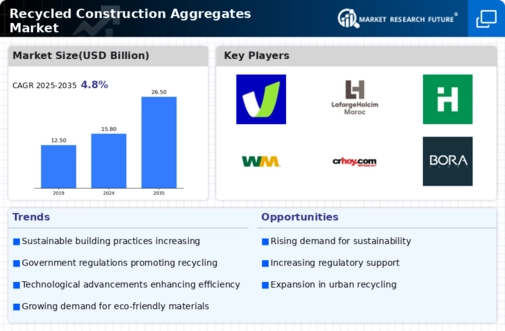

Top Industry Leaders in the Recycled Construction Aggregates Market

The construction industry is a major contributor to global waste generation, producing millions of tons of debris annually. However, a revolution is brewing within this sector, one that prioritizes sustainability and resource conservation: the recycled construction aggregates market. This dynamic market, is attracting a diverse range of players, all vying to transform construction waste into valuable resources. Let's delve into the strategies shaping this landscape, explore the factors influencing market share, and unveil the recent developments propelling recycled aggregates towards a sustainable future.

The construction industry is a major contributor to global waste generation, producing millions of tons of debris annually. However, a revolution is brewing within this sector, one that prioritizes sustainability and resource conservation: the recycled construction aggregates market. This dynamic market, is attracting a diverse range of players, all vying to transform construction waste into valuable resources. Let's delve into the strategies shaping this landscape, explore the factors influencing market share, and unveil the recent developments propelling recycled aggregates towards a sustainable future.

Strategies Paving the Way to Sustainable Construction:

-

Product Diversification: Leading companies like CRH and Holcim are expanding beyond traditional crushed concrete offerings, venturing into processed asphalt, brick, and even glass aggregates, catering to specialized construction needs. -

Technological Advancements: Pioneering innovations like advanced sorting and processing technologies, mobile crushing units, and even AI-powered quality control systems, as seen in AMP Robotics' offerings, are optimizing efficiency and maximizing resource recovery. -

Sustainability Focus: Utilizing eco-friendly practices like reducing water usage in processing, minimizing dust emissions, and offering carbon-neutral transportation, as seen in CEMEX's initiatives, are becoming crucial for responsible market growth. -

Regional Expansion and Localization: Entering high-growth markets like India and China, coupled with adapting products to local regulations and construction practices, is key to success. Larsen & Toubro's strong presence in Asia exemplifies this approach. -

Strategic Partnerships and Collaborations: Collaborations with demolition companies, waste management firms, and government agencies enhance access to materials, secure contracts, and promote wider adoption of recycled aggregates. LafargeHolcim's partnerships with waste management firms showcase this strategy.

Factors Forging Market Share Fortresses:

-

Brand Reputation and Quality: Established brands with a long history of quality and performance, like Oldcastle Materials and Eurovia, hold an edge over newer entrants. -

Production Capacity and Distribution Network: Extensive processing facilities and efficient distribution networks ensure timely delivery and cost-effectiveness, giving established players like Martin Marietta Materials a competitive advantage. -

Innovation and Technological Prowess: Pioneering new processing methods, developing alternative recycled materials like construction and demolition wood, and even integrating recycled aggregates into precast concrete products, as seen in TecEco's offerings, fosters market distinction. -

Price Competitiveness and Regional Considerations: Cost-effective options for mass markets in emerging economies like India and China can offer companies like Hanson an edge. -

Marketing and Customer Service: Engaging marketing campaigns highlighting the environmental and economic benefits of recycled aggregates, coupled with impeccable customer service, are crucial for brand loyalty and repeat business. CRH's focus on customer service sets them apart.

Key Players

- Delta Sand & Gravel (US)

- Heidelbergcement AG (Germany)

- Aggregate Industries Management Inc. (US)

- Green Stone Materials (US)

- CEMEX (Mexico)

- LafargeHolcim Ltd (Switzerland)

Recent Developments

-

October 2023: The European Union announces new regulations mandating higher recycled content in construction projects, further boosting the market in the region. -

November 2023: A major infrastructure project utilizes predominantly recycled aggregates, setting a precedent for large-scale adoption in public works. -

December 2023: A consortium of recycled aggregate companies launches a research initiative focused on developing new applications for recycled materials in innovative construction products.