-

EXECUTIVE SUMMARY

-

Key Findings

-

Market Segmentation

-

Challenges and Opportunities

-

Future

-

MARKET INTRODUCTION

-

Definition

-

Scope of the study

- Research Objective

- Assumption

- Limitations

-

RESEARCH METHODOLOGY

-

Overview

-

Secondary Research

-

Primary Research

- Breakdown of Primary

-

Forecasting Model

-

Market Size Estimation

- Top-Down Approach

-

Data Triangulation

-

Validation

-

MARKET DYNAMICS

-

Overview

-

Drivers

-

Restraints

-

Opportunities

-

MARKET

-

Value chain Analysis

-

Porter's Five Forces

- Bargaining Power of Suppliers

- Bargaining Power

- Threat of New Entrants

- Threat of Substitutes

- Intensity of Rivalry

-

COVID-19 Impact Analysis

- Regional Impact

- Opportunity and

-

RENAL CANCER DRUGS MARKET, BY THERAPEUTIC

-

Targeted Therapy

-

Immunotherapy

-

RENAL CANCER DRUGS MARKET, BY DRUG CLASS (USD BILLION)

-

Monoclonal Antibodies

-

Tyrosine Kinase Inhibitors

-

Checkpoint

-

Chemotherapeutic Agents

-

RENAL CANCER DRUGS MARKET,

-

Oral

-

Intravenous

-

Subcutaneous

-

RENAL CANCER DRUGS MARKET, BY END USER (USD BILLION)

-

Hospitals

-

Oncology Clinics

-

Research Institutions

-

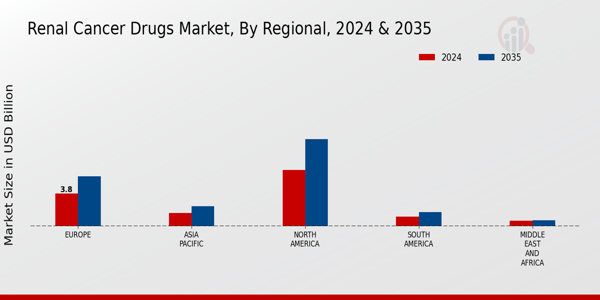

RENAL CANCER DRUGS MARKET, BY REGIONAL (USD BILLION)

