Green steel Market Trends

ID: MRFR/CnM/9766-HCR

128 Pages

September 2025

Green Steel Market Research Report By Method of Production (Hydrogen-Based Reduction, Electrolysis, Biomass Direct Reduction, Recycling), By End Use Industry (Construction, Automotive, Manufacturing, Energy), By Form (Flat Steel, Long Steel, Steel Products), By Quality Grade (High Strength Steel, Low Alloy Steel, Stainless Steel) and By Regional (North America, Europe, South America, Asia Pacif...

Market Summary

As per Market Research Future Analysis, the Global Green Steel Market is poised for substantial growth, driven by increasing environmental regulations and rising demand from the automotive and construction sectors. The market size was estimated at 0.87 USD Billion in 2024 and is projected to reach 3480.06 USD Billion by 2035, reflecting a compound annual growth rate (CAGR) of approximately 29.49% from 2025 to 2035. Key technological innovations, such as hydrogen-based reduction and recycling methods, are enhancing production efficiency and sustainability.

Key Market Trends & Highlights

The Global Green Steel Market is witnessing transformative trends focused on sustainability and innovation.

- Market Size in 2024: 0.87 USD Billion; expected to grow to 50 USD Billion by 2035.

- Hydrogen-Based Reduction method projected to grow from 0.91 USD Billion in 2024 to 15.0 USD Billion by 2035.

- Electric vehicles expected to account for 30% of all vehicle sales by 2030, driving green steel demand.

- Europe's market valuation in 2024: 1.2 USD Billion; anticipated to reach 20.0 USD Billion by 2035.

Market Size & Forecast

| 2024 Market Size | USD 0.87 Billion |

| 2035 Market Size | USD 3480.06 Billion |

| CAGR (2025-2035) | 1.13% |

| Largest Regional Market Share in 2024 | Europe. |

Major Players

Key companies include Boston Metal, Nucor, ClevelandCliffs, POSCO, Voestalpine, SSAB, Tata Steel, Severstal, Thyssenkrupp, United States Steel, Salzgitter AG, ArcelorMittal, H2 Green Steel.

Market Trends

The Green Steel Market is experiencing significant growth driven by increasing environmental regulations and the urgent need to reduce carbon emissions in steel production. Governments worldwide are pushing for greener manufacturing processes, and steel producers are responding by investing in technologies that promote sustainability, such as hydrogen-based steelmaking. This shift is driven by a growing awareness of climate change and its impact on health and the environment, pushing companies to adopt cleaner alternatives.

Additionally, the demand for green steel is rising due to the automotive and construction industries prioritizing sustainable materials to meet consumer expectations for environmentally friendly products.Opportunities to be explored in this market include advances in carbon capture and storage technologies, as well as the potential for recycling scrap steel, which can reduce the reliance on virgin iron ore. Developing countries, in particular, can benefit from investing in green steel technologies, thus creating an avenue for economic growth and job creation in sustainable sectors.

The future of the Green Steel Market looks promising, supported by policy incentives and growing consumer demand for sustainable solutions.

The transition towards green steel production is poised to reshape the global steel industry, driven by increasing regulatory pressures and a growing demand for sustainable practices across various sectors.

U.S. Department of Energy

Green steel Market Market Drivers

Market Growth Projections

The Global Green Steel Market Industry is projected to experience remarkable growth, with estimates suggesting a market value of 50 USD Billion by 2035. This anticipated expansion is driven by various factors, including rising demand for sustainable products, government regulations, and technological advancements. The industry is expected to witness a compound annual growth rate of 29.5% from 2025 to 2035, indicating a robust trajectory. As stakeholders increasingly recognize the importance of sustainable practices, the green steel sector is likely to play a crucial role in the global transition towards a low-carbon economy.

Government Regulations and Incentives

Government regulations play a pivotal role in shaping the Global Green Steel Market Industry. Many countries are implementing stringent emissions standards and offering incentives for companies that adopt greener practices. For instance, initiatives aimed at reducing carbon emissions are encouraging steel manufacturers to invest in green technologies. Such policies not only promote the use of green steel but also create a competitive advantage for compliant firms. As the regulatory landscape evolves, it is likely that the market will expand, with projections indicating a growth trajectory that could reach 50 USD Billion by 2035. This regulatory push underscores the importance of aligning with environmental goals.

Investment in Renewable Energy Sources

Investment in renewable energy sources is becoming increasingly critical for the Global Green Steel Market Industry. The integration of renewable energy into steel production processes can drastically lower carbon emissions, making green steel more competitive. As companies seek to transition away from fossil fuels, the reliance on solar, wind, and hydropower is expected to rise. This shift not only supports sustainability goals but also aligns with global energy trends. The growing emphasis on renewable energy solutions indicates a promising future for the green steel sector, as it positions itself as a key player in the broader transition to a low-carbon economy.

Rising Demand for Sustainable Products

The Global Green Steel Market Industry experiences a notable surge in demand for sustainable products as consumers and industries increasingly prioritize environmental responsibility. This shift is reflected in the growing adoption of green steel, which is produced with significantly lower carbon emissions compared to traditional methods. As of 2024, the market is valued at approximately 2.91 USD Billion, indicating a robust interest in eco-friendly alternatives. Industries such as automotive and construction are leading the charge, seeking to reduce their carbon footprints. This trend suggests that the Global Green Steel Market Industry is poised for substantial growth as sustainability becomes a core value across sectors.

Technological Advancements in Steel Production

Technological advancements are transforming the Global Green Steel Market Industry, enabling more efficient and sustainable production methods. Innovations such as hydrogen-based direct reduction processes and electric arc furnaces are gaining traction, significantly reducing the carbon intensity of steel production. These technologies not only enhance productivity but also align with global sustainability goals. As manufacturers adopt these cutting-edge techniques, the market is expected to witness a compound annual growth rate of 29.5% from 2025 to 2035. This rapid technological evolution indicates a shift towards a more sustainable steel industry, positioning green steel as a viable alternative in the global market.

Consumer Awareness and Corporate Responsibility

Consumer awareness regarding environmental issues is driving the Global Green Steel Market Industry towards more sustainable practices. As consumers become more informed about the impacts of their purchasing decisions, they increasingly favor products made from green steel. This shift is prompting companies to adopt corporate responsibility initiatives that prioritize sustainability in their supply chains. The growing demand for transparency and eco-friendly products is likely to influence manufacturers to invest in green steel technologies. As a result, the market is expected to expand significantly, reflecting a broader societal shift towards sustainability and responsible consumption.

Market Segment Insights

Green Steel Market Method of Production Insights

The Method of Production segment of the Green Steel Market is poised for significant development, showcasing diverse approaches such as Hydrogen-Based Reduction, Electrolysis, Biomass Direct Reduction, and Recycling. The overall market in 2024 is valued at 2.91 USD Billion and is expected to witness robust growth by 2035, reaching 50.0 USD Billion.

In 2024, the Hydrogen-Based Reduction segment holds a valuation of 1.2 USD Billion, reflecting its strong potential and increasing adoption as industries seek cleaner alternatives for steel production.By 2035, this segment is expected to lead with a valuation of 20.0 USD Billion, giving it a majority holding in the Green Steel Market. This method is considered significant due to its lower carbon emissions compared to traditional processes, which aligns with sustainability goals. Electrolysis, another key method, is valued at 0.85 USD Billion in 2024 and is projected to achieve 15.0 USD Billion by 2035.

This technology utilizes electricity to split water into hydrogen and oxygen, which is then applied in steel production, further enhancing its appeal amid the renewable energy push.Biomass Direct Reduction, with a valuation of 0.45 USD Billion in 2024, is anticipated to grow to 8.0 USD Billion by 2035. This method leverages organic materials to reduce iron ore into iron, contributing significantly to the circular economy by utilizing waste products. Lastly, the Recycling method, valued at 0.41 USD Billion in 2024, is expected to reach 7.0 USD Billion in 2035.

While it represents the least dominant segment, its importance cannot be overlooked as recycling steel greatly reduces energy consumption and greenhouse gas emissions.These insights reflect the underlying trends and market dynamics of the Green Steel Market, where sustainability and innovative production methods play a crucial role in shaping the future of steel manufacturing.

Source: Primary Research, Secondary Research, Market Research Future Database and Analyst Review

Green Steel Market End Use Industry Insights

The Green Steel Market, which is set to be valued at 2.91 USD Billion in 2024, showcases a significant expansion driven by the increasing demand in the End Use Industry. The construction sector plays a crucial role, as it increasingly adopts green steel to meet sustainability goals and reduce carbon footprints. The automotive industry is also witnessing a strong shift, with manufacturers prioritizing lightweight and eco-friendly materials to enhance fuel efficiency.

In manufacturing, green steel is essential for the production of machinery and components, aligning with the trend towards decarbonization.Energy applications of green steel are significant as well, particularly in renewable energy infrastructure, supporting the shift towards clean energy sources. The overall market growth is supported by rising environmental regulations and the urgency to mitigate climate change impacts, providing ample opportunities across these sectors. As the focus on sustainability deepens, green steel is expected to gain the majority holding, particularly in the construction and automotive industries, making it a pivotal element in the transition toward a greener future.

Green Steel Market Form Insights

The Green Steel Market, focusing on the Form segment, has been experiencing notable growth, with significant contributions from various categories such as Flat Steel, Long Steel, and Steel Products. By 2024, this market is expected to be valued at 2.91 USD Billion and is projected to witness an increase to 50.0 USD Billion by 2035. Flat Steel is essential due to its versatility and application across the automotive and construction industries, supporting the shift towards sustainable practices in these sectors.

