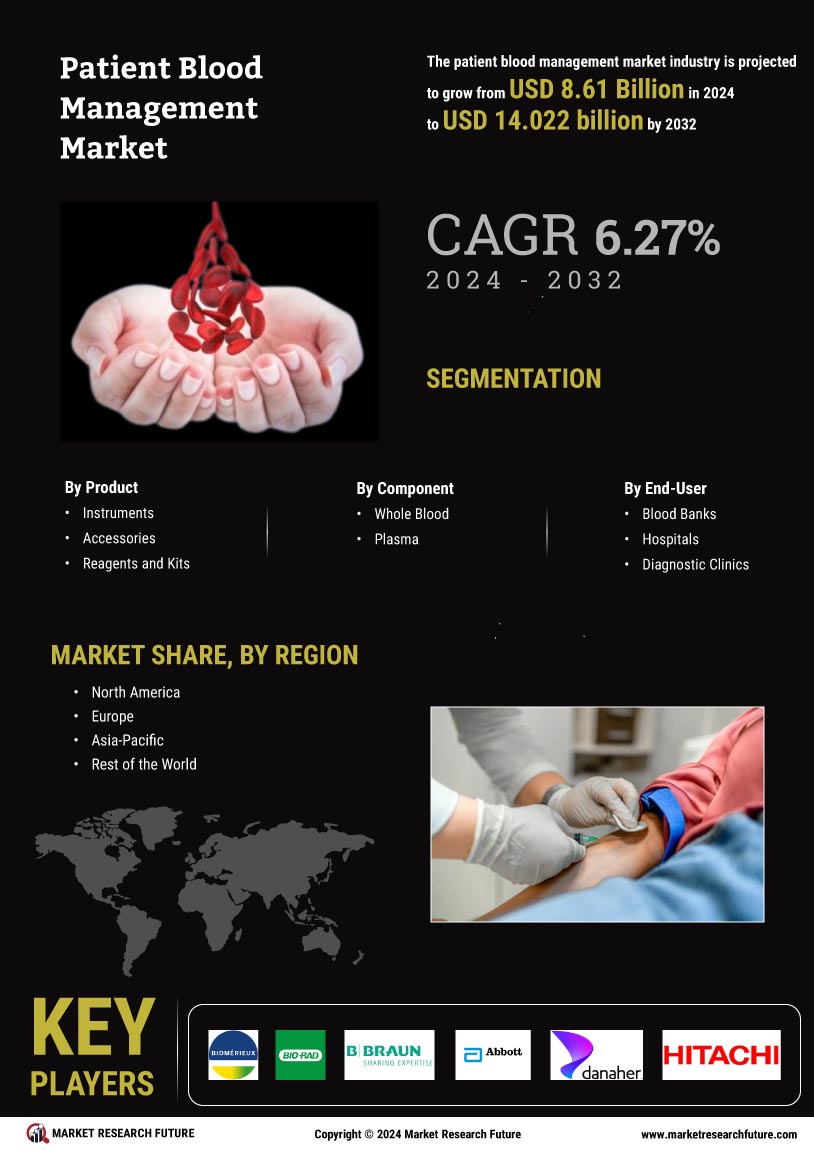

Regulatory Support and Compliance

Regulatory frameworks and guidelines established by health authorities are instrumental in driving the Patient Blood Management Market. These regulations often mandate the implementation of standardized blood management practices to ensure patient safety and improve clinical outcomes. For example, organizations such as the World Health Organization and various national health agencies advocate for the adoption of patient blood management protocols. Compliance with these regulations not only enhances patient care but also mitigates legal risks for healthcare providers. As a result, hospitals are increasingly investing in training and resources to align with these guidelines, thereby fostering the growth of the Patient Blood Management Market. The ongoing evolution of regulatory requirements is expected to further stimulate advancements in blood management practices.

Growing Awareness of Patient Safety

The heightened awareness surrounding patient safety and quality of care is a significant driver for the Patient Blood Management Market. Healthcare institutions are increasingly prioritizing strategies that minimize the risks associated with blood transfusions, such as transfusion-related infections and adverse reactions. This shift is reflected in the implementation of evidence-based guidelines and protocols aimed at optimizing blood use. Studies indicate that effective patient blood management can reduce transfusion rates by up to 30%, thereby enhancing patient safety and reducing healthcare costs. As hospitals and clinics strive to meet regulatory standards and improve patient outcomes, the focus on patient blood management is likely to gain momentum, further propelling the growth of the Patient Blood Management Market.

Increasing Prevalence of Chronic Diseases

The rising incidence of chronic diseases such as cardiovascular disorders, diabetes, and cancer is a pivotal driver for the Patient Blood Management Market. These conditions often necessitate frequent blood transfusions and surgical interventions, thereby increasing the demand for effective blood management strategies. According to recent data, approximately 60% of patients undergoing major surgeries require blood transfusions, highlighting the critical need for robust blood management systems. As healthcare providers strive to enhance patient outcomes and minimize complications associated with blood transfusions, the focus on patient blood management becomes increasingly pronounced. This trend is likely to propel the growth of the Patient Blood Management Market, as hospitals and clinics invest in advanced technologies and protocols to optimize blood usage and improve patient safety.

Technological Innovations in Blood Management

Technological advancements play a crucial role in shaping the Patient Blood Management Market. Innovations such as automated blood collection systems, advanced blood screening technologies, and data analytics tools are transforming how healthcare providers manage blood resources. For instance, the integration of artificial intelligence in blood management systems allows for real-time monitoring and predictive analytics, which can significantly reduce wastage and enhance transfusion safety. The market for blood management technologies is projected to grow at a compound annual growth rate of over 10% in the coming years, driven by the increasing adoption of these innovative solutions. As healthcare facilities seek to improve operational efficiency and patient outcomes, the emphasis on adopting cutting-edge technologies in the Patient Blood Management Market is expected to intensify.

Rising Demand for Cost-Effective Healthcare Solutions

The escalating need for cost-effective healthcare solutions is a driving force behind the Patient Blood Management Market. As healthcare costs continue to rise, providers are under pressure to implement strategies that enhance efficiency while maintaining high-quality care. Patient blood management initiatives have been shown to reduce unnecessary transfusions, thereby lowering associated costs. Research indicates that effective blood management can save healthcare systems millions annually by minimizing transfusion-related complications and optimizing blood utilization. This financial incentive is prompting healthcare facilities to adopt comprehensive blood management programs, which in turn is likely to fuel the growth of the Patient Blood Management Market. As the focus on value-based care intensifies, the demand for innovative and cost-effective blood management solutions is expected to increase.