-

North

- US

- Canada

-

Europe

- Germany

- UK

- France

- Russia

- Italy

- Spain

- Rest of Europe

-

APAC

- China

- India

- Japan

- South Korea

- Thailand

- Indonesia

- Rest of APAC

-

South America

- Brazil

- Mexico

- Rest of South America

-

MEA

- GCC

- South Africa

- Rest of MEA

-

COMPETITIVE LANDSCAPE

-

Overview

-

Competitive Analysis

-

Market share Analysis

-

Major Growth Strategy in the Renal

-

Competitive Benchmarking

-

Leading Players

- New Product Launch/Service

- Merger & Acquisitions

- Joint Ventures

-

Major Players Financial Matrix

- Sales and Operating Income

- Major Players R&D Expenditure. 2023

-

COMPANY PROFILES

-

Merck and Co

- Financial Overview

- Products

- Key Developments

- SWOT Analysis

-

Pfizer

- Financial Overview

- Key Developments

- SWOT Analysis

- Key Strategies

-

Ipsen

- Financial Overview

- Products Offered

- Key Developments

- SWOT Analysis

- Key Strategies

-

Roche

- Financial Overview

- Products Offered

- Key Developments

- SWOT

- Key Strategies

-

Eli Lilly

- Financial

- Products Offered

- Key Developments

- Key Strategies

-

Johnson and Johnson

- Products Offered

- Key Developments

- SWOT Analysis

- Key Strategies

-

GSK

- Products Offered

- Key Developments

- SWOT Analysis

- Key Strategies

-

Novartis

- Financial Overview

- Products Offered

- Key Developments

- SWOT Analysis

- Key Strategies

-

Exelixis

- Financial Overview

- Products Offered

- Key Developments

- SWOT Analysis

- Key Strategies

-

Teva Pharmaceuticals

- Financial Overview

- Products Offered

- SWOT Analysis

- Key Strategies

-

Bayer

- Financial Overview

- Products Offered

- Key Developments

- SWOT Analysis

- Key

-

BristolMyers Squibb

- Financial Overview

- Products Offered

- Key Developments

- SWOT

- Key Strategies

-

AstraZeneca

- Financial

- Products Offered

- Key Developments

- Key Strategies

-

Amgen

- Financial

- Products Offered

- Key Developments

- Key Strategies

-

Sanofi

- Financial

- Products Offered

- Key Developments

- Key Strategies

-

APPENDIX

-

References

-

Related Reports

-

LIST OF ASSUMPTIONS

-

NORTH AMERICA RENAL CANCER DRUGS MARKET SIZE ESTIMATES & FORECAST,

-

NORTH AMERICA RENAL

-

NORTH AMERICA RENAL CANCER DRUGS MARKET SIZE ESTIMATES

-

NORTH AMERICA RENAL CANCER DRUGS MARKET

-

US RENAL CANCER DRUGS MARKET SIZE ESTIMATES & FORECAST, BY THERAPEUTIC AREAS,

-

US RENAL CANCER DRUGS MARKET SIZE ESTIMATES

-

US RENAL

-

US RENAL CANCER DRUGS MARKET SIZE ESTIMATES &

-

US RENAL CANCER

-

CANADA RENAL CANCER DRUGS MARKET SIZE ESTIMATES & FORECAST,

-

CANADA RENAL CANCER

-

CANADA RENAL CANCER DRUGS MARKET SIZE ESTIMATES & FORECAST,

-

CANADA RENAL CANCER

-

CANADA RENAL CANCER DRUGS MARKET SIZE ESTIMATES & FORECAST,

-

EUROPE RENAL CANCER DRUGS

-