Long Steel plays a crucial role in infrastructure development, catering to the demands for eco-friendly building solutions.Steel Products encompasses a range of items that aid in the production of innovative and efficient applications, aligning with sustainability efforts. The Green Steel Market segmentation indicates a strong consumer preference for low-carbon steel solutions, driven by rising environmental regulations and growing awareness of climate change.

This market growth is further supported by advancements in technology aimed at reducing emissions, thus presenting numerous opportunities while also facing challenges related to production costs and raw material availability.Overall, the market data reflects a robust potential for expansion in the Green Steel industry, demonstrating significant shifts towards greener alternatives and increased demand for sustainable steel forms.

Green Steel Market Quality Grade Insights

The Green Steel Market is witnessing significant growth, particularly in the Quality Grade segment. By 2024, the market is valued at 2.91 USD Billion and is expected to rise substantially in the coming years. This segment encompasses various grades of steel, including High Strength Steel, Low Alloy Steel, and Stainless Steel, which are critical in meeting the evolving demands for sustainability and performance in industrial applications.

High Strength Steel is gaining traction due to its lightweight and high durability, making it vital for industries such as automotive and construction.Low Alloy Steel plays a crucial role in enhancing strength and toughness while maintaining low costs, appealing to manufacturers looking for efficient production methods. Stainless Steel, known for its corrosion resistance and longevity, remains significant for sectors requiring reliable materials, such as food and pharmaceuticals. The Green Steel Market revenues and segmentation underscore a robust market growth trajectory driven by increasing investments in sustainable practices and the adoption of advanced technologies.

Market challenges include the need for improved production methods to enhance efficiency while maintaining environmental benefits, presenting opportunities for innovation in this sector.Overall, the Quality Grade segment is poised to shape the Green Steel Market landscape as industries transition towards greener solutions.

Get more detailed insights about Green Steel Market Research Report - Global Forecast 2035

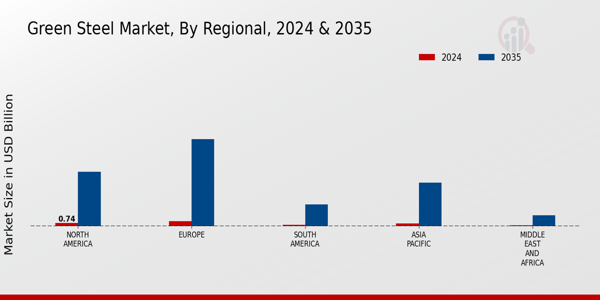

Regional Insights

The 'Green Steel Market' is projected to witness significant growth across various regions, with a valuation of 2.91 USD Billion in 2024 and expected to reach 50.0 USD Billion by 2035. North America is expected to hold a major portion, valued at 0.74 USD Billion in 2024, rising to 12.5 USD Billion in 2035, driven by a surge in eco-friendly initiatives and technological advancements.

Europe follows closely, with a valuation of 1.1 USD Billion in 2024, anticipated to reach 20.0 USD Billion by 2035, emphasizing the region's strong commitment to sustainable practices.Asia Pacific is also significant, valued at 0.61 USD Billion in 2024, and projected to grow to 10.0 USD Billion by 2035, benefiting from increased demand for green steel in rapidly industrializing economies.

Meanwhile, South America and the Middle East and Africa report valuations of 0.29 USD Billion and 0.17 USD Billion in 2024, respectively, with growth prospects reaching 5.0 USD Billion and 2.5 USD Billion by 2035, as local industries prioritize environmentally friendly production methods. Overall, the regional segmentation showcases varied growth drivers, with significant potential in established and emerging markets alike, highlighting the importance of sustainable steel production initiatives for environmental goals.

Source: Primary Research, Secondary Research, Market Research Future Database and Analyst Review

Key Players and Competitive Insights

The Green Steel Market is experiencing robust growth as environmental concerns and sustainability priorities drive manufacturers and consumers to seek more eco-friendly production methods. The competitive landscape is shaped by the pressing need for carbon neutrality and the shift toward hydrogen-reduced steelmaking processes. Various companies are investing heavily in research and development to innovate sustainable practices while maintaining high-quality steel production. As economies worldwide commit to reducing emissions, the market for green steel is likely to expand, drawing in new entrants while established players innovate to improve their offerings and enhance their competitive stance.

The competitive insights reveal a focus on technological advancements, strategic partnerships, and dynamic supply chain management to meet the changing demands of industries.Tata Steel has established a significant presence in the Green Steel Market, leveraging its expertise in steel manufacturing and commitment to sustainability. The company's strengths lie in its advanced manufacturing technologies and a strong emphasis on reducing its carbon footprint, positioning itself as a responsible steel producer. Tata Steel's ongoing initiatives in carbon capture and utilization demonstrate its proactive approach to addressing environmental challenges.

Additionally, the company has been focused on investing in renewable energy sources, which further strengthens its sustainability credentials. Through these efforts, Tata Steel is not only enhancing its reputation as a leader within the sector but also expanding its influence in markets that prioritize greener practices.Hyundai Steel is strategically positioned in the Green Steel Market, focusing on developing low-carbon and eco-friendly steel solutions. The company has adopted several initiatives to bolster its commitment to sustainability, including investing in innovative production technologies that reduce greenhouse gas emissions.

Hyundai Steel's key products include high-strength steel and specialized steel products that cater to various industries, emphasizing quality and sustainability. The company's market presence is augmented by its strategic mergers and acquisitions aimed at enhancing technological capabilities and expanding its product range. Hyundai Steel's ongoing R&D efforts to improve its steel production processes and its focus on industry collaborations further reflect its strengths in adapting to the evolving landscape of steel production. By maintaining a focus on sustainable practices, Hyundai Steel is poised to strengthen its market position as demand for green steel alternatives continues to grow globally.

Key Companies in the Green steel Market market include

Industry Developments

- Q3 2025: American startup tests cheaper approach to producing green steel Hertha Metals, a U.S. startup, announced the successful testing of a new, single-step, energy-efficient process for green steel production that minimizes emissions without increasing costs compared to traditional methods.

Future Outlook

Green steel Market Future Outlook

The Green Steel Market is projected to grow at a remarkable 1.13% CAGR from 2025 to 2035, driven by increasing demand for sustainable materials and regulatory support.

New opportunities lie in:

- Invest in innovative hydrogen-based steel production technologies.

- Develop partnerships with renewable energy providers for sustainable operations.

- Expand into emerging markets with tailored green steel solutions.

By 2035, the Green Steel Market is poised to achieve substantial growth, reflecting a robust transition towards sustainability.

Market Segmentation

Green Steel Market Form Outlook

- Flat Steel

- Long Steel

- Steel Products

Green Steel Market Regional Outlook

- North America

- Europe

- South America

- Asia Pacific

- Middle East and Africa

Green Steel Market Quality Grade Outlook

- High Strength Steel

- Low Alloy Steel

- Stainless Steel

Green Steel Market End Use Industry Outlook

- Construction

- Automotive

- Manufacturing

- Energy

Green Steel Market Method of Production Outlook

- Hydrogen-Based Reduction

- Electrolysis

- Biomass Direct Reduction

- Recycling

Report Scope

| Report Attribute/Metric | Details |

| Market Size 2024 | 2.91(USD Billion) |

| Market Size 2035 | 3480.06 (USD Billion) |

| Compound Annual Growth Rate (CAGR) | 112.52% (2025 - 2035) |

| Report Coverage | Revenue Forecast, Competitive Landscape, Growth Factors, and Trends |

| Base Year | 2024 |

| Market Forecast Period | 2025 - 2035 |

| Historical Data | 2019 - 2024 |

| Market Forecast Units | USD Billion |

| Key Companies Profiled | Tata Steel, Hyundai Steel, POSCO, Thyssenkrupp, ArcelorMittal, H2 Green Steel, Steel Dynamics, Nucor, ClevelandCliffs, SAIL, SSAB, Voestalpine, John Wood Group, United States Steel, Sierra Steel |

| Segments Covered | Method of Production, End Use Industry, Form, Quality Grade, Regional |

| Key Market Opportunities | Decarbonization initiatives drive demand, Government regulations favoring green processes, Growing electric vehicle manufacturing needs, Rising consumer preference for sustainability, and Investment in innovative production technologies. |

| Key Market Dynamics | sustainability trends, regulatory support, technological advancements, increasing demand, cost competitiveness |

| Countries Covered | North America, Europe, APAC, South America, MEA |

| Market Size 2025 | 1.85 (USD Billion) |

Market Highlights

Author

Latest Comments

John Doe

john@example.com

This is a great article! Really helped me understand the topic better.

Posted on July 23, 2025, 10:15

AM

Jane Smith

jane@domain.com

Thanks for sharing this. I’ve bookmarked it for later reference.

Posted on July 22, 2025, 7:45

PM

FAQs

What is the expected market size of the Green Steel Market in 2024?

The Green Steel Market is expected to be valued at 2.91 USD Billion in 2024.

What will be the market size of the Green Steel Market in 2035?

By 2035, the Green Steel Market is projected to reach 50.0 USD Billion.

What is the expected CAGR of the Green Steel Market from 2025 to 2035?

The expected CAGR for the Green Steel Market during this period is 29.5%.

Which region is expected to dominate the Green Steel Market by 2035?

