-

EXECUTIVE SUMMARY

-

MARKET INTRODUCTION

-

DEFINITION

-

SCOPE OF THE STUDY

-

RESEARCH

-

OBJECTIVE

-

MARKET STRUCTURE

-

RESEARCH METHODOLOGY

-

OVERVIEW

-

DATA FLOW

- DATA MINING PROCESS

-

PURCHASED DATABASE:

-

SECONDARY SOURCES:

-

SECONDARY RESEARCH DATA FLOW:

-

PRIMARY RESEARCH:

- PRIMARY RESEARCH DATA FLOW:

- PRIMARY RESEARCH: NUMBER OF INTERVIEWS

-

CONDUCTED

-

PRIMARY RESEARCH: REGIONAL COVERAGE

-

APPROACHES FOR

-

MARKET SIZE ESTIMATION:

-

REVENUE ANALYSIS APPROACH

-

DATA FORECASTING

- DATA FORECASTING TECHNIQUE

-

DATA MODELING

- MICROECONOMIC

-

FACTOR ANALYSIS:

-

DATA MODELING:

-

TEAMS AND ANALYST CONTRIBUTION

-

MARKET DYNAMICS

-

INTRODUCTION

-

DRIVERS

- GROWTH OF E-COMMERCE

-

AND ONLINE RETAILING

-

SUSTAINABILITY AND ECO-FRIENDLY PACKAGING

-

TECHNOLOGICAL ADVANCEMENTS IN PACKAGING

-

CONSUMER PREFERENCE FOR CONVENIENCE

- REGULATORY COMPLIANCE AND SAFETY STANDARDS

- DRIVER IMPACT ANALYSIS

-

RESTRAINTS

- HIGH COST OF SUSTAINABLE MATERIAL

- LIMITED

-

CONSUMER AWARENESS OF INNOVATIVE PACKAGING SOLUTIONS

-

STRINGENT REGULATIONS

-

ON PACKAGING WASTE MANAGEMENT

-

RESTRAINT IMPACT ANALYSIS

-

OPPORTUNITY

- EXPANSION OF BIODEGRADABLE MATERIALS

- GROWTH IN E-COMMERCE SUBSCRIPTION

-

SERVICES

-

INTEGRATION OF SMART PACKAGING SOLUTIONS

- INCREASE

-

IN REGIONAL SUPPLY CHAIN OPTIMIZATION

-

RISING DEMAND FOR CUSTOMIZABLE

-

PACKAGING SOLUTIONS

-

IMPACT ANALYSIS OF COVID - 19

- IMPACT ON

-

OVERALL PACKAGING AND TRANSPORTATION

-

IMPACT ON NORTH AMERICA PACKAGING

-

MARKET

-

IMPACT ON SUPPLY CHAIN OF PACKAGING MARKET

- IMPACT ON

-

MARKET DEMAND OF PACKAGING MARKET

-

IMPACT ON PRICING OF PACKAGING MARKET

-

MARKET FACTOR ANALYSIS

-

PORTER’S FIVE FORCES MODEL

- THREAT

-

OF NEW ENTRANTS

-

BARGAINING POWER OF SUPPLIERS

- BARGAINING POWER

-

OF BUYERS

-

THREAT OF SUBSTITUTES

- INTENSITY OF RIVALRY

-

SUPPLY CHAIN ANALYSIS

-

RAW MATERIAL PROCUREMENT

- MANUFACTURING

- DISTRIBUTORS AND LOGISTICS

- END-USER INDUSTRIES

-

NORTH

-

AMERICA PACKAGING MARKET, BY DISTRIBUTION CHANNEL

-

OVERVIEW

-

DIRECT

-

FROM MANUFACTURER

-

DISTRIBUTOR-DRIVEN SALES

-

NORTH AMERICA PACKAGING