EUROPE RENAL CANCER DRUGS MARKET SIZE ESTIMATES & FORECAST,

-

EUROPE RENAL CANCER DRUGS

-

EUROPE RENAL CANCER DRUGS MARKET SIZE ESTIMATES & FORECAST,

-

EUROPE RENAL CANCER DRUGS

-

GERMANY RENAL CANCER DRUGS MARKET SIZE ESTIMATES & FORECAST, BY

-

GERMANY RENAL CANCER

-

GERMANY RENAL CANCER DRUGS MARKET SIZE ESTIMATES & FORECAST,

-

GERMANY RENAL

-

GERMANY RENAL CANCER DRUGS MARKET SIZE ESTIMATES & FORECAST,

-

UK RENAL CANCER DRUGS MARKET

-

UK RENAL CANCER DRUGS MARKET SIZE ESTIMATES & FORECAST, BY DRUG

-

UK RENAL CANCER DRUGS MARKET SIZE

-

UK RENAL CANCER DRUGS MARKET SIZE ESTIMATES & FORECAST, BY END USER,

-

UK RENAL CANCER DRUGS MARKET SIZE ESTIMATES

-

FRANCE RENAL

-

FRANCE RENAL CANCER DRUGS MARKET SIZE ESTIMATES &

-

FRANCE RENAL CANCER

-

FRANCE RENAL CANCER DRUGS MARKET SIZE ESTIMATES &

-

FRANCE RENAL CANCER

-

RUSSIA RENAL CANCER DRUGS MARKET SIZE ESTIMATES & FORECAST,

-

RUSSIA RENAL CANCER

-

RUSSIA RENAL CANCER DRUGS MARKET SIZE ESTIMATES & FORECAST,

-

RUSSIA RENAL CANCER

-

RUSSIA RENAL CANCER DRUGS MARKET SIZE ESTIMATES & FORECAST,

-

ITALY RENAL CANCER DRUGS MARKET

-

ITALY RENAL CANCER DRUGS MARKET SIZE ESTIMATES & FORECAST, BY DRUG

-

ITALY RENAL CANCER DRUGS MARKET

-

ITALY RENAL CANCER DRUGS MARKET SIZE ESTIMATES & FORECAST, BY

-

ITALY RENAL CANCER DRUGS MARKET

-

SPAIN RENAL CANCER DRUGS MARKET SIZE ESTIMATES & FORECAST, BY THERAPEUTIC

-

SPAIN RENAL CANCER DRUGS MARKET

-

SPAIN RENAL CANCER DRUGS MARKET SIZE ESTIMATES & FORECAST, BY ADMINISTRATION

-

SPAIN RENAL CANCER DRUGS MARKET

-

SPAIN RENAL CANCER DRUGS MARKET SIZE ESTIMATES & FORECAST, BY REGIONAL,

-

REST OF EUROPE RENAL CANCER DRUGS MARKET

-

REST OF EUROPE RENAL CANCER DRUGS MARKET SIZE ESTIMATES & FORECAST,

-

REST OF EUROPE RENAL CANCER

-

REST OF EUROPE RENAL CANCER DRUGS MARKET SIZE ESTIMATES

-

REST OF EUROPE

-

APAC RENAL CANCER DRUGS MARKET SIZE ESTIMATES &

-

APAC RENAL

-

APAC RENAL CANCER DRUGS MARKET SIZE ESTIMATES & FORECAST,

-

APAC RENAL CANCER

-

APAC RENAL CANCER DRUGS MARKET SIZE ESTIMATES & FORECAST, BY

-

CHINA RENAL CANCER DRUGS MARKET

-

CHINA RENAL CANCER DRUGS MARKET SIZE ESTIMATES & FORECAST, BY DRUG

-

CHINA RENAL CANCER DRUGS MARKET

-

CHINA RENAL CANCER DRUGS MARKET SIZE ESTIMATES & FORECAST, BY

-

CHINA RENAL CANCER DRUGS MARKET

-

INDIA RENAL CANCER DRUGS MARKET SIZE ESTIMATES & FORECAST, BY THERAPEUTIC

-

INDIA RENAL CANCER DRUGS MARKET

-

INDIA RENAL CANCER DRUGS MARKET SIZE ESTIMATES & FORECAST, BY ADMINISTRATION

-

INDIA RENAL CANCER DRUGS MARKET

-

INDIA RENAL CANCER DRUGS MARKET SIZE ESTIMATES & FORECAST, BY REGIONAL,

-

JAPAN RENAL CANCER DRUGS MARKET SIZE ESTIMATES

-

JAPAN

-

JAPAN RENAL CANCER DRUGS MARKET SIZE ESTIMATES &

-

JAPAN

-

JAPAN RENAL CANCER DRUGS MARKET SIZE ESTIMATES &

-

SOUTH KOREA RENAL

-

SOUTH KOREA RENAL CANCER DRUGS MARKET SIZE ESTIMATES