Europe is expected to be the dominant region, with a market valuation of 20.0 USD Billion by 2035.

What is the market value of Hydrogen-Based Reduction in 2024?

The Hydrogen-Based Reduction segment is valued at 1.2 USD Billion in 2024.

What will the market size of Recycling be in 2035?

The Recycling segment is projected to reach 7.0 USD Billion by 2035.

Who are the key players in the Green Steel Market?

Major players include Tata Steel, Hyundai Steel, POSCO, Thyssenkrupp, and ArcelorMittal.

What is the market value of North America in the Green Steel Market for 2024?

North America is valued at 0.74 USD Billion in 2024.

What is the projected market value of the Asia Pacific region in 2035?

The Asia Pacific region is expected to reach a market value of 10.0 USD Billion by 2035.

What growth opportunities exist within the Green Steel Market?

Key opportunities include advancements in production methods and rising demand for sustainable steel.

-

Table of Contents

-

List of Tables and Figures

- 1. Executive Summary 1.1. Market Overview 1.2. Key Findings 1.3. Market Segmentation 1.4. Competitive Landscape 1.5. Challenges and Opportunities 1.6. Future Outlook 2. Market Introduction 2.1. Definition 2.2. Scope of the Study 2.2.1. Research Objective 2.2.2. Assumption 2.2.3. Limitations 3. Research Methodology 3.1. Overview 3.2. Data Mining 3.3. Secondary Research 3.4. Primary Research 3.4.1. Primary Interviews and Information Gathering Process 3.4.2. Breakdown of Primary Respondents 3.5. Forecasting Model 3.6. Market Size Estimation 3.6.1. Bottom-up Approach 3.6.2. Top-Down Approach 3.7. Data Triangulation 3.8. Validation 4. MARKET DYNAMICS 4.1. Overview 4.2. Drivers 4.3. Restraints 4.4. Opportunities 5. MARKET FACTOR ANALYSIS 5.1. Value chain Analysis 5.2. Porter's Five Forces Analysis 5.2.1. Bargaining Power of Suppliers 5.2.2. Bargaining Power of Buyers 5.2.3. Threat of New Entrants 5.2.4. Threat of Substitutes 5.2.5. Intensity of Rivalry 5.3. COVID-19 Impact Analysis 5.3.1. Market Impact Analysis 5.3.2. Regional Impact 5.3.3. Opportunity and Threat Analysis 6. GREEN STEEL MARKET BY METHOD OF PRODUCTION (USD BILLION) 6.1. Hydrogen-Based Reduction 6.2. Electrolysis 6.3. Biomass Direct Reduction 6.4. Recycling 7. GREEN STEEL MARKET BY END USE INDUSTRY (USD BILLION) 7.1. Construction 7.2. Automotive 7.3. Manufacturing 7.4. Energy 8. GREEN STEEL MARKET BY FORM (USD BILLION) 8.1. Flat Steel 8.2. Long Steel 8.3. Steel Products 9. GREEN STEEL MARKET BY QUALITY GRADE (USD BILLION) 9.1. High Strength Steel 9.2. Low Alloy Steel 9.3. Stainless Steel 10. GREEN STEEL MARKET BY REGIONAL (USD BILLION) 10.1. North America 10.1.1. US 10.1.2. Canada 10.2. Europe 10.2.1. Germany 10.2.2. UK 10.2.3. France 10.2.4. Russia 10.2.5. Italy 10.2.6. Spain 10.2.7. Rest of Europe 10.3. APAC 10.3.1. China 10.3.2. India 10.3.3. Japan 10.3.4. South Korea 10.3.5. Malaysia 10.3.6. Thailand 10.3.7. Indonesia 10.3.8. Rest of APAC 10.4. South America 10.4.1. Brazil 10.4.2. Mexico 10.4.3. Argentina 10.4.4. Rest of South America 10.5. MEA 10.5.1. GCC Countries 10.5.2. South Africa 10.5.3. Rest of MEA 11. Competitive Landscape 11.1. Overview 11.2. Competitive Analysis 11.3. Market share Analysis 11.4. Major Growth Strategy in the Green Steel Market 11.5. Competitive Benchmarking 11.6. Leading Players in Terms of Number of Developments in the Green Steel Market 11.7. Key developments and growth strategies 11.7.1. New Product Launch/Service Deployment 11.7.2. Merger & Acquisitions 11.7.3. Joint Ventures 11.8. Major Players Financial Matrix 11.8.1. Sales and Operating Income 11.8.2. Major Players R&D Expenditure. 2023 12. COMPANY PROFILES 12.1. Tata Steel 12.1.1. Financial Overview 12.1.2. Products Offered 12.1.3. Key Developments 12.1.4. SWOT Analysis 12.1.5. Key Strategies 12.2. Hyundai Steel 12.2.1. Financial Overview 12.2.2. Products Offered 12.2.3. Key Developments 12.2.4. SWOT Analysis 12.2.5. Key Strategies 12.3. POSCO 12.3.1. Financial Overview 12.3.2. Products Offered 12.3.3. Key Developments 12.3.4. SWOT Analysis 12.3.5. Key Strategies 12.4. Thyssenkrupp 12.4.1. Financial Overview 12.4.2. Products Offered 12.4.3. Key Developments 12.4.4. SWOT Analysis 12.4.5. Key Strategies 12.5. ArcelorMittal 12.5.1. Financial Overview 12.5.2. Products Offered 12.5.3. Key Developments 12.5.4. SWOT Analysis 12.5.5. Key Strategies 12.6. H2 Green Steel 12.6.1. Financial Overview 12.6.2. Products Offered 12.6.3. Key Developments 12.6.4. SWOT Analysis 12.6.5. Key Strategies 12.7. Steel Dynamics 12.7.1. Financial Overview 12.7.2. Products Offered 12.7.3. Key Developments 12.7.4. SWOT Analysis 12.7.5. Key Strategies 12.8. Nucor 12.8.1. Financial Overview 12.8.2. Products Offered 12.8.3. Key Developments 12.8.4. SWOT Analysis 12.8.5. Key Strategies 12.9. ClevelandCliffs 12.9.1. Financial Overview 12.9.2. Products Offered 12.9.3. Key Developments 12.9.4. SWOT Analysis 12.9.5. Key Strategies 12.10. SAIL 12.10.1. Financial Overview 12.10.2. Products Offered 12.10.3. Key Developments 12.10.4. SWOT Analysis 12.10.5. Key Strategies 12.11. SSAB 12.11.1. Financial Overview 12.11.2. Products Offered 12.11.3. Key Developments 12.11.4. SWOT Analysis 12.11.5. Key Strategies 12.12. Voestalpine 12.12.1. Financial Overview 12.12.2. Products Offered 12.12.3. Key Developments 12.12.4. SWOT Analysis 12.12.5. Key Strategies 12.13. John Wood Group 12.13.1. Financial Overview 12.13.2. Products Offered 12.13.3. Key Developments 12.13.4. SWOT Analysis 12.13.5. Key Strategies 12.14. United States Steel 12.14.1. Financial Overview 12.14.2. Products Offered 12.14.3. Key Developments 12.14.4. SWOT Analysis 12.14.5. Key Strategies 12.15. Sierra Steel 12.15.1. Financial Overview 12.15.2. Products Offered 12.15.3. Key Developments 12.15.4. SWOT Analysis 12.15.5. Key Strategies 13. APPENDIX 13.1. References 13.2. Related Reports LIST OF TABLES

- TABLE 1. LIST OF ASSUMPTIONS

- TABLE 2. NORTH AMERICA GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY METHOD OF PRODUCTION 2019-2035 (USD BILLIONS)

- TABLE 3. NORTH AMERICA GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY END USE INDUSTRY 2019-2035 (USD BILLIONS)

- TABLE 4. NORTH AMERICA GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY FORM 2019-2035 (USD BILLIONS)

- TABLE 5. NORTH AMERICA GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY QUALITY GRADE 2019-2035 (USD BILLIONS)

- TABLE 6. NORTH AMERICA GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY REGIONAL 2019-2035 (USD BILLIONS)

- TABLE 7. US GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY METHOD OF PRODUCTION 2019-2035 (USD BILLIONS)

- TABLE 8. US GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY END USE INDUSTRY 2019-2035 (USD BILLIONS)

- TABLE 9. US GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY FORM 2019-2035 (USD BILLIONS)

- TABLE 10. US GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY QUALITY GRADE 2019-2035 (USD BILLIONS)

- TABLE 11. US GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY REGIONAL 2019-2035 (USD BILLIONS)

- TABLE 12. CANADA GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY METHOD OF PRODUCTION 2019-2035 (USD BILLIONS)

- TABLE 13. CANADA GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY END USE INDUSTRY 2019-2035 (USD BILLIONS)

- TABLE 14. CANADA GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY FORM 2019-2035 (USD BILLIONS)

- TABLE 15. CANADA GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY QUALITY GRADE 2019-2035 (USD BILLIONS)

- TABLE 16. CANADA GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY REGIONAL 2019-2035 (USD BILLIONS)

- TABLE 17. EUROPE GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY METHOD OF PRODUCTION 2019-2035 (USD BILLIONS)

- TABLE 18. EUROPE GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY END USE INDUSTRY 2019-2035 (USD BILLIONS)

- TABLE 19. EUROPE GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY FORM 2019-2035 (USD BILLIONS)