-

MARKET, BY PACKAGING MATERIAL

-

OVERVIEW

-

PLASTIC

-

PAPER

-

PACKAGING

-

METAL

-

GLASS PACKAGING

-

OTHERS

-

NORTH

-

AMERICA PACKAGING MARKET, BY PACKAGING TYPE

-

OVERVIEW

-

PRIMARY PACKAGING

-

SECONDARY PACKAGING

-

TERTIARY PACKAGING

-

OTHERS

-

NORTH AMERICA PACKAGING MARKET, BY APPLICATION END USE INDUSTRY

-

OVERVIEW

-

FOOD & BEVERAGE PACKAGING

-

PHARMACEUTICALS

-

COSMETICS

-

& PERSONAL CARE PACKAGING

-

INDUSTRIAL GOODS

-

OTHERS

-

NORTH AMERICA PACKAGING MARKET, BY BUYER TYPE

-

OVERVIEW

-

SMALL

-

AND MEDIUM ENTERPRISES

-

LARGE ENTERPRISES

-

RETAIL CONSUMERS

-

OTHERS

-

NORTH AMERICA PACKAGING MARKET, BY COUNTRY

-

OVERVIEW

-

NORTH AMERICA PACKAGING MARKET, BY COUNTRY, 2019–2035

-

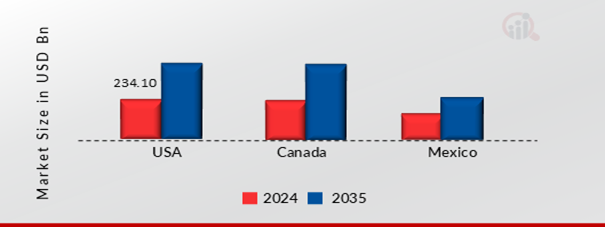

USA

-

CANADA

-

MEXICO

-

COMPETITIVE LANDSCAPE

-

INTRODUCTION

-

COMPETITOR DASHBOARD

-

THE LEADING PLAYER

-

IN TERMS OF THE NUMBER OF RECENT DEVELOPMENTS IN THE MARKET

-

KEY DEVELOPMENTS

-

& GROWTH STRATEGIES

-

PRODUCT LAUNCH

- PARTNERSHIP, COLLABORATION

-

AND AGREEMENT

-

ACQUISITION & MERGER

- EXPANSION

-

OTHERS

-

COMPANY PROFILES

-

CENTRAL NATIONAL GOTTESMAN INC. (CNG)

- COMPANY OVERVIEW

- FINANCIAL OVERVIEW

- PRODUCTS OFFERED

- KEY DEVELOPMENTS

- SWOT ANALYSIS

- KEY STRATEGIES

-

VERITIV CORPORATION

- COMPANY OVERVIEW

- FINANCIAL OVERVIEW

- PRODUCTS OFFERED

- KEY DEVELOPMENTS

- SWOT ANALYSIS

- KEY STRATEGIES

-

CLASSIC PACKAGING CORPORATION

- COMPANY

-

OVERVIEW

-

FINANCIAL OVERVIEW

- PRODUCTS OFFERED

-

KEY DEVELOPMENTS

-

SWOT ANALYSIS

- KEY STRATEGIES

-

SOUTHERN PACKAGING, LP

-

COMPANY OVERVIEW

- FINANCIAL OVERVIEW

- PRODUCTS OFFERED

- KEY DEVELOPMENTS

- SWOT ANALYSIS

- KEY STRATEGIES

-

TRICORBRAUN

- COMPANY OVERVIEW

-

FINANCIAL OVERVIEW

-

PRODUCTS OFFERED

- KEY DEVELOPMENTS

- SWOT ANALYSIS

- KEY STRATEGIES

-

PANTHEON PACKAGING

- COMPANY OVERVIEW

- FINANCIAL OVERVIEW

- PRODUCTS OFFERED

- KEY DEVELOPMENTS

- SWOT ANALYSIS

- KEY STRATEGIES

-

S&S INCORPORATED

- COMPANY OVERVIEW

- FINANCIAL OVERVIEW

- PRODUCTS OFFERED

- KEY DEVELOPMENTS

- SWOT ANALYSIS

- KEY STRATEGIES

-

LES EMBALLAGES CARROUSEL INC.