-

SOUTH KOREA

-

SOUTH KOREA RENAL CANCER DRUGS MARKET SIZE

-

MALAYSIA RENAL CANCER DRUGS MARKET SIZE

-

MALAYSIA RENAL CANCER DRUGS MARKET SIZE ESTIMATES & FORECAST, BY DRUG CLASS,

-

MALAYSIA RENAL CANCER DRUGS MARKET SIZE

-

MALAYSIA RENAL CANCER DRUGS MARKET SIZE ESTIMATES & FORECAST, BY

-

MALAYSIA RENAL CANCER DRUGS MARKET

-

THAILAND RENAL CANCER DRUGS MARKET SIZE ESTIMATES & FORECAST, BY THERAPEUTIC

-

THAILAND RENAL CANCER DRUGS MARKET

-

THAILAND RENAL CANCER DRUGS MARKET SIZE ESTIMATES & FORECAST, BY ADMINISTRATION

-

THAILAND RENAL CANCER DRUGS MARKET

-

THAILAND RENAL CANCER DRUGS MARKET SIZE ESTIMATES & FORECAST, BY REGIONAL,

-

INDONESIA RENAL CANCER DRUGS MARKET SIZE

-

INDONESIA RENAL CANCER DRUGS MARKET SIZE ESTIMATES & FORECAST, BY DRUG CLASS,

-

INDONESIA RENAL CANCER DRUGS MARKET SIZE

-

INDONESIA RENAL CANCER DRUGS MARKET SIZE ESTIMATES & FORECAST, BY

-

INDONESIA RENAL CANCER DRUGS

-

REST OF APAC RENAL CANCER DRUGS MARKET SIZE ESTIMATES & FORECAST,

-

REST OF APAC RENAL

-

REST OF APAC RENAL CANCER DRUGS MARKET SIZE ESTIMATES

-

REST OF APAC RENAL CANCER DRUGS MARKET

-

SOUTH AMERICA RENAL CANCER DRUGS MARKET SIZE ESTIMATES & FORECAST, BY THERAPEUTIC

-

SOUTH AMERICA RENAL CANCER DRUGS

-

SOUTH AMERICA RENAL CANCER DRUGS MARKET SIZE ESTIMATES & FORECAST,

-

SOUTH AMERICA

-

SOUTH AMERICA RENAL CANCER DRUGS MARKET SIZE ESTIMATES

-

BRAZIL RENAL

-

BRAZIL RENAL CANCER DRUGS MARKET SIZE ESTIMATES

-

BRAZIL

-

BRAZIL RENAL CANCER DRUGS MARKET SIZE

-

MEXICO RENAL CANCER DRUGS MARKET SIZE ESTIMATES

-

MEXICO RENAL CANCER DRUGS MARKET SIZE ESTIMATES

-

MEXICO RENAL CANCER DRUGS MARKET SIZE ESTIMATES

-

ARGENTINA

-

ARGENTINA RENAL CANCER DRUGS MARKET SIZE ESTIMATES

-

ARGENTINA

-

ARGENTINA RENAL CANCER DRUGS MARKET SIZE

-

REST OF SOUTH AMERICA RENAL CANCER DRUGS

-

REST OF SOUTH AMERICA RENAL CANCER DRUGS MARKET SIZE ESTIMATES

-

REST OF

-

REST OF SOUTH AMERICA RENAL CANCER

-

REST OF SOUTH AMERICA RENAL CANCER DRUGS MARKET SIZE ESTIMATES

-

MEA RENAL

-

MEA RENAL CANCER DRUGS MARKET SIZE ESTIMATES &

-

MEA RENAL CANCER

-

MEA RENAL CANCER DRUGS MARKET SIZE ESTIMATES & FORECAST,

-

MEA RENAL CANCER DRUGS MARKET

-

GCC COUNTRIES RENAL CANCER DRUGS MARKET SIZE ESTIMATES & FORECAST, BY THERAPEUTIC

-

GCC COUNTRIES RENAL CANCER DRUGS

-

GCC COUNTRIES RENAL CANCER DRUGS MARKET SIZE ESTIMATES & FORECAST,

-

GCC COUNTRIES

-

GCC COUNTRIES RENAL CANCER DRUGS MARKET SIZE ESTIMATES

-

SOUTH AFRICA

-

SOUTH AFRICA RENAL CANCER DRUGS MARKET SIZE ESTIMATES

-

SOUTH AFRICA

-

SOUTH AFRICA RENAL CANCER DRUGS MARKET

-

SOUTH AFRICA RENAL CANCER DRUGS MARKET SIZE ESTIMATES & FORECAST, BY REGIONAL,

-

REST OF MEA RENAL CANCER DRUGS MARKET

-

REST OF MEA RENAL CANCER DRUGS MARKET SIZE ESTIMATES & FORECAST,

-

REST OF MEA RENAL CANCER

-

