Certified Global Research Member

Key Questions Answered

- Global Market Outlook

- In-depth analysis of global and regional trends

- Analyze and identify the major players in the market, their market share, key developments, etc.

- To understand the capability of the major players based on products offered, financials, and strategies.

- Identify disrupting products, companies, and trends.

- To identify opportunities in the market.

- Analyze the key challenges in the market.

- Analyze the regional penetration of players, products, and services in the market.

- Comparison of major players’ financial performance.

- Evaluate strategies adopted by major players.

- Recommendations

Why Choose Market Research Future?

- Vigorous research methodologies for specific market.

- Knowledge partners across the globe

- Large network of partner consultants.

- Ever-increasing/ Escalating data base with quarterly monitoring of various markets

- Trusted by fortune 500 companies/startups/ universities/organizations

- Large database of 5000+ markets reports.

- Effective and prompt pre- and post-sales support.

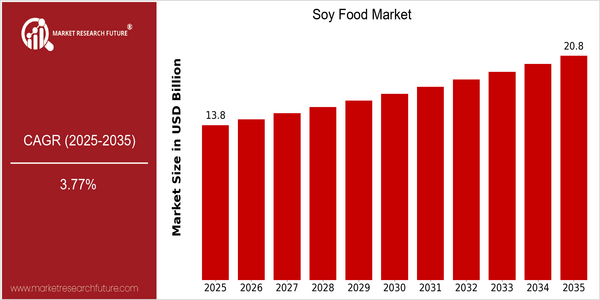

Market Size Snapshot

| Year | Value |

|---|---|

| 2025 | USD 13.84 Billion |

| 2035 | USD 20.8 Billion |

| CAGR (2025-2035) | 3.77 % |

Note – Market size depicts the revenue generated over the financial year

The world market for soy foods is expected to grow steadily, with a projected value of $13,843 million by 2025, which is expected to grow to $2,083 million by 2035. The CAGR is 3.77% for the decade. This is due to the increasing popularity of plant-based diets, driven by health consciousness and environmental concerns. The nutritional value of soy foods, which is mainly based on high-quality vegetable protein and essential amino acids, is increasingly recognized. Product innovation and technological progress are also major growth drivers. In particular, companies are investing in R & D to improve the taste, texture and variety of soy foods, thus attracting a wider audience. The industry's major players, such as Tofurky and Beyond Meat, are constantly launching new products and forming strategic alliances to expand their business. In addition, the use of health-related advertising is expected to continue to increase the consumption of soy foods. These factors will continue to shape the soy food industry, which will continue to grow steadily in the future.

Regional Market Size

Regional Deep Dive

The Soy Food Market is a dynamic market that is experiencing dynamic growth in various regions, driven by the increasing health consciousness, the increasing number of vegetarians and the demand for vegetable-based foods. In North America, the market is characterized by the presence of well-known brands and the innovation of new products, while in Europe, the market for organic and non-GMO soy products is booming. In the Asia-Pacific region, the consumption of soy foods remains the highest, and the consumption is deeply rooted in the people's customs. In the Middle East and Africa, soy foods are gradually entering the market due to the change in eating habits. Latin America is also becoming a major market due to the growing interest in soy-based alternatives. Each region has its own opportunities and challenges, influenced by the cultural preferences, the legal environment, and the economic situation.

Europe

- The European market is seeing a significant shift towards organic and non-GMO soy products, driven by consumer demand for transparency and sustainability, with brands like Alpro leading the way.

- Recent EU regulations aimed at reducing the environmental impact of food production are pushing manufacturers to explore more sustainable soy sourcing options, which is expected to reshape supply chains.

Asia Pacific

- In Asia-Pacific, traditional soy products like tofu and soy milk are being modernized with innovative flavors and packaging, appealing to younger consumers, with companies like Vitasoy expanding their product lines.

- Government initiatives in countries like China are promoting the consumption of plant-based proteins, including soy, as part of a broader strategy to improve public health and reduce meat consumption.

