Certified Global Research Member

Key Questions Answered

- Global Market Outlook

- In-depth analysis of global and regional trends

- Analyze and identify the major players in the market, their market share, key developments, etc.

- To understand the capability of the major players based on products offered, financials, and strategies.

- Identify disrupting products, companies, and trends.

- To identify opportunities in the market.

- Analyze the key challenges in the market.

- Analyze the regional penetration of players, products, and services in the market.

- Comparison of major players’ financial performance.

- Evaluate strategies adopted by major players.

- Recommendations

Why Choose Market Research Future?

- Vigorous research methodologies for specific market.

- Knowledge partners across the globe

- Large network of partner consultants.

- Ever-increasing/ Escalating data base with quarterly monitoring of various markets

- Trusted by fortune 500 companies/startups/ universities/organizations

- Large database of 5000+ markets reports.

- Effective and prompt pre- and post-sales support.

The landscape of the Mobile Emission Catalysts Market keeps changing because of various forces like strict regulations on emissions set up by different governments across the globe, among other factors, including increased use of electric vehicles (EV) as well as constant development of internal combustion engines (ICE). Some types of mobile emission catalysts, like catalytic converters, help decrease harmful pollutants produced by vehicles, such as nitrogen oxides (NOx), carbon monoxide (CO), and hydrocarbons, among others. Technological advancements in emission control systems and catalyst formulations are playing a pivotal role in shaping the market dynamics of mobile emission catalysts. There are also innovations in catalytic converter designs, materials, and technologies that improve emission reduction performance. As the automotive industry transitions towards hybrid and electric vehicles, research and development efforts are focused on optimizing emission catalysts for internal combustion engines, contributing to the overall dynamism of the market.

The competitive landscape is a significant factor influencing market dynamics, with various global and regional players competing to provide advanced mobile emission catalyst solutions. Technological innovation, quality products, and collaboration with automakers are some of the ways in which differentiation takes place in this market, leading to its competitiveness. Regulatory influences play a crucial role in shaping the market dynamics of the mobile emission catalysts market. Governments worldwide are implementing strict emission standards to address air quality concerns and combat climate change. Compliance with these regulations is essential for automotive manufacturers, driving the adoption of advanced emission control technologies and influencing the market dynamics of mobile emission catalysts. The ability of industry to adopt new regulations being put into effect becomes a major concern as emissions regulations evolve.

Further, market dynamics are influenced by business cycles and trends in the automobile industry. The demand for mobile emission catalysts is also influenced by economic variables such as fuel prices, vehicle sales, and consumer taste. In addition to this, market dynamics depend on the preferences of consumers in the automotive sector who are buying cars with advanced pollution control systems that support sustainable development objectives. On the other hand, global trends, which include the widespread use of electric vehicles and insistence on sustainable transportation, affect how catalytic exhaust controls for moving vehicles behave in a given period. However, internal combustion engines still have an important role in automobiles even though electric vehicles have become popular. Emission control systems for internal combustion engines remain essential in complying with emissions standards and reducing the environmental impacts of traditional vehicles.

Covered Aspects:

| Report Attribute/Metric | Details |

|---|---|

| Segment Outlook | Metal Type, Technology, Vehicle Type and Region |

Mobile Emission Catalysts Market Highlights:

Global Mobile Emission Catalysts Market Overview

Mobile Emission Catalysts Market Size was valued at USD 17.60 Billion in 2023. The Mobile Emission Catalysts Market industry is projected to grow from USD 18.87 Billion in 2024 to USD 30.80 Billion by 2032, exhibiting a compound annual growth rate (CAGR) of 6.32% during the forecast period (2024 - 2032). Increasing demand for light-duty automobiles and stringent emission standards are the key market drivers enhancing the market growth.

Source: Secondary Research, Primary Research, MRFR Database and Analyst Review

Mobile Emission Catalysts Market Trends

-

Rising emission standards are driving market growth

Market CAGR for mobile emission catalysts is being driven by the increasing emission standards. The market for mobile emission catalysts is expanding rapidly as emission laws become more stringent. The governments of several nations are establishing rigorous emission rules to decrease hazardous emissions from automobiles, which is boosting demand for mobile emission catalysts. Mobile emission catalysts are used in automobiles to limit the emission of hazardous gases such as carbon monoxide, hydrocarbons, and nitrogen oxides. The growing popularity of electric and hybrid vehicles is also driving demand for mobile emission catalysts, as these vehicles generate hazardous gases during the combustion process. The growing awareness of the adverse impacts of air pollution on human health is also propelling the growth of the mobile emission catalysts market. Mobile emission catalysts are used to limit the emission of hazardous gases from automobiles, hence improving air quality. Increased investments in research and development operations to create better mobile emission catalysts are also propelling the market forward. Market participants are concentrating their efforts on creating mobile emission catalysts that are more efficient and can lower dangerous gas emissions from automobiles to a larger extent. As a result, the increasing stringency of emission standards is propelling the growth of the mobile emission catalysts market.