- TABLE 20. EUROPE GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY QUALITY GRADE 2019-2035 (USD BILLIONS)

- TABLE 21. EUROPE GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY REGIONAL 2019-2035 (USD BILLIONS)

- TABLE 22. GERMANY GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY METHOD OF PRODUCTION 2019-2035 (USD BILLIONS)

- TABLE 23. GERMANY GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY END USE INDUSTRY 2019-2035 (USD BILLIONS)

- TABLE 24. GERMANY GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY FORM 2019-2035 (USD BILLIONS)

- TABLE 25. GERMANY GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY QUALITY GRADE 2019-2035 (USD BILLIONS)

- TABLE 26. GERMANY GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY REGIONAL 2019-2035 (USD BILLIONS)

- TABLE 27. UK GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY METHOD OF PRODUCTION 2019-2035 (USD BILLIONS)

- TABLE 28. UK GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY END USE INDUSTRY 2019-2035 (USD BILLIONS)

- TABLE 29. UK GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY FORM 2019-2035 (USD BILLIONS)

- TABLE 30. UK GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY QUALITY GRADE 2019-2035 (USD BILLIONS)

- TABLE 31. UK GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY REGIONAL 2019-2035 (USD BILLIONS)

- TABLE 32. FRANCE GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY METHOD OF PRODUCTION 2019-2035 (USD BILLIONS)

- TABLE 33. FRANCE GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY END USE INDUSTRY 2019-2035 (USD BILLIONS)

- TABLE 34. FRANCE GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY FORM 2019-2035 (USD BILLIONS)

- TABLE 35. FRANCE GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY QUALITY GRADE 2019-2035 (USD BILLIONS)

- TABLE 36. FRANCE GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY REGIONAL 2019-2035 (USD BILLIONS)

- TABLE 37. RUSSIA GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY METHOD OF PRODUCTION 2019-2035 (USD BILLIONS)

- TABLE 38. RUSSIA GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY END USE INDUSTRY 2019-2035 (USD BILLIONS)

- TABLE 39. RUSSIA GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY FORM 2019-2035 (USD BILLIONS)

- TABLE 40. RUSSIA GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY QUALITY GRADE 2019-2035 (USD BILLIONS)

- TABLE 41. RUSSIA GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY REGIONAL 2019-2035 (USD BILLIONS)

- TABLE 42. ITALY GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY METHOD OF PRODUCTION 2019-2035 (USD BILLIONS)

- TABLE 43. ITALY GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY END USE INDUSTRY 2019-2035 (USD BILLIONS)

- TABLE 44. ITALY GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY FORM 2019-2035 (USD BILLIONS)

- TABLE 45. ITALY GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY QUALITY GRADE 2019-2035 (USD BILLIONS)

- TABLE 46. ITALY GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY REGIONAL 2019-2035 (USD BILLIONS)

- TABLE 47. SPAIN GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY METHOD OF PRODUCTION 2019-2035 (USD BILLIONS)

- TABLE 48. SPAIN GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY END USE INDUSTRY 2019-2035 (USD BILLIONS)

- TABLE 49. SPAIN GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY FORM 2019-2035 (USD BILLIONS)

- TABLE 50. SPAIN GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY QUALITY GRADE 2019-2035 (USD BILLIONS)

- TABLE 51. SPAIN GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY REGIONAL 2019-2035 (USD BILLIONS)

- TABLE 52. REST OF EUROPE GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY METHOD OF PRODUCTION 2019-2035 (USD BILLIONS)

- TABLE 53. REST OF EUROPE GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY END USE INDUSTRY 2019-2035 (USD BILLIONS)

- TABLE 54. REST OF EUROPE GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY FORM 2019-2035 (USD BILLIONS)

- TABLE 55. REST OF EUROPE GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY QUALITY GRADE 2019-2035 (USD BILLIONS)

- TABLE 56. REST OF EUROPE GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY REGIONAL 2019-2035 (USD BILLIONS)

- TABLE 57. APAC GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY METHOD OF PRODUCTION 2019-2035 (USD BILLIONS)

- TABLE 58. APAC GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY END USE INDUSTRY 2019-2035 (USD BILLIONS)

- TABLE 59. APAC GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY FORM 2019-2035 (USD BILLIONS)

- TABLE 60. APAC GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY QUALITY GRADE 2019-2035 (USD BILLIONS)

- TABLE 61. APAC GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY REGIONAL 2019-2035 (USD BILLIONS)

- TABLE 62. CHINA GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY METHOD OF PRODUCTION 2019-2035 (USD BILLIONS)

- TABLE 63. CHINA GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY END USE INDUSTRY 2019-2035 (USD BILLIONS)

- TABLE 64. CHINA GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY FORM 2019-2035 (USD BILLIONS)

- TABLE 65. CHINA GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY QUALITY GRADE 2019-2035 (USD BILLIONS)

- TABLE 66. CHINA GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY REGIONAL 2019-2035 (USD BILLIONS)

- TABLE 67. INDIA GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY METHOD OF PRODUCTION 2019-2035 (USD BILLIONS)

- TABLE 68. INDIA GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY END USE INDUSTRY 2019-2035 (USD BILLIONS)

- TABLE 69. INDIA GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY FORM 2019-2035 (USD BILLIONS)

- TABLE 70. INDIA GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY QUALITY GRADE 2019-2035 (USD BILLIONS)

- TABLE 71. INDIA GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY REGIONAL 2019-2035 (USD BILLIONS)

- TABLE 72. JAPAN GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY METHOD OF PRODUCTION 2019-2035 (USD BILLIONS)

- TABLE 73. JAPAN GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY END USE INDUSTRY 2019-2035 (USD BILLIONS)

- TABLE 74. JAPAN GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY FORM 2019-2035 (USD BILLIONS)

- TABLE 75. JAPAN GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY QUALITY GRADE 2019-2035 (USD BILLIONS)

- TABLE 76. JAPAN GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY REGIONAL 2019-2035 (USD BILLIONS)

- TABLE 77. SOUTH KOREA GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY METHOD OF PRODUCTION 2019-2035 (USD BILLIONS)

- TABLE 78. SOUTH KOREA GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY END USE INDUSTRY 2019-2035 (USD BILLIONS)

- TABLE 79. SOUTH KOREA GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY FORM 2019-2035 (USD BILLIONS)

- TABLE 80. SOUTH KOREA GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY QUALITY GRADE 2019-2035 (USD BILLIONS)

- TABLE 81. SOUTH KOREA GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY REGIONAL 2019-2035 (USD BILLIONS)

- TABLE 82. MALAYSIA GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY METHOD OF PRODUCTION 2019-2035 (USD BILLIONS)

- TABLE 83. MALAYSIA GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY END USE INDUSTRY 2019-2035 (USD BILLIONS)

- TABLE 84. MALAYSIA GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY FORM 2019-2035 (USD BILLIONS)

- TABLE 85. MALAYSIA GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY QUALITY GRADE 2019-2035 (USD BILLIONS)

- TABLE 86. MALAYSIA GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY REGIONAL 2019-2035 (USD BILLIONS)

- TABLE 87. THAILAND GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY METHOD OF PRODUCTION 2019-2035 (USD BILLIONS)

- TABLE 88. THAILAND GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY END USE INDUSTRY 2019-2035 (USD BILLIONS)

- TABLE 89. THAILAND GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY FORM 2019-2035 (USD BILLIONS)

- TABLE 90. THAILAND GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY QUALITY GRADE 2019-2035 (USD BILLIONS)

- TABLE 91. THAILAND GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY REGIONAL 2019-2035 (USD BILLIONS)

- TABLE 92. INDONESIA GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY METHOD OF PRODUCTION 2019-2035 (USD BILLIONS)

- TABLE 93. INDONESIA GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY END USE INDUSTRY 2019-2035 (USD BILLIONS)

- TABLE 94. INDONESIA GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY FORM 2019-2035 (USD BILLIONS)

- TABLE 95. INDONESIA GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY QUALITY GRADE 2019-2035 (USD BILLIONS)

- TABLE 96. INDONESIA GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY REGIONAL 2019-2035 (USD BILLIONS)

- TABLE 97. REST OF APAC GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY METHOD OF PRODUCTION 2019-2035 (USD BILLIONS)

- TABLE 98. REST OF APAC GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY END USE INDUSTRY 2019-2035 (USD BILLIONS)

- TABLE 99. REST OF APAC GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY FORM 2019-2035 (USD BILLIONS)

- TABLE 100. REST OF APAC GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY QUALITY GRADE 2019-2035 (USD BILLIONS)

- TABLE 101. REST OF APAC GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY REGIONAL 2019-2035 (USD BILLIONS)

- TABLE 102. SOUTH AMERICA GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY METHOD OF PRODUCTION 2019-2035 (USD BILLIONS)

- TABLE 103. SOUTH AMERICA GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY END USE INDUSTRY 2019-2035 (USD BILLIONS)

- TABLE 104. SOUTH AMERICA GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY FORM 2019-2035 (USD BILLIONS)

- TABLE 105. SOUTH AMERICA GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY QUALITY GRADE 2019-2035 (USD BILLIONS)

- TABLE 106. SOUTH AMERICA GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY REGIONAL 2019-2035 (USD BILLIONS)