Latin America

- Latin America is witnessing a rise in the popularity of soy-based meat alternatives, with local startups innovating in the space, such as the Brazilian company Fazenda Futuro, which focuses on plant-based protein.

- Cultural shifts towards healthier eating habits and the influence of social media are driving demand for soy foods, leading to increased investment in marketing and product development by established food companies.

North America

- The rise of plant-based diets has led to increased innovation in soy food products, with companies like Beyond Meat and Impossible Foods incorporating soy protein into their offerings to cater to health-conscious consumers.

- Regulatory changes, such as the USDA's support for plant-based protein sources, are encouraging the growth of the soy food market, promoting sustainable agricultural practices and increasing consumer awareness.

Middle East And Africa

- The growing trend of vegetarianism and veganism in urban areas of the Middle East is leading to increased availability of soy-based products, with local brands like Al Ain Food and international players entering the market.

- Regulatory support for health and wellness products is encouraging the development of soy foods, as governments recognize the need for healthier dietary options in response to rising obesity rates.

Did You Know?

“Did you know that soybeans are one of the most versatile crops, used not only for food products but also for industrial applications, including biodiesel and plastics?” — United States Department of Agriculture (USDA)

Segmental Market Size

The Soya Food Market is experiencing a growing demand as consumers turn to soy-based food as a source of plant-based protein. The market is driven by the growing health consciousness, and the importance of a diet rich in plant-based foods with low levels of saturated fat. The demand is also driven by the growing awareness of the impact of livestock farming on the environment. The encouragement of the government to eat a plant-based diet will also support the growth of the market. In North America and Europe, soy-based food products are currently at the early stage of development. In the US, Beyond Meat and Impossible Foods are leading the market. These brands have successfully incorporated soy-based food products, which have been well received by the growing number of flexitarians and vegans. Soya is the main ingredient in meat substitutes, dairy alternatives and snacks. Soy milk and tofu are the most popular products. In addition, macro-economic trends such as the COVID pandemic have accelerated the interest in health-oriented diets, and the trend towards sustainable consumption continues to shape consumer preferences. The application of fermentation and extrusion will also play an important role in improving the taste and texture of soy products, thus attracting more consumers.

Future Outlook

The soya food market will grow steadily from 2025 to 2035, and the market value is expected to increase from $13,884 million to $20,800,000. The compound annual growth rate will be 3.77%. The main reason for this is that the soya bean food industry will continue to develop, and the demand for soya bean food will be driven by the increasing public demand for health-conscious and environment-friendly vegetarian food. Soya bean food will become more and more popular, and the penetration rate will increase from 20.0% to 30.0% in 2035, compared with 20.0% in 2025. The public is more aware of the health benefits of soy products, such as reducing cholesterol and supplying essential amino acids. The public will gradually change their diets. Then, the key development of science and technology and the trend of national policies will also have a certain impact on the market. The process and formula of soya bean food will be further improved, and the taste and texture will be further improved, and the public's love for soya bean food will also be further developed. In addition, the policy of promoting green agriculture and promoting the consumption of soya bean food will also help to promote the development of the industry. The trend of soya bean food will be further developed in the field of health-conscious and environment-friendly vegetarian food, and soya bean food will be more and more popularized. So the soya bean food industry must be flexible to meet the needs of the public.

Covered Aspects:| Report Attribute/Metric | Details |

|---|---|

| Market Size Value In 2023 | USD 42.8 Billion |

| Growth Rate | 4.34% (2024-2032) |

Soy Food Market Highlights:

Leading companies partner with us for data-driven Insights

Kindly complete the form below to receive a free sample of this Report

Tailored for You

- Dedicated Research on any specifics segment or region.

- Focused Research on specific players in the market.

- Custom Report based only on your requirements.

- Flexibility to add or subtract any chapter in the study.

- Historic data from 2014 and forecasts outlook till 2040.

- Flexibility of providing data/insights in formats (PDF, PPT, Excel).

- Provide cross segmentation in applicable scenario/markets.