecological oncology.

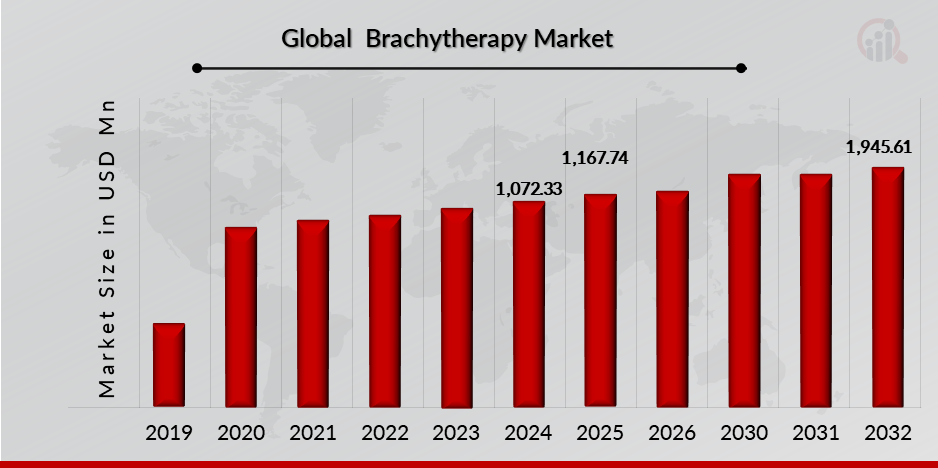

Brachytherapy Market Size Overview:

As per MRFR analysis, the Brachytherapy Market Size was estimated at 1,072.33 (USD Million) in 2024. The Brachytherapy Market Industry is expected to grow from 1,167.74 (USD Million) in 2025 to 1,945.61 (USD Million) till 2032, at a CAGR (growth rate) is expected to be around 6.84% during the forecast period (2024 - 2032). Introduction of brachytherapy services increasing incidences of cancer across the globe, increasing number of product launch, growing awareness among healthcare providers and patients about the benefits of brachytherapy are the key market drivers enhancing the growth of the market.

Source: The Secondary Research, Primary Research, MRFR Database and Analyst Review

Brachytherapy Regulatory Landscape:

There are several key regulatory agencies who oversee the approval and monitoring of Brachytherapy to ensure their safety, efficacy, and quality.

| Regulatory agencies | Regulatory Ministry |

| Federal Food and Drug Administration | United States: Department of Health and Human Services (HHS) |

| The Medicines and Healthcare products Regulatory Agency | United Kingdom: The Medicines and Healthcare products Regulatory Agency (MHRA) under the Department of Health and Social Care (DHSC) |

| Central Drug Standard Control Organization | India: The Ministry of Health and Family Welfare |

| Health Canada | Canada: The Ministry of Health |

| Pharmaceuticals and Medical Devices Agency (PMDA) | Japan: Ministry of Health, Labour and Welfare. |

| National Medical Products Administration (NMPA) | China: The Ministry of Health |

| Health Sciences Authority | Singapore: The Ministry of Health |

| European Medicine Agency | European union |

| Therapeutic Goods Administration (TGA) | Commonwealth of Australia |

Eligibility: Patients who have good general health with the ability to tolerate the treatment process can be administered with brachytherapy. Doctors suggest brachytherapy for small early-stage cancers, that have not spread to other body parts. It is suitable for patients suffering with localized cancers such as prostate, cervical, breast and skin cancers where precise radiation is required, has fewer side effects, and quicker recovery treatment options as compared to traditional treatment. Administration depends on the type of cancer the patient is having, whether he or she will be able to tolerate the treatment and possible side effects later and cost affordability of the treatment.

Patients in underserved areas often encounter delays in receiving timely and effective cancer treatment. Many are forced to travel long distances to reach specialized facilities that can offer brachytherapy, creating additional logistical and financial burdens. This scenario not only prolongs suffering but also raises the risk of disease progression for patients who cannot access necessary treatments promptly.