Electric vehicle usage is quickly increasing as a result of growing concerns about air pollution and increased government attempts to minimize carbon emissions. However, the production of electric vehicles necessitates a substantial amount of energy and resources, resulting in the emission of greenhouse gases. To solve this issue, the usage of mobile emission catalysts in electric vehicles is growing to reduce dangerous gas emissions such as nitrogen oxides, carbon monoxide, and hydrocarbons. Furthermore, rising expenditures in the development of innovative mobile emission catalysts to increase the performance of electric vehicles are likely to propel the mobile emission catalysts market forward. The rising demand for electric vehicles in emerging economies like as China and India is expected to open up attractive potential for mobile emission catalysts market participants.

Mobile Emission Catalysts Market Segment Insights

Mobile Emission Catalysts Metal Type Insights

The Mobile Emission Catalysts Market segmentation, based on metal type includes palladium, platinum, rhodium and others. The palladium segment dominates the mobile emission catalysts market, because of its strong catalytic characteristics and great effectiveness in decreasing hazardous gas emissions from cars. Palladium-based catalysts are widely employed in the automotive sector because they effectively minimize the emission of hazardous gases such as carbon monoxide, hydrocarbons, and nitrogen oxides. The rising demand for palladium-based catalysts in the automobile industry is propelling the palladium segment of the mobile emission catalysts market forward. Furthermore, the increasing use of electric and hybrid vehicles in many nations is boosting demand for palladium-based catalysts, which are used in the production of fuel cells, which are used in electric and hybrid vehicles.

Figure1: Mobile Emission Catalysts Market, by Metal Type, 2022 & 2032 (USD Billion)

Source: Secondary Research, Primary Research, MRFR Database and Analyst Review

Mobile Emission Catalysts Technology Insights

The Mobile Emission Catalysts Market segmentation, based on technology, includes three-way conversion catalyst, four-way conversion catalyst, diesel oxidation catalyst, catalyzed soot filter, selective catalytic reduction, lean GDI catalyst, electrically heated catalytic converter and others. During the predicted time, selective catalytic reduction is expected to expand the fastest and have the largest demand. Industry has a high level of acceptance for mobile emission catalysts. SCR technology is far less expensive than other product types, and this, combined with new technologies, is enticing manufacturers to engage in the sector. When compared to other segments, the SCR system is more cost effective. Furthermore, with the increased use in multiple industries and the cost-effective nature of SCR, the market for mobile emission catalysts around the world is predicted to expand steadily.

Mobile Emission Catalysts Vehicle Type Insights

The Mobile Emission Catalysts Market segmentation, based on vehicle type includes light-duty vehicles, heavy-duty diesel, natural gas vehicles, motorcycles, utility engines, and others. The light-duty vehicles category is the fastest growing segment in the mobile emission catalysts industry, due to the increasing demand for light-duty automobiles in many regions. Increased population, urbanization, and economic expansion in various nations are driving demand for light-duty cars, which in turn is boosting need for mobile emission catalysts. Furthermore, governments in several countries are imposing tight emission restrictions for light-duty vehicles in order to limit hazardous emissions from vehicles. The growing awareness of the adverse impacts of air pollution on human health is also boosting demand for mobile emission catalysts in the Light-Duty Vehicles market.

Mobile Emission Catalysts Regional Insights

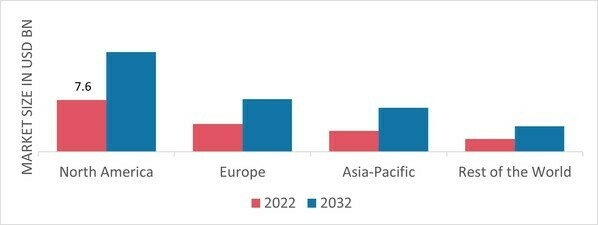

By region, the study provides the market insights into North America, Europe, Asia-Pacific and Rest of the World. North America is the industry leader in mobile emission catalysts, because of the region's government's rigorous pollution regulations. To prevent harmful emissions from vehicles, the United States and Canada have enacted severe emission rules. The region's growing awareness of the adverse impacts of air pollution on human health is also boosting demand for mobile emission catalysts. Furthermore, the region's increasing usage of electric and hybrid vehicles is propelling the expansion of the mobile emission catalysts market.

Further, the major countries studiedin the market reportare The US, Canada, German, France, the UK, Italy, Spain, China, Japan, India, Australia, South Korea, and Brazil.

Figure2: MOBILE EMISSION CATALYSTS MARKET SHARE BY REGION 2022 (USD Billion)

Source: Secondary Research, Primary Research, MRFR Database and Analyst Review

Europe Mobile Emission Catalysts Market accounts for the second-largest market share due to the presence of a high number of car manufacturers in the region. Further, the German Mobile Emission Catalysts Market held the largest market share, and the UK Mobile Emission Catalysts Market was the fastest growing market in the European region.