- TABLE 107. BRAZIL GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY METHOD OF PRODUCTION 2019-2035 (USD BILLIONS)

- TABLE 108. BRAZIL GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY END USE INDUSTRY 2019-2035 (USD BILLIONS)

- TABLE 109. BRAZIL GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY FORM 2019-2035 (USD BILLIONS)

- TABLE 110. BRAZIL GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY QUALITY GRADE 2019-2035 (USD BILLIONS)

- TABLE 111. BRAZIL GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY REGIONAL 2019-2035 (USD BILLIONS)

- TABLE 112. MEXICO GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY METHOD OF PRODUCTION 2019-2035 (USD BILLIONS)

- TABLE 113. MEXICO GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY END USE INDUSTRY 2019-2035 (USD BILLIONS)

- TABLE 114. MEXICO GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY FORM 2019-2035 (USD BILLIONS)

- TABLE 115. MEXICO GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY QUALITY GRADE 2019-2035 (USD BILLIONS)

- TABLE 116. MEXICO GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY REGIONAL 2019-2035 (USD BILLIONS)

- TABLE 117. ARGENTINA GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY METHOD OF PRODUCTION 2019-2035 (USD BILLIONS)

- TABLE 118. ARGENTINA GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY END USE INDUSTRY 2019-2035 (USD BILLIONS)

- TABLE 119. ARGENTINA GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY FORM 2019-2035 (USD BILLIONS)

- TABLE 120. ARGENTINA GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY QUALITY GRADE 2019-2035 (USD BILLIONS)

- TABLE 121. ARGENTINA GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY REGIONAL 2019-2035 (USD BILLIONS)

- TABLE 122. REST OF SOUTH AMERICA GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY METHOD OF PRODUCTION 2019-2035 (USD BILLIONS)

- TABLE 123. REST OF SOUTH AMERICA GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY END USE INDUSTRY 2019-2035 (USD BILLIONS)

- TABLE 124. REST OF SOUTH AMERICA GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY FORM 2019-2035 (USD BILLIONS)

- TABLE 125. REST OF SOUTH AMERICA GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY QUALITY GRADE 2019-2035 (USD BILLIONS)

- TABLE 126. REST OF SOUTH AMERICA GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY REGIONAL 2019-2035 (USD BILLIONS)

- TABLE 127. MEA GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY METHOD OF PRODUCTION 2019-2035 (USD BILLIONS)

- TABLE 128. MEA GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY END USE INDUSTRY 2019-2035 (USD BILLIONS)

- TABLE 129. MEA GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY FORM 2019-2035 (USD BILLIONS)

- TABLE 130. MEA GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY QUALITY GRADE 2019-2035 (USD BILLIONS)

- TABLE 131. MEA GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY REGIONAL 2019-2035 (USD BILLIONS)

- TABLE 132. GCC COUNTRIES GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY METHOD OF PRODUCTION 2019-2035 (USD BILLIONS)

- TABLE 133. GCC COUNTRIES GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY END USE INDUSTRY 2019-2035 (USD BILLIONS)

- TABLE 134. GCC COUNTRIES GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY FORM 2019-2035 (USD BILLIONS)

- TABLE 135. GCC COUNTRIES GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY QUALITY GRADE 2019-2035 (USD BILLIONS)

- TABLE 136. GCC COUNTRIES GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY REGIONAL 2019-2035 (USD BILLIONS)

- TABLE 137. SOUTH AFRICA GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY METHOD OF PRODUCTION 2019-2035 (USD BILLIONS)

- TABLE 138. SOUTH AFRICA GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY END USE INDUSTRY 2019-2035 (USD BILLIONS)

- TABLE 139. SOUTH AFRICA GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY FORM 2019-2035 (USD BILLIONS)

- TABLE 140. SOUTH AFRICA GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY QUALITY GRADE 2019-2035 (USD BILLIONS)

- TABLE 141. SOUTH AFRICA GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY REGIONAL 2019-2035 (USD BILLIONS)

- TABLE 142. REST OF MEA GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY METHOD OF PRODUCTION 2019-2035 (USD BILLIONS)

- TABLE 143. REST OF MEA GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY END USE INDUSTRY 2019-2035 (USD BILLIONS)

- TABLE 144. REST OF MEA GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY FORM 2019-2035 (USD BILLIONS)

- TABLE 145. REST OF MEA GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY QUALITY GRADE 2019-2035 (USD BILLIONS)

- TABLE 146. REST OF MEA GREEN STEEL MARKET SIZE ESTIMATES & FORECAST BY REGIONAL 2019-2035 (USD BILLIONS)

