Rising Energy Costs

The escalating costs of energy are a primary driver for the Residential Combined Heat and Power Market. As households face increasing utility bills, there is a growing inclination towards self-generation of energy. This trend is particularly pronounced in regions where electricity prices have surged by over 30 percent in recent years. The ability of combined heat and power systems to provide both electricity and thermal energy from a single fuel source offers a compelling economic advantage. By reducing reliance on grid electricity, homeowners can mitigate the impact of rising energy costs, thereby enhancing the appeal of the Residential Combined Heat and Power Market. Furthermore, as energy prices continue to fluctuate, the demand for efficient energy solutions is likely to increase, further propelling market growth.

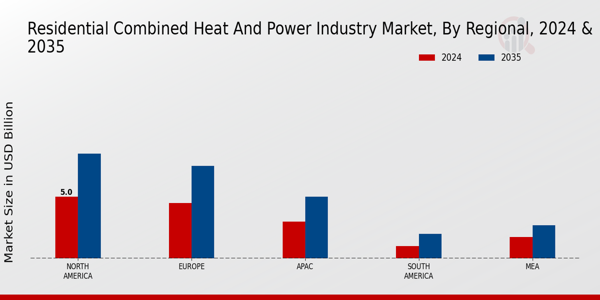

Technological Innovations

Technological innovations play a crucial role in shaping the Residential Combined Heat and Power Market. Advances in energy management systems, such as smart meters and IoT integration, enhance the efficiency and usability of combined heat and power systems. These innovations allow for real-time monitoring and optimization of energy consumption, making it easier for homeowners to manage their energy use effectively. The market has witnessed a surge in the development of more compact and efficient CHP units, which cater to the needs of residential users. As these technologies become more accessible and affordable, the adoption rate of combined heat and power systems is expected to rise, potentially increasing market penetration by 20 percent in the coming years.

Energy Independence and Security

The pursuit of energy independence and security is a significant driver for the Residential Combined Heat and Power Market. As geopolitical tensions and energy supply disruptions become more prevalent, households are increasingly motivated to seek alternative energy solutions. Combined heat and power systems provide a means for homeowners to generate their own energy, thereby reducing dependence on external sources. This trend is particularly relevant in regions that have experienced energy shortages or price volatility. The ability to produce energy on-site not only enhances energy security but also contributes to a more resilient energy infrastructure. As awareness of these benefits grows, the Residential Combined Heat and Power Market is expected to expand, reflecting a shift towards self-sufficiency in energy production.

Regulatory Support and Incentives

Regulatory support and incentives are pivotal in driving the Residential Combined Heat and Power Market. Governments worldwide are implementing policies aimed at promoting energy efficiency and reducing greenhouse gas emissions. These initiatives often include financial incentives, such as tax credits and rebates for homeowners who invest in combined heat and power systems. For instance, certain regions have reported a 25 percent increase in installations due to favorable regulatory frameworks. Such support not only lowers the initial investment barrier but also encourages wider adoption of CHP technologies. As regulatory environments continue to evolve, the Residential Combined Heat and Power Market is likely to experience sustained growth, driven by both consumer interest and governmental backing.

Environmental Sustainability Concerns

Concerns regarding environmental sustainability are increasingly influencing consumer choices, thereby driving the Residential Combined Heat and Power Market. With a heightened awareness of climate change and its implications, many households are seeking ways to reduce their carbon footprint. Combined heat and power systems, which utilize waste heat for additional energy production, present a more sustainable alternative to traditional energy sources. This shift is reflected in the growing number of households adopting such systems, with estimates suggesting a potential increase of 15 percent in installations over the next five years. As consumers prioritize eco-friendly solutions, the Residential Combined Heat and Power Market is poised to benefit from this trend, aligning with broader sustainability goals.

Leave a Comment