The Asia-Pacific Mobile Emission Catalysts Market is expected to grow at the fastest CAGR from 2023 to 2032. This is due to the increased demand for autos in the region. Moreover, China’s Mobile Emission Catalysts Market held the largest market share, and the Indian Mobile Emission Catalysts Market was the fastest growing market in the Asia-Pacific region.

Mobile Emission Catalysts Key Market Players & Competitive Insights

Leading market players are investing heavily in research and development in order to expand their product lines, which will help the Mobile Emission Catalysts Market, grow even more. Market participants are also undertaking a variety of strategic activities to expand their footprint, with important market developments including new product launches, contractual agreements, mergers and acquisitions, higher investments, and collaboration with other organizations. To expand and survive in a more competitive and rising market climate, Mobile Emission Catalysts industry must offer cost-effective items.

Manufacturing locally to minimize operational costs is one of the key business tactics used by manufacturers in the Mobile Emission Catalysts industry to benefit clients and increase the market sector. In recent years, the Mobile Emission Catalysts industry has offered some of the most significant advantages to medicine. Major players in the Mobile Emission Catalysts Market, including Cataler Corporation (Japan), Corning Incorporated (US), Heraeus Holding (Germany), N.E. CHEMCAT (Japan), Zeolyst International, Inc (US) and others, are attempting to increase market demand by investing in research and development operations.

Corning Incorporated is a multinational technology corporation based in the United States that specializes in specialized glass, ceramics, and related materials and technologies, including advanced optics, principally for industrial and scientific purposes. Corning Glass Works was the company's name until 1989. Corning sold the Corning Consumer Products Company division (now known as Corelle Brands) to Borden in 1998, divesting its consumer product lines (including CorningWare and Visions Pyroceram-based cookware, Corelle Vitrelle tableware, and Pyrex glass bakeware). In 2019, Corning Incorporated has introduced a novel mobile emissions catalyst system for gasoline engines. The new method is intended to lower nitrogen oxide and hydrocarbon emissions from gasoline engines.

Tenneco (previously Tenneco Automotive and initially Tennessee Gas Transmission Company) is a maker of automotive components as well as aftermarket ride control and emissions solutions. It is a Fortune 500 corporation that was publicly traded on the New York Stock Exchange from November 1999 until it was taken private by Apollo Management in November 2022. Tenneco is based in Northville, Michigan. In 2019, Tenneco Inc. has announced the purchase of Federal-Mogul LLC, a prominent supplier of mobile emissions control technologies. Tenneco's position in the mobile emissions control industry is projected to improve as a result of the acquisition.

Key Companies in the Mobile Emission Catalysts market include

- BASF SE (Germany)

- Solvay (Belgium)

- Johnson Matthey (UK)

- Clariant (Switzerland)

- Umicore AG & Co. KG (Belgium)

- Cataler Corporation (Japan)

- Corning Incorporated (US)

- Heraeus Holding (Germany)

- E. CHEMCAT (Japan)

- Zeolyst International, Inc (US)

Mobile Emission Catalysts Industry Developments

In August 2021, BASF SE has introduced a new mobile emissions catalytic system for gasoline engines. The new method is intended to lower nitrogen oxide and hydrocarbon emissions from gasoline engines.

In July 2020, Johnson Matthey Plc has introduced a new mobile emissions catalyst system for diesel engines. The new technology is intended to lower nitrogen oxide and particulate matter emissions from diesel engines.

In November 2019, Umicore SA has introduced a novel mobile emissions catalyst system for gasoline engines. The new method is intended to lower nitrogen oxide and hydrocarbon emissions from gasoline engines.

Mobile Emission Catalysts Market Segmentation

Mobile Emission Catalysts Market By Metal Type Outlook

- Palladium

- Platinum

- Rhodium

- Others

Mobile Emission Catalysts Market By Technology Outlook

- Three-Way Conversion Catalyst

- Four-Way Conversion Catalyst

- Diesel Oxidation Catalyst

- Catalyzed Soot Filter

- Selective Catalytic Reduction

- Lean GDI Catalyst

- Electrically Heated Catalytic Converter

- Others

Mobile Emission Catalysts Market By Vehicle Type Outlook

- Light-Duty Vehicles

- Heavy-Duty Diesel

- Natural Gas Vehicles

- Motorcycles

- Utility Engines

- Others

Mobile Emission Catalysts Regional Outlook

- North America

- US

- Canada

- Europe

- Germany

- France

- UK

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Australia

- Rest of Asia-Pacific

- Rest of the World

- Middle East

- Africa

- Latin America

Leading companies partner with us for data-driven Insights

Kindly complete the form below to receive a free sample of this Report

Tailored for You

- Dedicated Research on any specifics segment or region.

- Focused Research on specific players in the market.

- Custom Report based only on your requirements.

- Flexibility to add or subtract any chapter in the study.

- Historic data from 2014 and forecasts outlook till 2040.

- Flexibility of providing data/insights in formats (PDF, PPT, Excel).

- Provide cross segmentation in applicable scenario/markets.