- TABLE 147. PRODUCT LAUNCH/PRODUCT DEVELOPMENT/APPROVAL

- TABLE 148. ACQUISITION/PARTNERSHIP LIST OF FIGURES

- FIGURE 1. MARKET SYNOPSIS

- FIGURE 2. NORTH AMERICA GREEN STEEL MARKET ANALYSIS

- FIGURE 3. US GREEN STEEL MARKET ANALYSIS BY METHOD OF PRODUCTION

- FIGURE 4. US GREEN STEEL MARKET ANALYSIS BY END USE INDUSTRY

- FIGURE 5. US GREEN STEEL MARKET ANALYSIS BY FORM

- FIGURE 6. US GREEN STEEL MARKET ANALYSIS BY QUALITY GRADE

- FIGURE 7. US GREEN STEEL MARKET ANALYSIS BY REGIONAL

- FIGURE 8. CANADA GREEN STEEL MARKET ANALYSIS BY METHOD OF PRODUCTION

- FIGURE 9. CANADA GREEN STEEL MARKET ANALYSIS BY END USE INDUSTRY

- FIGURE 10. CANADA GREEN STEEL MARKET ANALYSIS BY FORM

- FIGURE 11. CANADA GREEN STEEL MARKET ANALYSIS BY QUALITY GRADE

- FIGURE 12. CANADA GREEN STEEL MARKET ANALYSIS BY REGIONAL

- FIGURE 13. EUROPE GREEN STEEL MARKET ANALYSIS

- FIGURE 14. GERMANY GREEN STEEL MARKET ANALYSIS BY METHOD OF PRODUCTION

- FIGURE 15. GERMANY GREEN STEEL MARKET ANALYSIS BY END USE INDUSTRY

- FIGURE 16. GERMANY GREEN STEEL MARKET ANALYSIS BY FORM

- FIGURE 17. GERMANY GREEN STEEL MARKET ANALYSIS BY QUALITY GRADE

- FIGURE 18. GERMANY GREEN STEEL MARKET ANALYSIS BY REGIONAL

- FIGURE 19. UK GREEN STEEL MARKET ANALYSIS BY METHOD OF PRODUCTION

- FIGURE 20. UK GREEN STEEL MARKET ANALYSIS BY END USE INDUSTRY

- FIGURE 21. UK GREEN STEEL MARKET ANALYSIS BY FORM

- FIGURE 22. UK GREEN STEEL MARKET ANALYSIS BY QUALITY GRADE

- FIGURE 23. UK GREEN STEEL MARKET ANALYSIS BY REGIONAL

- FIGURE 24. FRANCE GREEN STEEL MARKET ANALYSIS BY METHOD OF PRODUCTION

- FIGURE 25. FRANCE GREEN STEEL MARKET ANALYSIS BY END USE INDUSTRY

- FIGURE 26. FRANCE GREEN STEEL MARKET ANALYSIS BY FORM

- FIGURE 27. FRANCE GREEN STEEL MARKET ANALYSIS BY QUALITY GRADE

- FIGURE 28. FRANCE GREEN STEEL MARKET ANALYSIS BY REGIONAL

- FIGURE 29. RUSSIA GREEN STEEL MARKET ANALYSIS BY METHOD OF PRODUCTION

- FIGURE 30. RUSSIA GREEN STEEL MARKET ANALYSIS BY END USE INDUSTRY

- FIGURE 31. RUSSIA GREEN STEEL MARKET ANALYSIS BY FORM

- FIGURE 32. RUSSIA GREEN STEEL MARKET ANALYSIS BY QUALITY GRADE

- FIGURE 33. RUSSIA GREEN STEEL MARKET ANALYSIS BY REGIONAL

- FIGURE 34. ITALY GREEN STEEL MARKET ANALYSIS BY METHOD OF PRODUCTION

- FIGURE 35. ITALY GREEN STEEL MARKET ANALYSIS BY END USE INDUSTRY

- FIGURE 36. ITALY GREEN STEEL MARKET ANALYSIS BY FORM

- FIGURE 37. ITALY GREEN STEEL MARKET ANALYSIS BY QUALITY GRADE

- FIGURE 38. ITALY GREEN STEEL MARKET ANALYSIS BY REGIONAL

- FIGURE 39. SPAIN GREEN STEEL MARKET ANALYSIS BY METHOD OF PRODUCTION

- FIGURE 40. SPAIN GREEN STEEL MARKET ANALYSIS BY END USE INDUSTRY

- FIGURE 41. SPAIN GREEN STEEL MARKET ANALYSIS BY FORM

- FIGURE 42. SPAIN GREEN STEEL MARKET ANALYSIS BY QUALITY GRADE

- FIGURE 43. SPAIN GREEN STEEL MARKET ANALYSIS BY REGIONAL

- FIGURE 44. REST OF EUROPE GREEN STEEL MARKET ANALYSIS BY METHOD OF PRODUCTION

- FIGURE 45. REST OF EUROPE GREEN STEEL MARKET ANALYSIS BY END USE INDUSTRY

- FIGURE 46. REST OF EUROPE GREEN STEEL MARKET ANALYSIS BY FORM

- FIGURE 47. REST OF EUROPE GREEN STEEL MARKET ANALYSIS BY QUALITY GRADE

- FIGURE 48. REST OF EUROPE GREEN STEEL MARKET ANALYSIS BY REGIONAL

- FIGURE 49. APAC GREEN STEEL MARKET ANALYSIS

- FIGURE 50. CHINA GREEN STEEL MARKET ANALYSIS BY METHOD OF PRODUCTION

- FIGURE 51. CHINA GREEN STEEL MARKET ANALYSIS BY END USE INDUSTRY

- FIGURE 52. CHINA GREEN STEEL MARKET ANALYSIS BY FORM

- FIGURE 53. CHINA GREEN STEEL MARKET ANALYSIS BY QUALITY GRADE

- FIGURE 54. CHINA GREEN STEEL MARKET ANALYSIS BY REGIONAL

- FIGURE 55. INDIA GREEN STEEL MARKET ANALYSIS BY METHOD OF PRODUCTION

- FIGURE 56. INDIA GREEN STEEL MARKET ANALYSIS BY END USE INDUSTRY

- FIGURE 57. INDIA GREEN STEEL MARKET ANALYSIS BY FORM

- FIGURE 58. INDIA GREEN STEEL MARKET ANALYSIS BY QUALITY GRADE

- FIGURE 59. INDIA GREEN STEEL MARKET ANALYSIS BY REGIONAL

- FIGURE 60. JAPAN GREEN STEEL MARKET ANALYSIS BY METHOD OF PRODUCTION

- FIGURE 61. JAPAN GREEN STEEL MARKET ANALYSIS BY END USE INDUSTRY

- FIGURE 62. JAPAN GREEN STEEL MARKET ANALYSIS BY FORM

- FIGURE 63. JAPAN GREEN STEEL MARKET ANALYSIS BY QUALITY GRADE

- FIGURE 64. JAPAN GREEN STEEL MARKET ANALYSIS BY REGIONAL

- FIGURE 65. SOUTH KOREA GREEN STEEL MARKET ANALYSIS BY METHOD OF PRODUCTION

- FIGURE 66. SOUTH KOREA GREEN STEEL MARKET ANALYSIS BY END USE INDUSTRY

- FIGURE 67. SOUTH KOREA GREEN STEEL MARKET ANALYSIS BY FORM

- FIGURE 68. SOUTH KOREA GREEN STEEL MARKET ANALYSIS BY QUALITY GRADE

- FIGURE 69. SOUTH KOREA GREEN STEEL MARKET ANALYSIS BY REGIONAL

- FIGURE 70. MALAYSIA GREEN STEEL MARKET ANALYSIS BY METHOD OF PRODUCTION

- FIGURE 71. MALAYSIA GREEN STEEL MARKET ANALYSIS BY END USE INDUSTRY

- FIGURE 72. MALAYSIA GREEN STEEL MARKET ANALYSIS BY FORM

- FIGURE 73. MALAYSIA GREEN STEEL MARKET ANALYSIS BY QUALITY GRADE

- FIGURE 74. MALAYSIA GREEN STEEL MARKET ANALYSIS BY REGIONAL

- FIGURE 75. THAILAND GREEN STEEL MARKET ANALYSIS BY METHOD OF PRODUCTION

- FIGURE 76. THAILAND GREEN STEEL MARKET ANALYSIS BY END USE INDUSTRY

- FIGURE 77. THAILAND GREEN STEEL MARKET ANALYSIS BY FORM

- FIGURE 78. THAILAND GREEN STEEL MARKET ANALYSIS BY QUALITY GRADE

- FIGURE 79. THAILAND GREEN STEEL MARKET ANALYSIS BY REGIONAL

- FIGURE 80. INDONESIA GREEN STEEL MARKET ANALYSIS BY METHOD OF PRODUCTION

- FIGURE 81. INDONESIA GREEN STEEL MARKET ANALYSIS BY END USE INDUSTRY

- FIGURE 82. INDONESIA GREEN STEEL MARKET ANALYSIS BY FORM

- FIGURE 83. INDONESIA GREEN STEEL MARKET ANALYSIS BY QUALITY GRADE

- FIGURE 84. INDONESIA GREEN STEEL MARKET ANALYSIS BY REGIONAL

- FIGURE 85. REST OF APAC GREEN STEEL MARKET ANALYSIS BY METHOD OF PRODUCTION

- FIGURE 86. REST OF APAC GREEN STEEL MARKET ANALYSIS BY END USE INDUSTRY

- FIGURE 87. REST OF APAC GREEN STEEL MARKET ANALYSIS BY FORM

- FIGURE 88. REST OF APAC GREEN STEEL MARKET ANALYSIS BY QUALITY GRADE

- FIGURE 89. REST OF APAC GREEN STEEL MARKET ANALYSIS BY REGIONAL

- FIGURE 90. SOUTH AMERICA GREEN STEEL MARKET ANALYSIS

- FIGURE 91. BRAZIL GREEN STEEL MARKET ANALYSIS BY METHOD OF PRODUCTION

- FIGURE 92. BRAZIL GREEN STEEL MARKET ANALYSIS BY END USE INDUSTRY

- FIGURE 93. BRAZIL GREEN STEEL MARKET ANALYSIS BY FORM

- FIGURE 94. BRAZIL GREEN STEEL MARKET ANALYSIS BY QUALITY GRADE

- FIGURE 95. BRAZIL GREEN STEEL MARKET ANALYSIS BY REGIONAL

- FIGURE 96. MEXICO GREEN STEEL MARKET ANALYSIS BY METHOD OF PRODUCTION

- FIGURE 97. MEXICO GREEN STEEL MARKET ANALYSIS BY END USE INDUSTRY

- FIGURE 98. MEXICO GREEN STEEL MARKET ANALYSIS BY FORM

- FIGURE 99. MEXICO GREEN STEEL MARKET ANALYSIS BY QUALITY GRADE

- FIGURE 100. MEXICO GREEN STEEL MARKET ANALYSIS BY REGIONAL

- FIGURE 101. ARGENTINA GREEN STEEL MARKET ANALYSIS BY METHOD OF PRODUCTION

- FIGURE 102. ARGENTINA GREEN STEEL MARKET ANALYSIS BY END USE INDUSTRY

- FIGURE 103. ARGENTINA GREEN STEEL MARKET ANALYSIS BY FORM

- FIGURE 104. ARGENTINA GREEN STEEL MARKET ANALYSIS BY QUALITY GRADE

- FIGURE 105. ARGENTINA GREEN STEEL MARKET ANALYSIS BY REGIONAL

- FIGURE 106. REST OF SOUTH AMERICA GREEN STEEL MARKET ANALYSIS BY METHOD OF PRODUCTION

- FIGURE 107. REST OF SOUTH AMERICA GREEN STEEL MARKET ANALYSIS BY END USE INDUSTRY

- FIGURE 108. REST OF SOUTH AMERICA GREEN STEEL MARKET ANALYSIS BY FORM

- FIGURE 109. REST OF SOUTH AMERICA GREEN STEEL MARKET ANALYSIS BY QUALITY GRADE

- FIGURE 110. REST OF SOUTH AMERICA GREEN STEEL MARKET ANALYSIS BY REGIONAL

- FIGURE 111. MEA GREEN STEEL MARKET ANALYSIS

- FIGURE 112. GCC COUNTRIES GREEN STEEL MARKET ANALYSIS BY METHOD OF PRODUCTION

- FIGURE 113. GCC COUNTRIES GREEN STEEL MARKET ANALYSIS BY END USE INDUSTRY

- FIGURE 114. GCC COUNTRIES GREEN STEEL MARKET ANALYSIS BY FORM

- FIGURE 115. GCC COUNTRIES GREEN STEEL MARKET ANALYSIS BY QUALITY GRADE

- FIGURE 116. GCC COUNTRIES GREEN STEEL MARKET ANALYSIS BY REGIONAL

- FIGURE 117. SOUTH AFRICA GREEN STEEL MARKET ANALYSIS BY METHOD OF PRODUCTION

- FIGURE 118. SOUTH AFRICA GREEN STEEL MARKET ANALYSIS BY END USE INDUSTRY

- FIGURE 119. SOUTH AFRICA GREEN STEEL MARKET ANALYSIS BY FORM

- FIGURE 120. SOUTH AFRICA GREEN STEEL MARKET ANALYSIS BY QUALITY GRADE

- FIGURE 121. SOUTH AFRICA GREEN STEEL MARKET ANALYSIS BY REGIONAL

- FIGURE 122. REST OF MEA GREEN STEEL MARKET ANALYSIS BY METHOD OF PRODUCTION

- FIGURE 123. REST OF MEA GREEN STEEL MARKET ANALYSIS BY END USE INDUSTRY

- FIGURE 124. REST OF MEA GREEN STEEL MARKET ANALYSIS BY FORM

- FIGURE 125. REST OF MEA GREEN STEEL MARKET ANALYSIS BY QUALITY GRADE

- FIGURE 126. REST OF MEA GREEN STEEL MARKET ANALYSIS BY REGIONAL

- FIGURE 127. KEY BUYING CRITERIA OF GREEN STEEL MARKET

- FIGURE 128. RESEARCH PROCESS OF MRFR

- FIGURE 129. DRO ANALYSIS OF GREEN STEEL MARKET

- FIGURE 130. DRIVERS IMPACT ANALYSIS GREEN STEEL MARKET

- FIGURE 131. RESTRAINTS IMPACT ANALYSIS GREEN STEEL MARKET

- FIGURE 132. SUPPLY / VALUE CHAIN GREEN STEEL MARKET

- FIGURE 133. GREEN STEEL MARKET BY METHOD OF PRODUCTION 2025 (% SHARE)

