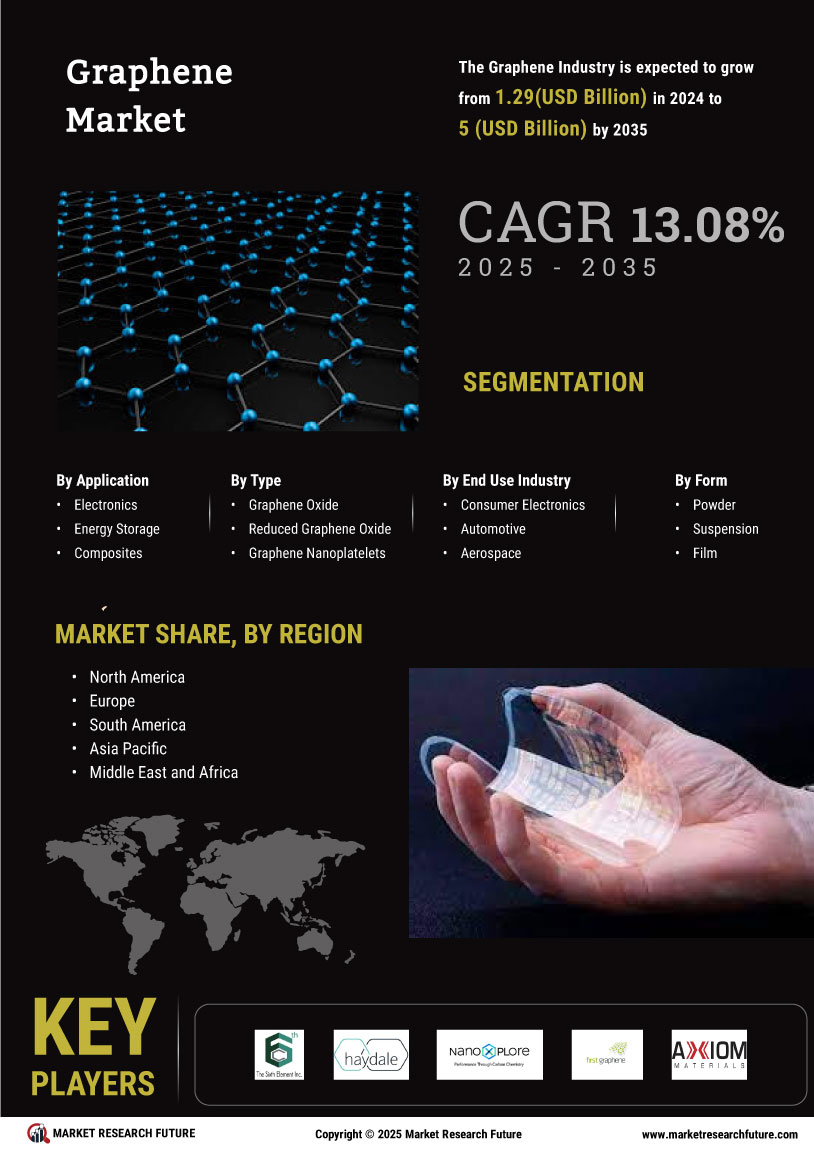

Increasing Applications in Healthcare

The Graphene Market is witnessing a surge in applications within the healthcare sector. Graphene Market's unique properties, such as its biocompatibility and electrical conductivity, make it an attractive material for medical devices, drug delivery systems, and biosensors. The market for graphene-based biomedical applications is projected to grow significantly, with estimates suggesting a compound annual growth rate of over 30% in the coming years. This growth is driven by the increasing need for advanced medical technologies and the rising prevalence of chronic diseases. As research continues to unveil new applications, the Graphene Market is likely to expand further, potentially revolutionizing healthcare solutions.

Sustainability and Environmental Benefits

Sustainability is becoming a pivotal concern across industries, and the Graphene Market is no exception. Graphene Market's potential to enhance the performance of renewable energy technologies, such as solar cells and batteries, positions it as a key player in the transition to sustainable energy solutions. The incorporation of graphene can lead to more efficient energy storage systems, which is essential for the growing demand for renewable energy sources. As governments and organizations prioritize sustainability, the Graphene Market is expected to thrive, driven by the need for environmentally friendly materials and technologies that support a greener future.

Growth in Research and Development Activities

The Graphene Market is significantly influenced by the increasing investment in research and development activities. Academic institutions and private companies are dedicating substantial resources to explore the myriad applications of graphene, from advanced materials to electronics. This focus on innovation is likely to yield breakthroughs that could expand the market further. With funding from various governmental and private entities, the Graphene Market is expected to see a rise in new products and applications, potentially leading to a more robust market landscape. As R&D continues to evolve, the implications for the Graphene Market could be profound, fostering a culture of continuous improvement and adaptation.

Innovations in Electronics and Semiconductors

The Graphene Market is experiencing a transformative phase due to innovations in electronics and semiconductors. Graphene Market's exceptional electrical properties enable faster and more efficient electronic devices, which is crucial in an era where consumer demand for high-performance gadgets is escalating. The market for graphene-based electronic components is projected to reach several billion dollars by 2027, driven by advancements in flexible electronics, sensors, and transistors. As companies invest in research and development to harness graphene's potential, the Graphene Market is likely to expand, fostering a new generation of electronic devices that could redefine user experiences.

Demand for Lightweight Materials in Automotive

The automotive sector is increasingly adopting lightweight materials to enhance fuel efficiency and reduce emissions. The Graphene Market is poised to benefit from this trend, as graphene composite market offer superior strength-to-weight ratios compared to traditional materials. With the automotive industry aiming for a 20% reduction in vehicle weight by 2030, the demand for graphene-enhanced materials is expected to rise. This shift not only aligns with regulatory pressures for lower emissions but also caters to consumer preferences for more efficient vehicles. Consequently, the Graphene Market is likely to see substantial growth as automotive manufacturers integrate graphene into their production processes.