REST OF MEA RENAL CANCER DRUGS MARKET SIZE ESTIMATES

-

REST OF MEA

-

PRODUCT LAUNCH/PRODUCT DEVELOPMENT/APPROVAL

-

ACQUISITION/PARTNERSHIP

-

MARKET SYNOPSIS

-

NORTH AMERICA RENAL CANCER DRUGS MARKET ANALYSIS

-

US RENAL CANCER DRUGS MARKET ANALYSIS BY THERAPEUTIC AREAS

-

US RENAL CANCER DRUGS MARKET ANALYSIS BY DRUG CLASS

-

US RENAL

-

US RENAL CANCER

-

US RENAL CANCER DRUGS MARKET ANALYSIS

-

CANADA RENAL CANCER DRUGS MARKET ANALYSIS BY THERAPEUTIC

-

CANADA RENAL CANCER DRUGS MARKET ANALYSIS BY DRUG CLASS

-

CANADA RENAL CANCER DRUGS MARKET ANALYSIS BY ADMINISTRATION ROUTE

-

CANADA RENAL CANCER DRUGS MARKET ANALYSIS BY END USER

-

CANADA RENAL CANCER DRUGS MARKET ANALYSIS BY REGIONAL

-

EUROPE

-

GERMANY RENAL CANCER DRUGS MARKET

-

GERMANY RENAL CANCER DRUGS MARKET

-

GERMANY RENAL CANCER DRUGS MARKET ANALYSIS

-

GERMANY RENAL CANCER DRUGS MARKET ANALYSIS

-

GERMANY RENAL CANCER DRUGS MARKET ANALYSIS BY REGIONAL

-

UK RENAL CANCER DRUGS MARKET ANALYSIS BY THERAPEUTIC AREAS

-

UK RENAL CANCER DRUGS MARKET ANALYSIS BY DRUG CLASS

-

UK

-

UK RENAL CANCER

-

FRANCE RENAL CANCER DRUGS MARKET

-

FRANCE RENAL CANCER DRUGS MARKET

-

FRANCE RENAL CANCER DRUGS MARKET ANALYSIS

-

FRANCE RENAL CANCER DRUGS MARKET ANALYSIS

-

FRANCE RENAL CANCER DRUGS MARKET ANALYSIS BY REGIONAL

-

RUSSIA RENAL CANCER DRUGS MARKET ANALYSIS BY THERAPEUTIC AREAS

-

RUSSIA RENAL CANCER DRUGS MARKET ANALYSIS BY DRUG CLASS

-

RUSSIA RENAL CANCER DRUGS MARKET ANALYSIS BY ADMINISTRATION ROUTE

-

RUSSIA RENAL CANCER DRUGS MARKET ANALYSIS BY END USER

-

RUSSIA

-

ITALY RENAL CANCER

-

ITALY RENAL CANCER DRUGS

-

ITALY RENAL CANCER DRUGS MARKET ANALYSIS

-

ITALY RENAL CANCER DRUGS MARKET ANALYSIS

-

ITALY RENAL CANCER DRUGS MARKET ANALYSIS BY REGIONAL

-

SPAIN RENAL CANCER DRUGS MARKET ANALYSIS BY THERAPEUTIC AREAS

-

SPAIN RENAL CANCER DRUGS MARKET ANALYSIS BY DRUG CLASS

-

SPAIN RENAL CANCER DRUGS MARKET ANALYSIS BY ADMINISTRATION ROUTE

-

SPAIN RENAL CANCER DRUGS MARKET ANALYSIS BY END USER

-

SPAIN

-

REST OF EUROPE RENAL

-

REST OF EUROPE

-

REST OF EUROPE

-

REST

-

REST OF

-

APAC RENAL

-

CHINA RENAL CANCER DRUGS MARKET ANALYSIS

-

CHINA RENAL CANCER DRUGS MARKET ANALYSIS BY

-

CHINA RENAL CANCER DRUGS MARKET ANALYSIS BY ADMINISTRATION

-

CHINA RENAL CANCER DRUGS MARKET ANALYSIS BY END USER

-

CHINA RENAL CANCER DRUGS MARKET ANALYSIS BY REGIONAL

-

INDIA

-

INDIA RENAL CANCER

-

INDIA RENAL CANCER

-

INDIA RENAL CANCER DRUGS MARKET

-

JAPAN RENAL CANCER DRUGS MARKET ANALYSIS BY

-

JAPAN RENAL CANCER DRUGS MARKET ANALYSIS BY DRUG

-

JAPAN RENAL CANCER DRUGS MARKET ANALYSIS BY ADMINISTRATION

-

JAPAN RENAL CANCER DRUGS MARKET ANALYSIS BY END USER

-

JAPAN RENAL CANCER DRUGS MARKET ANALYSIS BY REGIONAL

-

SOUTH KOREA RENAL CANCER DRUGS MARKET ANALYSIS BY DRUG CLASS

-

SOUTH KOREA RENAL CANCER DRUGS MARKET ANALYSIS BY END USER