The financial strain associated with implementing and maintaining brachytherapy services can deter healthcare providers from adopting this crucial treatment modality. As a result, the range of available treatment options for patients who would benefit from this targeted and localized therapy becomes severely limited. Ultimately, the high costs of brachytherapy not only impede its availability but also exacerbate existing healthcare disparities in cancer care on a global scale, leaving vulnerable populations without access to vital, life-saving treatments.

Dosage: According to international commission on radiation units and measurements (ICRU 38), brachytherapy doses are divided into 3 classes. Low dose rate (LDR) where implants deliver dose at 0.4-2 Gy/h rate, for 24 to 144 hrs., but in routine clinical practice it is used at rate of 0.3 – 2 Gy/h. medium dose rate (MDR) is administered in range of 2 Gy/h to 12 Gy/h. high dose rate (HDR) at dose rate of 12 Gy/h or more, ending treatment time in minutes and administered in 4-6 fractions.

Classification of the Product:

Brachytherapy Regulatory Process Overview, By Country:

January 2024, U.S. Food and Drugs Administration (FDA) and U.S. Nuclear Regulatory Commission (NRC), has signed memorandum of understanding (MOU), they have agreed to collaborate and coordinate for regulatory decisions regarding;

-

Products using byproducts, sources, or special nuclear material

-

Products which can be impacted due to the release of byproduct, source, or special nuclear material.

This MOU gives framework for FDA and NRC collaboration and does not impact independence of FDA or NRC or either agency’s authority for fulfilling their responsibilities.

Code of federal regulation part 892 covers radiation therapy devices, including brachytherapy equipment’s safety and efficacy regulations under Centre for devices and radiological health (CDRH), division of U.S. food and drug administration (FDA).

FDA has issued guidance for premarket notification for photon emitting brachytherapy sources, according to the guidance brachytherapy sources are currently classified under class II, which require premarket notification (510(k).

A 510(k) is a premarket notification manufacturer needs to get from FDA to ensure the safety and efficacy of the device to be marketed, and is, substantially equivalent, to a legally marketed device. Submitters has to show comparison between their device and one or more similar legally marketed devices and make and support their substantial equivalence claims.

The currently used product code to identify these devices is KXK. As per the guidance, the principal components of brachytherapy sources are radioactive material, either absorbed or it is plated on substrate and encapsulation.

Brachytherapy Market trends

May 2024: GT Medical Technologies partnered with Theragenics Corporation (US) to enhance physician access to Cesium-131 seeds for brachytherapy, a vital form of internal radiotherapy. Under this agreement, Theragenics will serve as the exclusive distributor of Cesium-131 brachytherapy seeds and carriers, expanding their use beyond brain tumours to include treatments for other cancers, such as prostate cancer. Cesium-131 is a widely used isotope in low dose rate (LDR) brachytherapy, where tiny radioactive seeds are implanted directly into or adjacent to tumours. This method effectively delivers a concentrated dose of radiation to cancer cells while minimizing damage to surrounding healthy tissues, making it a favourable option for various cancer treatments. GT Medical Technologies acquired these Cesium 131 seeds through its purchase of Perspective Therapeutics' subsidiary, Isoray Medical, in December 2023.

January 2021: BEBIG Medical GmbH (Germany) significantly enhanced its position in the HDR brachytherapy market by acquiring the global production and distribution structures of Eckert & Ziegler BEBIG GmbH, including Mick Radio Nuclear Instruments, Inc. This move is part of a broader strategy to capitalize on the growing demand for effective cancer treatments. Additionally, Eckert & Ziegler AG has formed a joint venture with TCL Healthcare to develop advanced tumors irradiation devices specifically targeting gynaecological cancers and other forms of cancer. This collaboration aims to leverage the strengths of both companies, particularly in the rapidly expanding Chinese healthcare market, where approximately 4 million new cancer cases are reported annually.

