Leading market players are investing heavily in research and development to expand their product lines, which will help the Lightweight Metal Market, grow even more. Market participants are also undertaking various strategic activities to expand their global footprint, with important market developments including new product launches, contractual agreements, mergers and acquisitions, higher investments, and collaboration with other organizations. To expand and survive in a more competitive and rising market climate, Lightweight Metal industry must offer cost-effective items.

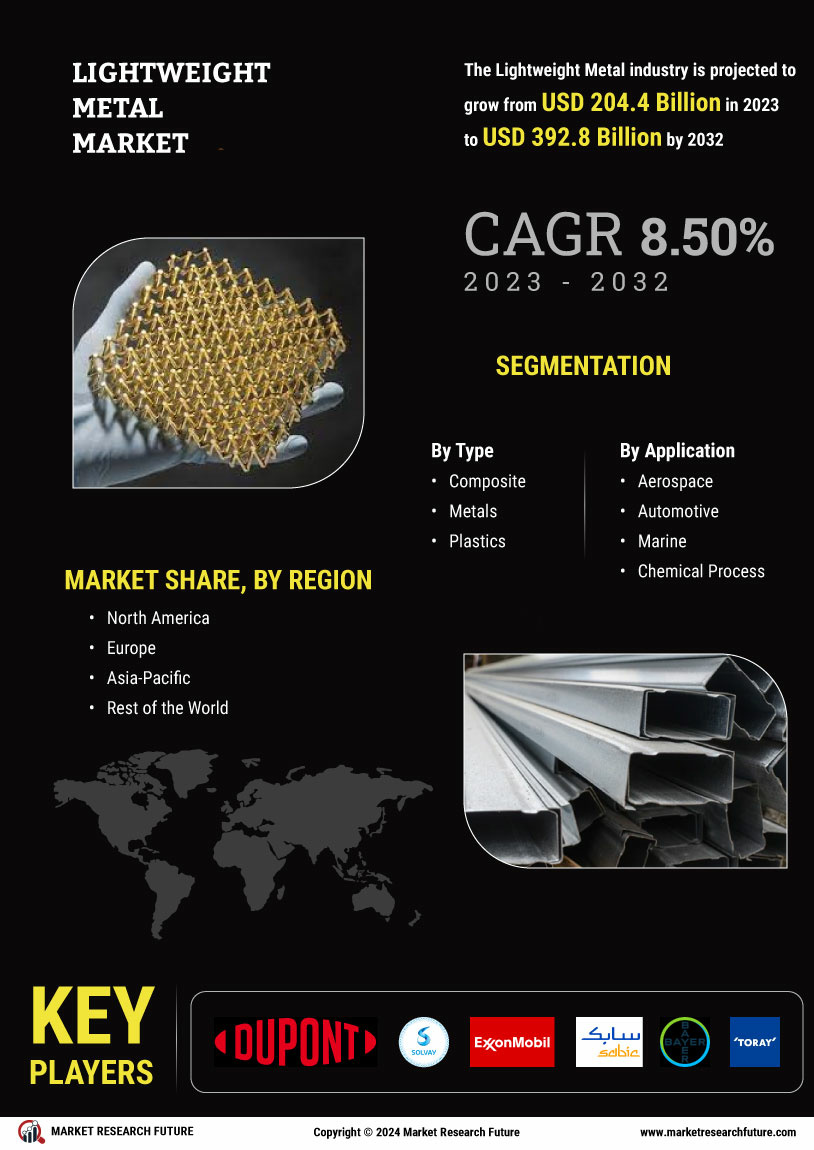

Manufacturing locally to minimize operational costs is one of the key business tactics manufacturers use in the global Lightweight Metal industry to benefit clients and increase the market sector. In recent years, the Lightweight Metal industry has offered some of the most significant advantages to lightweight metal. Major players in the Lightweight Metal Market, including DuPont, Solvay, Exxon Mobil Corporation, SABIC, Bayer AG, Toray Industries, Inc., Novelis, ArcelorMittal, PPG Industries, Inc., Alcoa Corporation, US Magnesium LLC, Owens Corning, Hexcel Corporation, and others, are attempting to increase market demand by investing in research and development operations.

Toray Industries, Inc. (Japan) is a multinational corporation specializing in industrial products based on polymer chemistry, biochemistry, and organic synthetic chemistry technologies. Since its founding in 1926, Toray Group has upheld the management principle of "realizing that corporations are public institutions of society and contributing to society through its business." Toray Group prioritizes corporate social responsibility and integrates CSR initiatives into management strategies, working towards the Group's sustainable development and creating a sustainable world. Fibers, textiles, plastics, and chemicals were its first business sectors.

The company has also expanded into other industries, including advanced composite materials, electronics, IT products, housing and engineering and large reverse osmosis membranes. The company is listed in the first section of the Tokyo Stock Exchange. It is a constituent of the TOPIX 100 and Nikkie 225 stock market indices. The 20 nations and areas in which Toray operates are Japan, China, Hong Kong, Taiwan, South Korea, Indonesia, Malaysia, Singapore, Thailand, India, Czech Republic, France, Germany, Italy, Netherlands, Switzerland, United Kingdom, Mexico, and the United States.

In August 2022, Toray Industries, Inc. released its 3D printer to manufacture automotive parts, heat-resistant equipment, and power tools with high strength and sound design accuracy.

LyondellBasell is a pioneer in the worldwide chemical sector that develops products for environmentally friendly daily living. A circular and low-carbon economy is becoming possible thanks to targeted investments and cutting-edge technologies. The company's goal is to unleash value for society, investors, and customers in all the company does. As one of the biggest producers of polymers worldwide and a pioneer in polyolefin technologies, the company designs produces and sells polymers.

Company beliefs, commitments, and purpose all represent the role a company wants to play in the world, the special contributions a company can make to fulfil that mission, and the way the company acts. When combined with its business plan, the company's story and culture effectively convey its role in creating a more sustainable world.

In October LyondellBasell Industries Holdings BV produced a PP compound made up of PP compound material, which lowered the vehicle's weight by 10kg. It can replace metal, thin the walls of components and foam parts, lower material density, and remove paint from automobiles.