-

MALAYSIA

-

MALAYSIA

-

MALAYSIA RENAL

-

MALAYSIA RENAL

-

MALAYSIA RENAL CANCER

-

THAILAND RENAL CANCER DRUGS MARKET

-

THAILAND RENAL CANCER DRUGS MARKET

-

THAILAND RENAL CANCER DRUGS MARKET ANALYSIS

-

THAILAND RENAL CANCER DRUGS MARKET ANALYSIS

-

THAILAND RENAL CANCER DRUGS MARKET ANALYSIS BY REGIONAL

-

INDONESIA RENAL CANCER DRUGS MARKET ANALYSIS BY THERAPEUTIC AREAS

-

INDONESIA RENAL CANCER DRUGS MARKET ANALYSIS BY DRUG CLASS

-

INDONESIA RENAL CANCER DRUGS MARKET ANALYSIS BY ADMINISTRATION ROUTE

-

INDONESIA RENAL CANCER DRUGS MARKET ANALYSIS BY END USER

-

INDONESIA RENAL CANCER DRUGS MARKET ANALYSIS BY REGIONAL

-

REST

-

REST

-

REST OF APAC RENAL CANCER DRUGS MARKET ANALYSIS BY END USER

-

SOUTH

-

BRAZIL RENAL CANCER

-

BRAZIL RENAL CANCER

-

BRAZIL RENAL CANCER DRUGS MARKET

-

BRAZIL RENAL CANCER DRUGS MARKET

-

BRAZIL RENAL CANCER DRUGS MARKET ANALYSIS

-

MEXICO RENAL CANCER DRUGS MARKET ANALYSIS BY THERAPEUTIC

-

MEXICO RENAL CANCER DRUGS MARKET ANALYSIS BY DRUG CLASS

-

MEXICO RENAL CANCER DRUGS MARKET ANALYSIS BY ADMINISTRATION ROUTE

-

MEXICO RENAL CANCER DRUGS MARKET ANALYSIS BY END USER

-

MEXICO RENAL CANCER DRUGS MARKET ANALYSIS BY REGIONAL

-

ARGENTINA

-

ARGENTINA

-

ARGENTINA RENAL

-

ARGENTINA

-

ARGENTINA RENAL

-

REST OF SOUTH AMERICA

-

REST OF

-

REST OF SOUTH AMERICA RENAL CANCER DRUGS MARKET ANALYSIS BY END

-

REST OF SOUTH AMERICA RENAL CANCER DRUGS MARKET ANALYSIS

-

MEA RENAL CANCER DRUGS MARKET ANALYSIS

-

GCC COUNTRIES RENAL CANCER DRUGS MARKET ANALYSIS BY THERAPEUTIC AREAS

-

GCC COUNTRIES RENAL CANCER DRUGS MARKET ANALYSIS BY DRUG CLASS

-

GCC COUNTRIES RENAL CANCER DRUGS MARKET ANALYSIS BY ADMINISTRATION ROUTE

-

GCC COUNTRIES RENAL CANCER DRUGS MARKET ANALYSIS BY END USER

-

GCC COUNTRIES RENAL CANCER DRUGS MARKET ANALYSIS BY REGIONAL

-

SOUTH AFRICA RENAL CANCER DRUGS MARKET ANALYSIS BY DRUG CLASS

-

SOUTH AFRICA RENAL CANCER DRUGS MARKET ANALYSIS BY ADMINISTRATION ROUTE

-

SOUTH AFRICA RENAL CANCER DRUGS MARKET ANALYSIS BY END USER

-

SOUTH AFRICA RENAL CANCER DRUGS MARKET ANALYSIS BY REGIONAL

-

REST OF MEA RENAL CANCER DRUGS MARKET ANALYSIS BY DRUG CLASS

-

REST OF MEA RENAL CANCER DRUGS MARKET ANALYSIS BY END USER

-

KEY

-

RESEARCH PROCESS

-

DRO ANALYSIS OF RENAL CANCER DRUGS MARKET

-

DRIVERS IMPACT ANALYSIS: RENAL CANCER DRUGS MARKET

-

RESTRAINTS

-

SUPPLY / VALUE CHAIN:

-

RENAL CANCER DRUGS MARKET, BY THERAPEUTIC

-

RENAL CANCER DRUGS MARKET, BY THERAPEUTIC

-

RENAL CANCER DRUGS MARKET,

-

RENAL CANCER DRUGS MARKET, BY DRUG

-

RENAL CANCER DRUGS MARKET,

-

RENAL CANCER DRUGS MARKET,

-

RENAL CANCER

-

RENAL CANCER DRUGS MARKET,

-

RENAL CANCER DRUGS MARKET,

-

RENAL CANCER DRUGS MARKET, BY REGIONAL,

-

TO 2035 (USD Billions)

-

BENCHMARKING OF MAJOR COMPETITORS

Leave a Comment