- COMPANY

-

OVERVIEW

-

FINANCIAL OVERVIEW

- PRODUCTS OFFERED

-

KEY DEVELOPMENTS

-

SWOT ANALYSIS

- KEY STRATEGIES

-

CANPACO INC.

-

COMPANY OVERVIEW

- FINANCIAL OVERVIEW

-

PRODUCTS OFFERED

-

KEY DEVELOPMENTS

- SWOT ANALYSIS

-

KEY STRATEGIES

-

KYANA PACKAGING & INDUSTRIAL SUPPLY

- COMPANY

-

OVERVIEW

-

FINANCIAL OVERVIEW

- PRODUCTS OFFERED

-

KEY DEVELOPMENTS

-

SWOT ANALYSIS

- KEY STRATEGIES

-

LIST

-

OF TABLES

-

NORTH AMERICA: PACKAGING MARKET, BY DISTRIBUTION CHANNEL, 2019–2035 (USD

-

BILLION)

-

(USD BILLION)

-

(USD BILLION)

-

–2035 (USD BILLION)

-

TYPE, 2019–2035 (USD BILLION)

-

BY COUNTRY, 2019–2035 (USD BILLION)

-

DISTRIBUTION CHANNEL, 2019–2035 (USD BILLION)

-

MARKET, BY PACKAGING MATERIALS 2019–2035 (USD BILLION)

-

PACKAGING MARKET, BY PACKAGING TYPE, 2019–2035 (USD BILLION)

-

USA: PACKAGING MARKET, BY END USE INDUSTRY, 2019–2035 (USD BILLION)

-

USA: PACKAGING MARKET, BY BUYER TYPE, 2019–2035 (USD BILLION)

-

CANADA: PACKAGING MARKET, BY DISTRIBUTION CHANNEL, 2019–2035 (USD BILLION)

-

BILLION)

-

(USD BILLION)

-

(USD BILLION)

-

(USD BILLION)

-

(USD BILLION)

-

(USD BILLION)

-

(USD BILLION)

-

(USD BILLION)

-

(USD BILLION)

-

NATIONAL GOTTESMAN INC.: KEY DEVELOPMENTS

-

OFFERED

-

PACKAGING CORPORATION: PRODUCTS OFFERED

-

OFFERED

-

DEVELOPMENTS

-

INCORPORATED: PRODUCTS OFFERED

-

OFFERED

-

CANPACO INC.: PRODUCTS OFFERED

-

LIST

-

OF FIGURES

-

MARKET DYNAMICS: NORTH AMERICA PACKAGING MARKET

-

NORTH AMERICA PACKAGING MARKET

-

PACKAGING MARKET

-

PACKAGING MARKET

-

(USD BILLION)

-

(% SHARE)

-

–2035 (USD BILLION)

-

PACKAGING TYPE, 2024 (% SHARE)

-

PACKAGING TYPE, 2019–2035 (USD BILLION)

-

MARKET, BY END USE INDUSTRY, 2024 (% SHARE)

-

MARKET, BY END USE INDUSTRY, 2019–2035 (USD BILLION)

-

AMERICA PACKAGING MARKET, BY BUYER TYPE, 2024 (% SHARE)

-

PACKAGING MARKET, BY BUYER TYPE, 2019–2035 (USD BILLION)

-

AMERICA PACKAGING MARKET, BY COUNTRY, 2024 (% SHARE)

-

NORTH AMERICA PACKAGING MARKET

-

ANALYSIS

-

PACKAGING CORPORATION: SWOT ANALYSIS

-

ANALYSIS

-

SWOT ANALYSIS

-

LES EMBALLAGES CARROUSEL INC.: SWOT ANALYSIS