Technology adoption overview:

July 2022, UC San Diego Health began offering the new brachytherapy treatment option. It is the first hospital to offer new, highly targeted and high precision radiation therapy which has shown to delay the tumor regrowth, even protecting healthy tissue in patients with brain cancer.

This novel GammaTile approach approved by FDA, uses small radiation seeds or brachytherapy, implanted at site of tumor at surgery time and it is naturally absorbed in body, treating malignant and recurrent brain tumors, including gliomas, glioblastomas and meningiomas.

Brachytherapy Regulatory challenges:

Compliance challenges due to complex nature, radiation risk and strict FDA and NRC regulatory requirements, will create issues in getting premarket notification which in turn will delay the approval process of new brachytherapy equipment’s manufactured.

Brachytherapy equipment’s falling in class III, need premarket approval (PMA), which involves extensive clinical testing and review, compliance with that is very challenging, since brachytherapy equipment’s involve use of radioactive materials, who can cause safety issues in patients.

Biocompatibility of the materials used in brachytherapy equipment is another major challenge, material used in manufacturing brachytherapy medical devices should be highly safe to the patient not showing any adverse effects on patients health.

Risk in development of Brachytherapy treatment options:

High Cost of Brachytherapy Treatment; The high costs associated with brachytherapy equipment and procedures create significant barriers to accessibility, particularly in low- and middle-income countries (LMICs). These regions face substantial challenges due to the steep initial investment required for advanced brachytherapy machines, which can range from USD 1,200 to USD 30,000. This initial expenditure, coupled with ongoing maintenance costs and the necessity for specialized training for healthcare professionals, can be prohibitive for many medical institutions struggling with limited budgets.

Competition From Alternative Cancer Treatment Modalities; Competition from alternative cancer treatment modalities significantly restrains the growth of the global brachytherapy market. As healthcare providers have access to various effective treatments, such as external beam radiation therapy, surgery, and systemic therapies, they may opt for these alternatives due to their established protocols, familiarity, and sometimes broader acceptance among patients. These competing options can overshadow the unique advantages of brachytherapy, such as its targeted approach and reduced side effects. Moreover, many gynecologic cancers can be effectively treated with brachytherapy. However, some patients are unable to tolerate brachytherapy due to medical or other conditions. For these patients, stereotactic body radiotherapy (SBRT) provides an alternative treatment option. Additionally, some healthcare facilities may prioritize investments in more widely recognized technologies, further limiting the resources allocated to brachytherapy. This competitive landscape can result in lower adoption rates and utilization of brachytherapy, ultimately impeding its market growth and availability for patients who could benefit from this localized treatment option.

Brachytherapy Competitive Landscape Dashboard:

Companies With Marketed Brachytherapy Products:

-

Elekta

-

Siemens Healthineers AG

-

BEBIG Medical GmbH

-

Theragenics Corporation

-

Eckert & Ziegler

-

Becton, Dickinson and Company

-

GE Healthcare

-

Merit Medical Systems

-

Best Medical International, Inc.

-

IsoAid, LLC

Regulatory Landscape - Table of Content

Table of contents will appear here once available.

Customer Stories

“This is really good guys. Excellent work on a tight deadline. I will continue to use you going forward and recommend you to others. Nice job”

“Thanks. It’s been a pleasure working with you, please use me as reference with any other Intel employees.”

“Thanks for sending the report it gives us a good global view of the Betaïne market.”

“Thank you, this will be very helpful for OQS.”

“We found the report very insightful! we found your research firm very helpful. I'm sending this email to secure our future business.”

“I am very pleased with how market segments have been defined in a relevant way for my purposes (such as "Portable Freezers & refrigerators" and "last-mile"). In general the report is well structured. Thanks very much for your efforts.”

“I have been reading the first document or the study, ,the Global HVAC and FP market report 2021 till 2026. Must say, good info! I have not gone in depth at all parts, but got a good indication of the data inside!”

“We got the report in time, we really thank you for your support in this process. I also thank to all of your team as they did a great job.”