Market Growth Projections

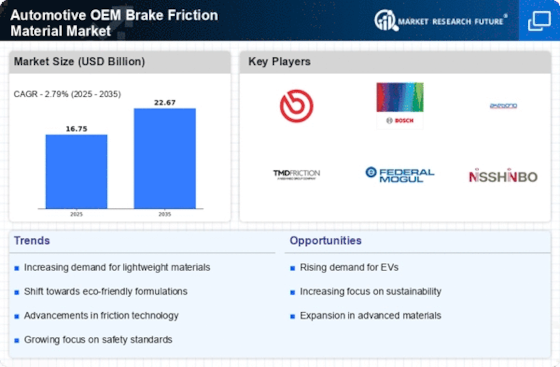

The Global Automotive OEM Brake Friction Material Market Industry is projected to experience substantial growth over the coming years. In 2024, the market is expected to reach 16.8 USD Billion, with further expansion anticipated as it approaches 22.7 USD Billion by 2035. This growth trajectory indicates a compound annual growth rate (CAGR) of 2.79% from 2025 to 2035. Such projections reflect the increasing demand for high-performance brake materials driven by rising vehicle production, technological advancements, and heightened consumer awareness regarding safety. These factors collectively contribute to a favorable market outlook, positioning the industry for sustained growth.

Growing Vehicle Production

The Global Automotive OEM Brake Friction Material Market Industry is poised for growth as vehicle production continues to rise. In 2024, the market is projected to reach 16.8 USD Billion, driven by increasing demand for automobiles across various regions. This surge in production is primarily attributed to the expansion of automotive manufacturing facilities and advancements in production technologies. As more vehicles are produced, the need for high-quality brake friction materials becomes imperative to ensure safety and performance. Consequently, manufacturers are focusing on developing innovative materials that meet stringent safety standards, thereby enhancing their market presence.

Market Dynamics and Competitive Landscape

The Global Automotive OEM Brake Friction Material Market Industry is characterized by dynamic market conditions and a competitive landscape. Various players are vying for market share, leading to innovations in product offerings and pricing strategies. This competition encourages manufacturers to enhance their production capabilities and invest in advanced technologies. As the market evolves, collaborations and partnerships among OEMs and suppliers are likely to become more prevalent, fostering innovation and improving supply chain efficiency. The anticipated CAGR of 2.79% from 2025 to 2035 suggests a steady growth trajectory, indicating a robust market environment.

Regulatory Compliance and Safety Standards

Regulatory frameworks and safety standards significantly influence the Global Automotive OEM Brake Friction Material Market Industry. Governments worldwide are implementing stringent regulations to enhance vehicle safety and reduce environmental impact. Compliance with these regulations necessitates the use of high-performance brake materials that meet specific safety criteria. As a result, manufacturers are compelled to innovate and adapt their product offerings to align with these evolving standards. This dynamic environment fosters competition among OEMs, driving the development of superior brake friction materials that not only comply with regulations but also enhance overall vehicle performance.

Technological Advancements in Brake Materials

Technological innovations play a pivotal role in shaping the Global Automotive OEM Brake Friction Material Market Industry. The introduction of advanced materials, such as carbon-ceramic and low-metallic formulations, enhances braking performance and reduces wear. These advancements not only improve vehicle safety but also contribute to lower emissions and noise levels. As manufacturers invest in research and development, the market is likely to witness a shift towards eco-friendly materials that comply with global environmental regulations. This trend indicates a growing awareness among consumers and manufacturers alike regarding the importance of sustainable practices in the automotive sector.

Increasing Consumer Awareness of Vehicle Safety

Consumer awareness regarding vehicle safety is a crucial driver for the Global Automotive OEM Brake Friction Material Market Industry. As safety features become a priority for consumers, the demand for high-quality brake materials is expected to rise. This trend is evident in the growing preference for vehicles equipped with advanced braking systems, which rely on superior friction materials for optimal performance. Manufacturers are responding to this demand by investing in research and development to create innovative brake solutions that enhance safety. The projected market growth to 22.7 USD Billion by 2035 reflects this increasing consumer focus on safety and performance.