Expansion in Coatings and Paints

The Global Neopentyl Glycol Market Industry is significantly influenced by the expansion of the coatings and paints sector. Neopentyl glycol serves as a key ingredient in the formulation of alkyd resins, which are widely used in industrial and decorative coatings. The increasing demand for high-quality, durable coatings in various industries, including construction and manufacturing, propels the growth of neopentyl glycol. As sustainability becomes a priority, the shift towards eco-friendly coatings further enhances the market potential. The anticipated growth in this sector contributes to the overall market value, supporting the projected increase from 1.71 USD Billion in 2024 to 2.95 USD Billion by 2035.

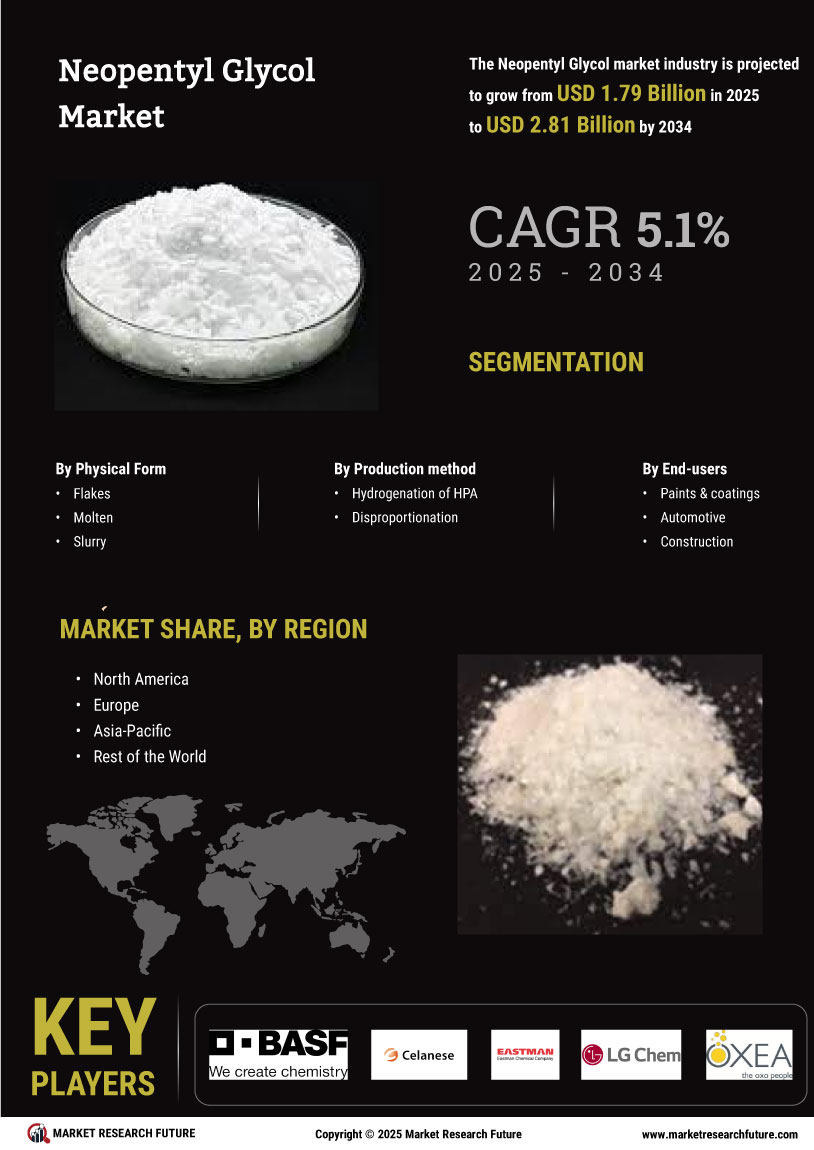

Growing Demand in Automotive Sector

The Global Neopentyl Glycol Market Industry experiences a notable surge in demand driven by the automotive sector. Neopentyl glycol is utilized in the production of high-performance coatings and adhesives, which are essential for automotive applications. As the automotive industry increasingly focuses on lightweight materials and environmentally friendly solutions, the demand for neopentyl glycol is projected to rise. In 2024, the market value is estimated at 1.71 USD Billion, with expectations to reach 2.95 USD Billion by 2035, reflecting a compound annual growth rate (CAGR) of 5.09% from 2025 to 2035. This trend indicates a robust growth trajectory for neopentyl glycol in automotive applications.

Diverse Applications Across Industries

The Global Neopentyl Glycol Market Industry is characterized by its diverse applications across various sectors, including automotive, coatings, and plastics. Neopentyl glycol's versatility as a building block for resins and plasticizers makes it a valuable component in numerous formulations. As industries seek to enhance product performance and durability, the demand for neopentyl glycol continues to grow. This broad applicability not only supports the market's expansion but also mitigates risks associated with dependency on a single sector. The anticipated growth in applications across multiple industries is likely to sustain the market's upward trajectory, contributing to its projected increase in value.

Rising Demand for Sustainable Products

The Global Neopentyl Glycol Market Industry is witnessing a shift towards sustainable and bio-based products. As environmental regulations tighten globally, manufacturers are increasingly seeking alternatives to traditional petrochemical-based materials. Neopentyl glycol, with its potential for bio-based production, aligns with this trend. The growing consumer preference for eco-friendly products drives innovation and investment in sustainable neopentyl glycol production methods. This shift not only enhances the market's appeal but also positions neopentyl glycol as a viable option for manufacturers aiming to meet sustainability goals. Consequently, this trend is expected to contribute to the market's growth trajectory in the coming years.

Technological Advancements in Production

The Global Neopentyl Glycol Market Industry benefits from ongoing technological advancements in production processes. Innovations in chemical synthesis and processing techniques enhance the efficiency and yield of neopentyl glycol production. These advancements not only reduce production costs but also improve the quality of the final product, making it more attractive to manufacturers. As production becomes more efficient, the market is likely to see increased competition and a broader range of applications for neopentyl glycol. This evolution in production technology is expected to play a crucial role in supporting the market's growth, particularly as it aims to meet the rising global demand.