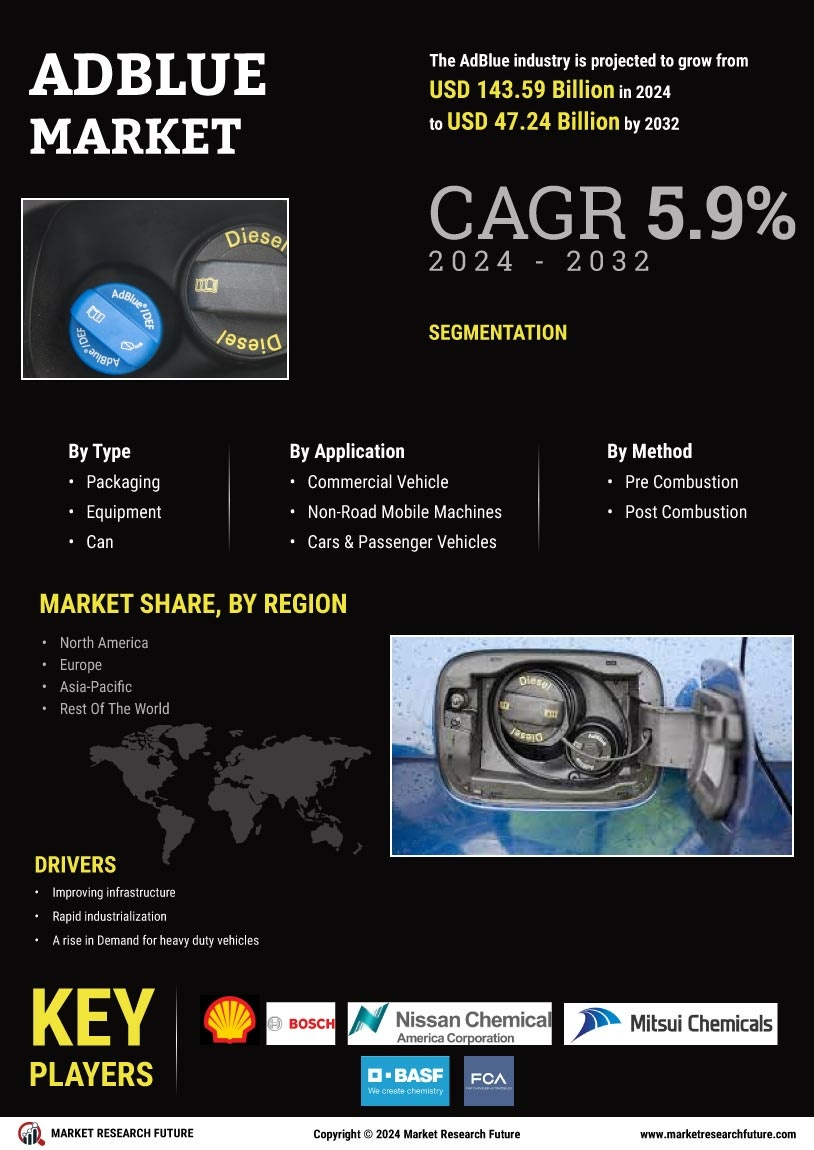

Rising Diesel Vehicle Sales

The rising sales of diesel vehicles are a pivotal driver for the AdBlue Market. Diesel engines are known for their fuel efficiency and lower carbon dioxide emissions, making them a popular choice among consumers and businesses alike. As diesel vehicles become more prevalent, the demand for AdBlue, which is essential for reducing harmful emissions, is expected to increase correspondingly. Recent data indicates that diesel vehicle sales have seen a resurgence, particularly in commercial sectors such as transportation and logistics. This trend suggests a robust growth trajectory for the AdBlue Market, as manufacturers and suppliers work to meet the needs of a growing diesel vehicle fleet.

Expansion of Distribution Networks

The expansion of distribution networks is a critical factor influencing the AdBlue Market. As demand for AdBlue continues to rise, the establishment of efficient distribution channels becomes essential to ensure product availability. Companies are increasingly investing in logistics and supply chain enhancements to facilitate the timely delivery of AdBlue to consumers and businesses. This expansion not only improves accessibility but also helps stabilize prices in the market. Furthermore, partnerships with fuel stations and automotive service providers are becoming more common, allowing for greater convenience for end-users. This strategic growth in distribution networks is expected to support the ongoing demand for AdBlue, thereby reinforcing its position in the market.

Technological Innovations in Production

Technological advancements in the production of AdBlue are reshaping the AdBlue Market. Innovations such as improved manufacturing processes and enhanced distribution logistics are contributing to the increased availability and affordability of AdBlue. For example, the development of more efficient production methods has led to a reduction in production costs, which can potentially lower retail prices for consumers. Furthermore, advancements in storage and transportation technologies ensure that AdBlue remains stable and effective over time. As the market continues to evolve, these technological innovations are likely to play a crucial role in meeting the growing demand for AdBlue, particularly in regions with stringent emission regulations.

Regulatory Compliance and Emission Standards

The AdBlue Market is significantly influenced by stringent regulatory compliance and emission standards imposed by various governments. These regulations aim to reduce nitrogen oxide emissions from diesel engines, thereby promoting the use of AdBlue as a solution. For instance, the introduction of Euro 6 standards has necessitated the adoption of selective catalytic reduction (SCR) technology in vehicles, which requires AdBlue for optimal performance. As a result, the demand for AdBlue has surged, with projections indicating a compound annual growth rate of approximately 5% over the next few years. This regulatory landscape not only drives the market but also encourages manufacturers to innovate and improve the efficiency of AdBlue production and distribution.

Environmental Awareness and Sustainability Initiatives

Growing environmental awareness among consumers and businesses is driving the AdBlue Market towards sustainability. As stakeholders become more conscious of their environmental impact, there is a marked shift towards adopting cleaner technologies, including the use of AdBlue in diesel engines. This shift is further supported by corporate sustainability initiatives that aim to reduce carbon footprints. Many companies are now prioritizing the use of AdBlue as part of their commitment to environmental stewardship. This trend is likely to bolster the market, as more organizations recognize the importance of compliance with environmental regulations and the benefits of using AdBlue to achieve their sustainability goals.