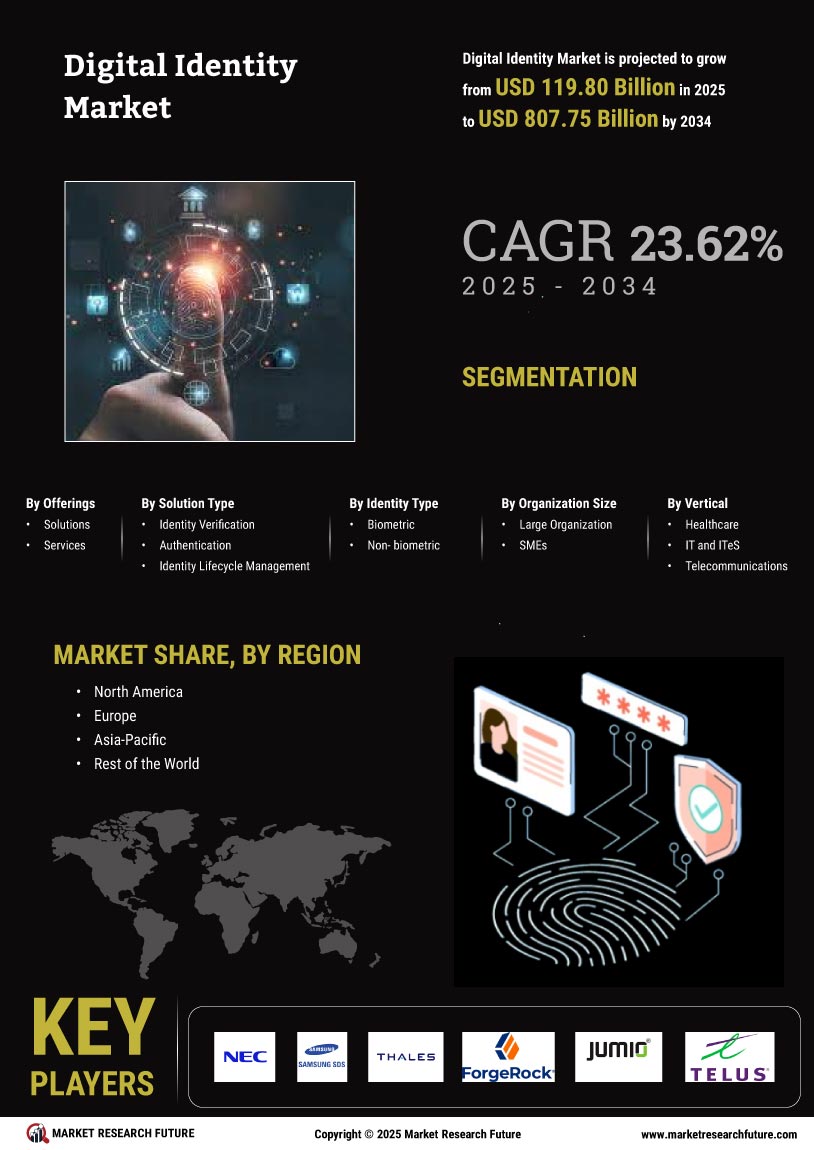

The Digital Identity Market is currently experiencing a transformative phase, driven by the increasing need for secure and efficient identity verification solutions. As organizations and individuals alike seek to enhance their online presence, the demand for robust digital identity frameworks continues to grow. This market encompasses a wide array of technologies and services, including biometric authentication, identity management systems, and decentralized identity solutions. The integration of advanced technologies, such as artificial intelligence and blockchain, appears to be reshaping the landscape, offering innovative approaches to identity verification and management. Moreover, regulatory frameworks are evolving to address the complexities associated with digital identities.

The digital identity in healthcare market is witnessing rapid growth driven by secure patient identification, electronic health records, and telehealth authentication. Key digital identity market trends include rising biometric adoption, decentralized identity models, and AI-driven authentication systems. Governments and regulatory bodies are implementing policies that promote secure digital identity practices while ensuring user privacy. This regulatory push is likely to foster trust among users and encourage wider adoption of digital identity solutions across various sectors, including finance, healthcare, and e-commerce. As the Digital Identity Market continues to mature, it seems poised to play a crucial role in shaping the future of online interactions and transactions, potentially leading to a more secure and efficient digital ecosystem.

The digital identity in airports market is emerging as a critical application area, driven by biometric boarding, contactless immigration, and passenger authentication systems. This digital identity in airports market analysis highlights increasing investments in biometric security, automated border control, and passenger identity management systems. The digital identity in education market is expanding rapidly as institutions deploy secure student identification, online examination authentication, and digital credential systems. The digital identity in education market share is increasing steadily as governments promote digital learning ecosystems and identity-based access controls.

Rise of Biometric Solutions

The adoption of biometric technologies is gaining momentum within the Digital Identity Market. Organizations are increasingly utilizing fingerprint, facial recognition, and iris scanning methods to enhance security and streamline user authentication processes. This trend suggests a shift towards more personalized and secure identity verification methods.

The digital identity in airports market size is expected to expand significantly during the forecast period, supported by rising global air travel and smart airport deployments. Key digital identity in airports market trends include facial recognition boarding, biometric immigration clearance, and integration with airline identity platforms. Digital identity in BFSI market trends indicate rising adoption of biometric authentication, AI-driven fraud detection, and digital KYC platforms.

Decentralized Identity Models

Decentralized identity solutions are emerging as a viable alternative to traditional identity management systems. By leveraging blockchain technology, these models empower individuals to control their own identity data, reducing reliance on centralized authorities. This trend indicates a growing preference for privacy and user autonomy in identity management. The digital identity solution market is driven by strong demand for identity verification, authentication, and lifecycle management platforms. The digital identity solutions market continues to dominate the industry, supported by enterprise adoption of biometric and authentication platforms. The digital identity verification market holds the largest share due to widespread adoption in BFSI, government, and healthcare sectors.

Regulatory Compliance and Standards

The Digital Identity Market is witnessing a heightened focus on regulatory compliance and the establishment of industry standards. As governments implement stricter data protection laws, organizations are compelled to adopt solutions that align with these regulations. This trend highlights the importance of ensuring security and privacy in digital identity practices. Digital identity in education market trends highlight growing use of biometric attendance, online identity verification, and blockchain-based academic credentials. The digital identity in government sector market is expanding as national ID programs, e-governance platforms, and citizen authentication systems gain adoption.