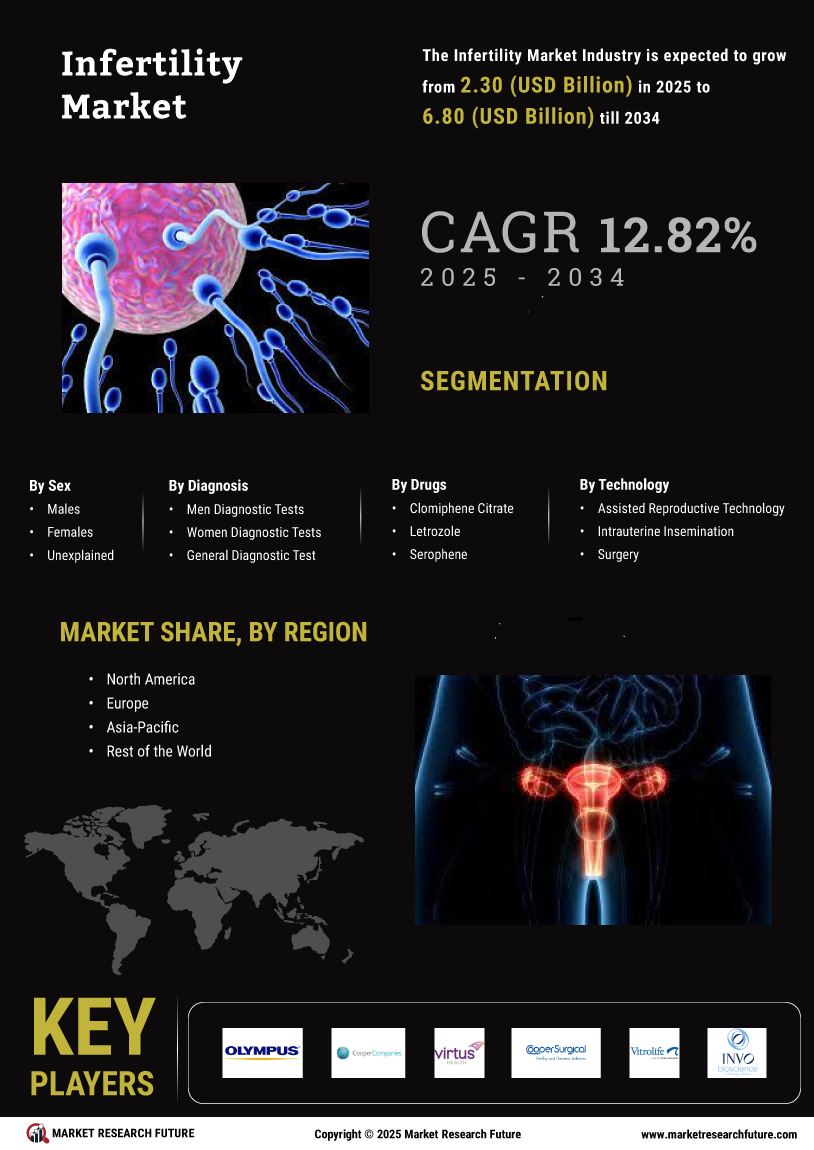

Market Growth Projections

The Global Infertility Market Industry is projected to experience substantial growth in the coming years. By 2024, the market is anticipated to reach 19.7 USD Billion, with further expansion expected to 30.5 USD Billion by 2035. This growth trajectory indicates a compound annual growth rate (CAGR) of 4.03% from 2025 to 2035. Such projections highlight the increasing demand for infertility treatments and services, driven by factors such as rising infertility rates, technological advancements, and greater awareness. As the market evolves, stakeholders are likely to explore new opportunities for innovation and investment, positioning themselves to meet the needs of a growing patient population.

Rising Prevalence of Infertility

The Global Infertility Market Industry is witnessing a notable increase in infertility rates, attributed to various factors such as delayed childbearing and lifestyle changes. According to recent data, approximately 15% of couples globally experience infertility issues. This rising prevalence is driving demand for fertility treatments and services, contributing to the market's projected growth. By 2024, the market is expected to reach 19.7 USD Billion, reflecting a growing awareness and acceptance of assisted reproductive technologies. As more individuals seek solutions for infertility, the industry is likely to expand, fostering innovation in treatment options and enhancing patient access.

Government Initiatives and Support

Government policies and initiatives play a crucial role in shaping the Global Infertility Market Industry. Many countries are implementing programs to support infertility treatments, including funding for research and subsidies for patients. For example, some nations offer financial assistance for IVF procedures, making them more accessible to a broader population. These initiatives not only alleviate the financial burden on couples but also encourage the development of advanced fertility clinics and services. As governments recognize the importance of addressing infertility, the market is likely to benefit from increased investment and support, further driving growth in the coming years.

Demographic Shifts and Lifestyle Changes

Demographic changes, including an aging population and evolving lifestyle choices, are significantly impacting the Global Infertility Market Industry. As individuals prioritize education and career advancement, many are delaying family planning, which can lead to increased infertility rates. Additionally, lifestyle factors such as obesity, smoking, and stress are contributing to fertility challenges. These shifts necessitate a greater demand for fertility solutions, as couples seek to overcome the biological limitations associated with age and lifestyle. The market's growth is expected to reflect these demographic trends, with a notable increase in service utilization as awareness of fertility issues rises.

Technological Advancements in Fertility Treatments

Innovations in reproductive technologies are significantly influencing the Global Infertility Market Industry. Techniques such as in vitro fertilization (IVF), intracytoplasmic sperm injection (ICSI), and preimplantation genetic testing (PGT) are becoming increasingly sophisticated. These advancements not only improve success rates but also enhance patient experiences. For instance, the introduction of artificial intelligence in embryo selection has shown promising results in optimizing outcomes. As these technologies evolve, they are expected to attract more patients, thereby propelling the market forward. The anticipated growth trajectory suggests that by 2035, the market could reach 30.5 USD Billion, underscoring the importance of continuous innovation.

Increasing Awareness and Acceptance of Fertility Treatments

The Global Infertility Market Industry is experiencing a shift in societal attitudes towards fertility treatments. Increased awareness campaigns and educational initiatives are helping to destigmatize infertility and promote available treatment options. As a result, more individuals and couples are seeking assistance, leading to a rise in demand for fertility services. This trend is particularly evident in urban areas where access to information is more prevalent. The growing acceptance of assisted reproductive technologies is expected to contribute to a compound annual growth rate (CAGR) of 4.03% from 2025 to 2035, indicating a robust market expansion driven by informed consumer choices.