Market Analysis

In-depth Analysis of Commercial Aircraft Aftermarket Parts Market Industry Landscape

In the realm of replacement parts, large Original Equipment Manufacturers (OEMs) traditionally hold a monopoly on the aftermarket business. However, as in any industry, the introduction of alternative aftermarket products that match or exceed the quality of OEM offerings can drive down prices and foster healthy competition. In the aviation sector, this competition primarily comes from smaller independent Maintenance, Repair, and Overhaul (MRO) providers and Parts Manufacturer Approval (PMA) parts manufacturers.

The Federal Aviation Administration (FAA) has played a pivotal role in shaping the landscape of aftermarket parts since the 1950s. The FAA grants Parts Manufacturer Approval to third-party manufacturers, allowing them to produce replacement parts for aircraft. PMA parts are estimated to provide cost savings ranging between 30 to 50%, coupled with potential design improvements. The emphasis on cost-effectiveness is a compelling argument for the adoption of PMA parts by operators and airlines.

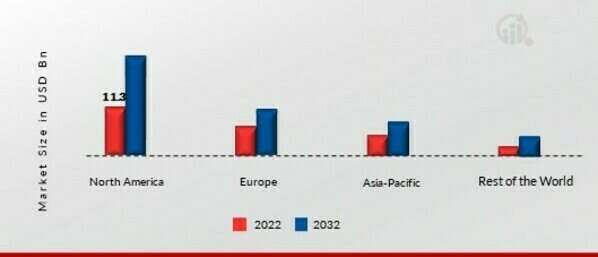

Most OEMs assert that procuring parts from PMA manufacturers proves to be more economical in the long run. This assertion has gained traction, leading to increased acceptance of PMA parts by many air carriers in North America. The competition between OEMs and PMA manufacturers in this region is already pronounced. However, looking ahead, PMA manufacturers are expected to pivot their focus towards other regions of the world, particularly Asia-Pacific and the Middle East, where the acceptance and usage of PMA parts are rapidly evolving.

In North America, where PMA acceptance is widespread, air carriers recognize the cost benefits and quality assurance offered by PMA parts. This market maturity has paved the way for PMA manufacturers to establish themselves as viable alternatives to traditional OEMs. In contrast, regions such as Europe, Asia, and other developing countries still grapple with a prevailing perception that OEM parts are of higher quality and more reliable. In the realm of replacement parts, large Original Equipment Manufacturers (OEMs) traditionally hold a monopoly on the aftermarket business. However, as in any industry, the introduction of alternative aftermarket products that match or exceed the quality of OEM offerings can drive down prices and foster healthy competition. In the aviation sector, this competition primarily comes from smaller independent Maintenance, Repair, and Overhaul (MRO) providers and Parts Manufacturer Approval (PMA) parts manufacturers.

The Federal Aviation Administration (FAA) has played a pivotal role in shaping the landscape of aftermarket parts since the 1950s. The FAA grants Parts Manufacturer Approval to third-party manufacturers, allowing them to produce replacement parts for aircraft. PMA parts are estimated to provide cost savings ranging between 30 to 50%, coupled with potential design improvements. The emphasis on cost-effectiveness is a compelling argument for the adoption of PMA parts by operators and airlines.

Most OEMs assert that procuring parts from PMA manufacturers proves to be more economical in the long run. This assertion has gained traction, leading to increased acceptance of PMA parts by many air carriers in North America. The competition between OEMs and PMA manufacturers in this region is already pronounced. However, looking ahead, PMA manufacturers are expected to pivot their focus towards other regions of the world, particularly Asia-Pacific and the Middle East, where the acceptance and usage of PMA parts are rapidly evolving.

In North America, where PMA acceptance is widespread, air carriers recognize the cost benefits and quality assurance offered by PMA parts. This market maturity has paved the way for PMA manufacturers to establish themselves as viable alternatives to traditional OEMs. In contrast, regions such as Europe, Asia, and other developing countries still grapple with a prevailing perception that OEM parts are of higher quality and more reliable.