- FIGURE 134. GREEN STEEL BY METHOD OF PRODUCTION 2019 TO 2035 (USD Billions)

- FIGURE 135. GREEN STEEL BY END USE INDUSTRY 2025 (% SHARE)

- FIGURE 136. GREEN STEEL BY END USE INDUSTRY 2019 TO 2035 (USD Billions)

- FIGURE 137. GREEN STEEL BY FORM 2025 (% SHARE)

- FIGURE 138. GREEN STEEL BY FORM 2019 TO 2035 (USD Billions)

- FIGURE 139. GREEN STEEL BY QUALITY GRADE 2025 (% SHARE)

- FIGURE 140. GREEN STEEL BY QUALITY GRADE 2019 TO 2035 (USD Billions)

- FIGURE 141. GREEN STEEL BY REGIONAL 2025 (% SHARE)

- FIGURE 142. GREEN STEEL BY REGIONAL 2019 TO 2035 (USD Billions)

- FIGURE 143. BENCHMARKING OF MAJOR COMPETITORS

Green Steel Market Segmentation

Green Steel By Method of Production (USD Billion, 2019-2035)

- Hydrogen-Based Reduction

- Electrolysis

- Biomass Direct Reduction

- Recycling

Green Steel By End Use Industry (USD Billion, 2019-2035)

- Construction

- Automotive

- Manufacturing

- Energy

Green Steel By Form (USD Billion, 2019-2035)

- Flat Steel

- Long Steel

- Steel Products

Green Steel By Quality Grade (USD Billion, 2019-2035)

- High Strength Steel

- Low Alloy Steel

- Stainless Steel

Green Steel By Regional (USD Billion, 2019-2035)

- North America

- Europe

- South America

- Asia Pacific

- Middle East and Africa

Green Steel Market Regional Outlook (USD Billion, 2019-2035)

North America Outlook (USD Billion, 2019-2035)

North America Green Steel by Method of Production Type

- Hydrogen-Based Reduction

- Electrolysis

- Biomass Direct Reduction

- Recycling

North America Green Steel by End Use Industry Type

- Construction

- Automotive

- Manufacturing

- Energy

North America Green Steel by Form Type

- Flat Steel

- Long Steel

- Steel Products

North America Green Steel by Quality Grade Type

- High Strength Steel

- Low Alloy Steel

- Stainless Steel

North America Green Steel by Regional Type

- US

- Canada

- US Outlook (USD Billion, 2019-2035)

US Green Steel by Method of Production Type

- Hydrogen-Based Reduction

- Electrolysis

- Biomass Direct Reduction

- Recycling

US Green Steel by End Use Industry Type

- Construction

- Automotive

- Manufacturing

- Energy

US Green Steel by Form Type

- Flat Steel

- Long Steel

- Steel Products

US Green Steel by Quality Grade Type

- High Strength Steel

- Low Alloy Steel

- Stainless Steel

- CANADA Outlook (USD Billion, 2019-2035)

CANADA Green Steel by Method of Production Type

- Hydrogen-Based Reduction

- Electrolysis

- Biomass Direct Reduction

- Recycling

CANADA Green Steel by End Use Industry Type

- Construction

- Automotive

- Manufacturing

- Energy

CANADA Green Steel by Form Type

- Flat Steel

- Long Steel

- Steel Products

CANADA Green Steel by Quality Grade Type

- High Strength Steel

- Low Alloy Steel

- Stainless Steel

Europe Outlook (USD Billion, 2019-2035)

Europe Green Steel by Method of Production Type

- Hydrogen-Based Reduction

- Electrolysis

- Biomass Direct Reduction

- Recycling

Europe Green Steel by End Use Industry Type

- Construction

- Automotive

- Manufacturing

- Energy

Europe Green Steel by Form Type

- Flat Steel

- Long Steel

- Steel Products

Europe Green Steel by Quality Grade Type

- High Strength Steel

- Low Alloy Steel

- Stainless Steel

Europe Green Steel by Regional Type

- Germany

- UK

- France

- Russia

- Italy

- Spain

- Rest of Europe

- GERMANY Outlook (USD Billion, 2019-2035)

GERMANY Green Steel by Method of Production Type

- Hydrogen-Based Reduction

- Electrolysis

- Biomass Direct Reduction

- Recycling

GERMANY Green Steel by End Use Industry Type

- Construction

- Automotive

- Manufacturing

- Energy

GERMANY Green Steel by Form Type

- Flat Steel

- Long Steel

- Steel Products

GERMANY Green Steel by Quality Grade Type

- High Strength Steel

- Low Alloy Steel

- Stainless Steel

- UK Outlook (USD Billion, 2019-2035)

UK Green Steel by Method of Production Type

- Hydrogen-Based Reduction

- Electrolysis

- Biomass Direct Reduction

- Recycling

UK Green Steel by End Use Industry Type

- Construction

- Automotive

- Manufacturing

- Energy

UK Green Steel by Form Type

- Flat Steel

- Long Steel

- Steel Products

UK Green Steel by Quality Grade Type

- High Strength Steel

- Low Alloy Steel

- Stainless Steel

- FRANCE Outlook (USD Billion, 2019-2035)

FRANCE Green Steel Market by Method of Production Type

- Hydrogen-Based Reduction

- Electrolysis

- Biomass Direct Reduction

- Recycling

FRANCE Green Steel by End Use Industry Type

- Construction

- Automotive

- Manufacturing

- Energy

FRANCE Green Steel by Form Type

- Flat Steel

- Long Steel

- Steel Products

FRANCE Green Steel by Quality Grade Type

- High Strength Steel

- Low Alloy Steel

- Stainless Steel

- RUSSIA Outlook (USD Billion, 2019-2035)

RUSSIA Green Steel by Method of Production Type

- Hydrogen-Based Reduction

- Electrolysis

- Biomass Direct Reduction

- Recycling

RUSSIA Green Steel by End Use Industry Type

- Construction

- Automotive

- Manufacturing

- Energy

RUSSIA Green Steel by Form Type

- Flat Steel

- Long Steel

- Steel Products

RUSSIA Green Steel by Quality Grade Type

- High Strength Steel

- Low Alloy Steel

- Stainless Steel

- ITALY Outlook (USD Billion, 2019-2035)

ITALY Green Steel by Method of Production Type

- Hydrogen-Based Reduction

- Electrolysis

- Biomass Direct Reduction

- Recycling

ITALY Green Steel by End Use Industry Type

- Construction

- Automotive

- Manufacturing

- Energy

ITALY Green Steel by Form Type

- Flat Steel

- Long Steel

- Steel Products

ITALY Green Steel by Quality Grade Type

- High Strength Steel

- Low Alloy Steel

- Stainless Steel

- SPAIN Outlook (USD Billion, 2019-2035)

SPAIN Green Steel by Method of Production Type

- Hydrogen-Based Reduction

- Electrolysis

- Biomass Direct Reduction

- Recycling

SPAIN Green Steel by End Use Industry Type

- Construction

- Automotive

- Manufacturing

- Energy

SPAIN Green Steel by Form Type

- Flat Steel

- Long Steel

- Steel Products

SPAIN Green Steel by Quality Grade Type

- High Strength Steel

- Low Alloy Steel

- Stainless Steel

- REST OF EUROPE Outlook (USD Billion, 2019-2035)

REST OF EUROPE Green Steel by Method of Production Type

- Hydrogen-Based Reduction

- Electrolysis

- Biomass Direct Reduction

- Recycling

REST OF EUROPE Green Steel by End Use Industry Type

- Construction

- Automotive

- Manufacturing

- Energy

REST OF EUROPE Green Steel by Form Type

- Flat Steel

- Long Steel

- Steel Products

REST OF EUROPE Green Steel by Quality Grade Type

- High Strength Steel

- Low Alloy Steel

- Stainless Steel

APAC Outlook (USD Billion, 2019-2035)

APAC Green Steel by Method of Production Type

- Hydrogen-Based Reduction

- Electrolysis

- Biomass Direct Reduction

- Recycling

APAC Green Steel by End Use Industry Type

- Construction

- Automotive

- Manufacturing

- Energy

APAC Green Steel by Form Type

- Flat Steel

- Long Steel

- Steel Products

APAC Green Steel by Quality Grade Type

- High Strength Steel

- Low Alloy Steel

- Stainless Steel

APAC Green Steel by Regional Type

- China

- India

- Japan

- South Korea

- Malaysia

- Thailand

- Indonesia

- Rest of APAC

- CHINA Outlook (USD Billion, 2019-2035)

CHINA Green Steel by Method of Production Type

- Hydrogen-Based Reduction

- Electrolysis

- Biomass Direct Reduction

- Recycling

CHINA Green Steel by End Use Industry Type

- Construction

- Automotive

- Manufacturing

- Energy

CHINA Green Steel by Form Type

- Flat Steel

- Long Steel

- Steel Products

CHINA Green Steel by Quality Grade Type

- High Strength Steel

- Low Alloy Steel

- Stainless Steel

- INDIA Outlook (USD Billion, 2019-2035)

