In Vehicle Wireless Charging Size

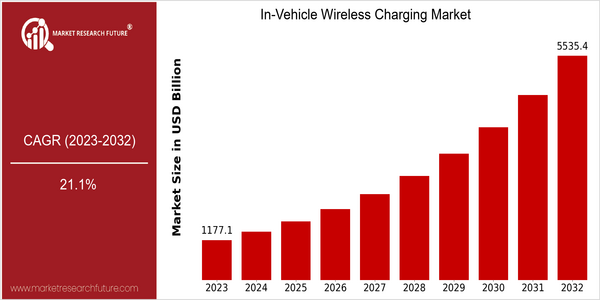

Market Size Snapshot

| Year | Value |

|---|---|

| 2023 | USD 1177.1 Billion |

| 2032 | USD 5535.4 Billion |

| CAGR (2023-2032) | 21.1 % |

Note – Market size depicts the revenue generated over the financial year

In-Vehicle Wireless Charging Market is set for significant growth, with a market size of $1,177.9 billion in 2023, and is projected to reach $ 55,355.40 billion by 2032. The CAGR of this market is 21.1 % over the forecast period. The increasing integration of advanced technology in vehicles and the growing demand for convenience and efficiency in charging solutions are driving the market growth. The growing popularity of electric vehicles is expected to increase the demand for new charging methods, such as wireless charging, which will also boost the market growth. The key factors driving the market growth are the advancements in wireless power transfer technology, the proliferation of smart devices, and the growing demand for a seamless charging experience. These factors are driving the R&D activities of key players, such as Qualcomm, BMW, and Toyota, to develop advanced wireless charging solutions. Strategic alliances and collaborations are also defining the market landscape. This market is expected to play a significant role in the future of mobility.

Regional Market Size

Regional Deep Dive

The In-Vehicle Wireless Charging Market is expected to grow at a CAGR of over 12% by 2023, driven by the increasing demand for convenience and technological advancements in the field of automobile design. North America is characterized by the high penetration of electric vehicles and the luxury segment, which is often characterized by advanced technology integration. Europe is seeing the rise of regulatory support for electric mobility. Asia-Pacific is a fast-growing market for the manufacture of electric vehicles. The Middle East and Africa are gradually catching up, influenced by the growing automotive industry and the increasing demand for advanced features. Latin America is still in the process of development, but is expected to grow due to rising incomes and the growing demand for smart mobility.

Europe

- The European Union has introduced regulations aimed at reducing carbon emissions, which is pushing automakers to adopt electric vehicles equipped with wireless charging capabilities.

- Companies like BMW and Audi are investing heavily in research and development for wireless charging systems, indicating a strong commitment to innovation in this space.

Asia Pacific

- China is leading the charge in the adoption of wireless charging technology, with companies like BYD and NIO developing advanced systems for their electric vehicles.

- The region is witnessing collaborations between automotive manufacturers and tech companies, such as the partnership between Toyota and WiTricity, to enhance wireless charging solutions.

Latin America

- Brazil is seeing an increase in electric vehicle adoption, with local startups exploring wireless charging solutions to meet the needs of urban consumers.

- Government incentives for electric vehicles in countries like Chile are encouraging automakers to consider wireless charging as a viable feature in their offerings.

North America

- Major automotive manufacturers like Tesla and General Motors are integrating wireless charging technology into their new models, enhancing consumer convenience and driving market growth.

- The U.S. Department of Energy has launched initiatives to promote electric vehicle infrastructure, including wireless charging stations, which is expected to accelerate the adoption of this technology.

Middle East And Africa

- The UAE is investing in smart city initiatives that include the development of wireless charging infrastructure for electric vehicles, reflecting a commitment to sustainable transportation.

- Local automotive companies are beginning to explore partnerships with international tech firms to integrate wireless charging solutions into their vehicles, indicating a growing interest in modern automotive technologies.

Did You Know?

“Approximately 70% of consumers express a preference for wireless charging capabilities in their next vehicle, highlighting the growing demand for convenience in automotive technology.” — Consumer Insights Report 2023

Segmental Market Size

In-vehicle wireless charging is a rapidly growing market, mainly driven by the growing demand for convenience and improved experience in the automotive industry. In addition, the popularity of electric vehicles is also a major driving force for this market. Moreover, the government's policy of promoting the construction of a national charging grid has further increased the demand for wireless charging systems. In the current market, the market is in the stage of mass production, and in the European and American markets, BMW and Tesla have been the first to launch wireless charging models. In the application, in-vehicle wireless charging mainly refers to passenger vehicles, fleet management and public transportation, where the technology can improve the efficiency and convenience of the operation and increase the satisfaction of the use. The trend of the future is that the trend of reducing the carbon footprint of vehicles and the trend of integrating smart devices into vehicles will accelerate the growth of this market. The development trend of the industry is that the magnetic resonance induction charging and resonant induction charging will be widely used, which will have a greater energy transfer efficiency and be more compatible with various vehicle models.

Future Outlook

The market for in-vehicle wireless charging will be worth $1,175,100,000 in 2023 and $ 5,503,400,800 in 2032. The compound annual growth rate of this market is 21.1%. This growth is driven by the growing adoption of electric vehicles (EVs) and the development of wireless charging technology, which has become an essential feature of modern vehicle design. In the future, the penetration of wireless charging in new car models will reach about 30%, compared to about 10% in 2023. In the future, technological advances such as increased power transfer efficiency and the development of standardized charging methods will help to increase the appeal of in-vehicle wireless charging solutions. The government's encouragement of EVs and the reduction of carbon dioxide emissions will also drive market growth. Emerging trends such as the integration of smart charging solutions and the development of charging infrastructure will also have a significant impact on the market. During this time, the market for in-vehicle wireless charging will be an important part of the evolution of the automotive industry.

Leave a Comment