The competition dynamics in the aftermarket parts sector are evolving, and PMA manufacturers are strategically positioning themselves to tap into new markets. While North America remains a competitive arena, the growth potential in Asia-Pacific and the Middle East is becoming increasingly evident. The trajectory of PMA acceptance in these regions indicates a shift towards recognizing the cost-effective and high-quality solutions offered by PMA parts.

Key players dominating the PMA market include AMETEK, a leading global manufacturer of electronic instruments and electromechanical devices. AMETEK has established itself as a reliable source for high-quality PMA parts. Additionally, Parker Hannifin, renowned for its motion and control technologies, is another influential player in the PMA sector. Precision Castparts, specializing in complex metal components and products, is yet another dominant force in the PMA market. These players collectively contribute to the growing acceptance and usage of PMA parts in the aviation industry.

The competition between OEMs and PMA manufacturers extends beyond cost considerations. PMA parts often offer design improvements, contributing to enhanced performance and efficiency. The ongoing advancements in PMA technology and manufacturing processes further strengthen the value proposition of these alternative aftermarket parts.

As the aviation industry continues to globalize, PMA manufacturers are strategically expanding their footprint to capitalize on emerging markets. While North America may have achieved a level of saturation in PMA acceptance, the untapped potential in Asia-Pacific and the Middle East presents an exciting frontier for growth. The challenge lies in dispelling lingering perceptions and demonstrating the reliability and quality of PMA parts in these regions.

In conclusion, the competition between OEMs and PMA manufacturers in the aviation aftermarket parts sector is a dynamic interplay of cost considerations, quality assurances, and market perceptions. While North America has embraced PMA parts, the future growth lies in the rapid adoption of these alternatives in regions like Asia-Pacific and the Middle East. PMA manufacturers, led by key players such as AMETEK, Parker Hannifin, and Precision Castparts, are well-positioned to reshape the aftermarket landscape and establish themselves as formidable contenders in the global aviation industry. The competition dynamics in the aftermarket parts sector are evolving, and PMA manufacturers are strategically positioning themselves to tap into new markets. While North America remains a competitive arena, the growth potential in Asia-Pacific and the Middle East is becoming increasingly evident. The trajectory of PMA acceptance in these regions indicates a shift towards recognizing the cost-effective and high-quality solutions offered by PMA parts.

Key players dominating the PMA market include AMETEK, a leading global manufacturer of electronic instruments and electromechanical devices. AMETEK has established itself as a reliable source for high-quality PMA parts. Additionally, Parker Hannifin, renowned for its motion and control technologies, is another influential player in the PMA sector. Precision Castparts, specializing in complex metal components and products, is yet another dominant force in the PMA market. These players collectively contribute to the growing acceptance and usage of PMA parts in the aviation industry.

The competition between OEMs and PMA manufacturers extends beyond cost considerations. PMA parts often offer design improvements, contributing to enhanced performance and efficiency. The ongoing advancements in PMA technology and manufacturing processes further strengthen the value proposition of these alternative aftermarket parts.

As the aviation industry continues to globalize, PMA manufacturers are strategically expanding their footprint to capitalize on emerging markets. While North America may have achieved a level of saturation in PMA acceptance, the untapped potential in Asia-Pacific and the Middle East presents an exciting frontier for growth. The challenge lies in dispelling lingering perceptions and demonstrating the reliability and quality of PMA parts in these regions.

In conclusion, the competition between OEMs and PMA manufacturers in the aviation aftermarket parts sector is a dynamic interplay of cost considerations, quality assurances, and market perceptions. While North America has embraced PMA parts, the future growth lies in the rapid adoption of these alternatives in regions like Asia-Pacific and the Middle East. PMA manufacturers, led by key players such as AMETEK, Parker Hannifin, and Precision Castparts, are well-positioned to reshape the aftermarket landscape and establish themselves as formidable contenders in the global aviation industry.

Leave a Comment