INDIA Green Steel by Method of Production Type

- Hydrogen-Based Reduction

- Electrolysis

- Biomass Direct Reduction

- Recycling

INDIA Green Steel by End Use Industry Type

- Construction

- Automotive

- Manufacturing

- Energy

INDIA Green Steel by Form Type

- Flat Steel

- Long Steel

- Steel Products

INDIA Green Steel by Quality Grade Type

- High Strength Steel

- Low Alloy Steel

- Stainless Steel

- JAPAN Outlook (USD Billion, 2019-2035)

JAPAN Green Steel by Method of Production Type

- Hydrogen-Based Reduction

- Electrolysis

- Biomass Direct Reduction

- Recycling

JAPAN Green Steel by End Use Industry Type

- Construction

- Automotive

- Manufacturing

- Energy

JAPAN Green Steel by Form Type

- Flat Steel

- Long Steel

- Steel Products

JAPAN Green Steel by Quality Grade Type

- High Strength Steel

- Low Alloy Steel

- Stainless Steel

- SOUTH KOREA Outlook (USD Billion, 2019-2035)

SOUTH KOREA Green Steel by Method of Production Type

- Hydrogen-Based Reduction

- Electrolysis

- Biomass Direct Reduction

- Recycling

SOUTH KOREA Green Steel by End Use Industry Type

- Construction

- Automotive

- Manufacturing

- Energy

SOUTH KOREA Green Steel by Form Type

- Flat Steel

- Long Steel

- Steel Products

SOUTH KOREA Green Steel by Quality Grade Type

- High Strength Steel

- Low Alloy Steel

- Stainless Steel

- MALAYSIA Outlook (USD Billion, 2019-2035)

MALAYSIA Green Steel by Method of Production Type

- Hydrogen-Based Reduction

- Electrolysis

- Biomass Direct Reduction

- Recycling

MALAYSIA Green Steel by End Use Industry Type

- Construction

- Automotive

- Manufacturing

- Energy

MALAYSIA Green Steel by Form Type

- Flat Steel

- Long Steel

- Steel Products

MALAYSIA Green Steel by Quality Grade Type

- High Strength Steel

- Low Alloy Steel

- Stainless Steel

- THAILAND Outlook (USD Billion, 2019-2035)

THAILAND Green Steel by Method of Production Type

- Hydrogen-Based Reduction

- Electrolysis

- Biomass Direct Reduction

- Recycling

THAILAND Green Steel by End Use Industry Type

- Construction

- Automotive

- Manufacturing

- Energy

THAILAND Green Steel by Form Type

- Flat Steel

- Long Steel

- Steel Products

THAILAND Green Steel by Quality Grade Type

- High Strength Steel

- Low Alloy Steel

- Stainless Steel

- INDONESIA Outlook (USD Billion, 2019-2035)

INDONESIA Green Steel by Method of Production Type

- Hydrogen-Based Reduction

- Electrolysis

- Biomass Direct Reduction

- Recycling

INDONESIA Green Steel by End Use Industry Type

- Construction

- Automotive

- Manufacturing

- Energy

INDONESIA Green Steel by Form Type

- Flat Steel

- Long Steel

- Steel Products

INDONESIA Green Steel by Quality Grade Type

- High Strength Steel

- Low Alloy Steel

- Stainless Steel

- REST OF APAC Outlook (USD Billion, 2019-2035)

REST OF APAC Green Steel by Method of Production Type

- Hydrogen-Based Reduction

- Electrolysis

- Biomass Direct Reduction

- Recycling

REST OF APAC Green Steel by End Use Industry Type

- Construction

- Automotive

- Manufacturing

- Energy

REST OF APAC Green Steel by Form Type

- Flat Steel

- Long Steel

- Steel Products

REST OF APAC Green Steel by Quality Grade Type

- High Strength Steel

- Low Alloy Steel

- Stainless Steel

South America Outlook (USD Billion, 2019-2035)

South America Green Steel by Method of Production Type

- Hydrogen-Based Reduction

- Electrolysis

- Biomass Direct Reduction

- Recycling

South America Green Steel by End Use Industry Type

- Construction

- Automotive

- Manufacturing

- Energy

South America Green Steel by Form Type

- Flat Steel

- Long Steel

- Steel Products

South America Green Steel by Quality Grade Type

- High Strength Steel

- Low Alloy Steel

- Stainless Steel

South America Green Steel by Regional Type

- Brazil

- Mexico

- Argentina

- Rest of South America

- BRAZIL Outlook (USD Billion, 2019-2035)

BRAZIL Green Steel by Method of Production Type

- Hydrogen-Based Reduction

- Electrolysis

- Biomass Direct Reduction

- Recycling

BRAZIL Green Steel by End Use Industry Type

- Construction

- Automotive

- Manufacturing

- Energy

BRAZIL Green Steel by Form Type

- Flat Steel

- Long Steel

- Steel Products

BRAZIL Green Steel by Quality Grade Type

- High Strength Steel

- Low Alloy Steel

- Stainless Steel

- MEXICO Outlook (USD Billion, 2019-2035)

MEXICO Green Steel by Method of Production Type

- Hydrogen-Based Reduction

- Electrolysis

- Biomass Direct Reduction

- Recycling

MEXICO Green Steel by End Use Industry Type

- Construction

- Automotive

- Manufacturing

- Energy

MEXICO Green Steel by Form Type

- Flat Steel

- Long Steel

- Steel Products

MEXICO Green Steel by Quality Grade Type

- High Strength Steel

- Low Alloy Steel

- Stainless Steel

- ARGENTINA Outlook (USD Billion, 2019-2035)

ARGENTINA Green Steel by Method of Production Type

- Hydrogen-Based Reduction

- Electrolysis

- Biomass Direct Reduction

- Recycling

ARGENTINA Green Steel by End Use Industry Type

- Construction

- Automotive

- Manufacturing

- Energy

ARGENTINA Green Steel by Form Type

- Flat Steel

- Long Steel

- Steel Products

ARGENTINA Green Steel by Quality Grade Type

- High Strength Steel

- Low Alloy Steel

- Stainless Steel

- REST OF SOUTH AMERICA Outlook (USD Billion, 2019-2035)

REST OF SOUTH AMERICA Green Steel by Method of Production Type

- Hydrogen-Based Reduction

- Electrolysis

- Biomass Direct Reduction

- Recycling

REST OF SOUTH AMERICA Green Steel by End Use Industry Type

- Construction

- Automotive

- Manufacturing

- Energy

REST OF SOUTH AMERICA Green Steel by Form Type

- Flat Steel

- Long Steel

- Steel Products

REST OF SOUTH AMERICA Green Steel by Quality Grade Type

- High Strength Steel

- Low Alloy Steel

- Stainless Steel

MEA Outlook (USD Billion, 2019-2035)

MEA Green Steel by Method of Production Type

- Hydrogen-Based Reduction

- Electrolysis

- Biomass Direct Reduction

- Recycling

MEA Green Steel by End Use Industry Type

- Construction

- Automotive

- Manufacturing

- Energy

MEA Green Steel by Form Type

- Flat Steel

- Long Steel

- Steel Products

MEA Green Steel by Quality Grade Type

- High Strength Steel

- Low Alloy Steel

- Stainless Steel

MEA Green Steel by Regional Type

- GCC Countries

- South Africa

- Rest of MEA

- GCC COUNTRIES Outlook (USD Billion, 2019-2035)

GCC COUNTRIES Green Steel by Method of Production Type

- Hydrogen-Based Reduction

- Electrolysis

- Biomass Direct Reduction

- Recycling

GCC COUNTRIES Green Steel by End Use Industry Type

- Construction

- Automotive

- Manufacturing

- Energy

GCC COUNTRIES Green Steel by Form Type

- Flat Steel

- Long Steel

- Steel Products

GCC COUNTRIES Green Steel by Quality Grade Type

- High Strength Steel

- Low Alloy Steel

- Stainless Steel

- SOUTH AFRICA Outlook (USD Billion, 2019-2035)

SOUTH AFRICA Green Steel by Method of Production Type

- Hydrogen-Based Reduction

- Electrolysis

- Biomass Direct Reduction

- Recycling

SOUTH AFRICA Green Steel by End Use Industry Type

- Construction

- Automotive

- Manufacturing

- Energy

SOUTH AFRICA Green Steel by Form Type

- Flat Steel

- Long Steel

- Steel Products

SOUTH AFRICA Green Steel by Quality Grade Type

- High Strength Steel

- Low Alloy Steel

- Stainless Steel

- REST OF MEA Outlook (USD Billion, 2019-2035)

REST OF MEA Green Steel by Method of Production Type

- Hydrogen-Based Reduction

- Electrolysis

- Biomass Direct Reduction

- Recycling

REST OF MEA Green Steel by End Use Industry Type

- Construction

- Automotive

- Manufacturing

- Energy

REST OF MEA Green Steel by Form Type

- Flat Steel

- Long Steel

- Steel Products

REST OF MEA Green Steel by Quality Grade Type

- High Strength Steel

- Low Alloy Steel

- Stainless Steel

Free Sample Request

Kindly complete the form below to receive a free sample of this Report

Customer Strories

“I am very pleased with how market segments have been defined in a relevant way for my purposes (such as "Portable Freezers & refrigerators" and "last-mile"). In general the report is well structured. Thanks very much for your efforts.”

Leave a Comment