Certified Global Research Member

Key Questions Answered

- Global Market Outlook

- In-depth analysis of global and regional trends

- Analyze and identify the major players in the market, their market share, key developments, etc.

- To understand the capability of the major players based on products offered, financials, and strategies.

- Identify disrupting products, companies, and trends.

- To identify opportunities in the market.

- Analyze the key challenges in the market.

- Analyze the regional penetration of players, products, and services in the market.

- Comparison of major players’ financial performance.

- Evaluate strategies adopted by major players.

- Recommendations

Why Choose Market Research Future?

- Vigorous research methodologies for specific market.

- Knowledge partners across the globe

- Large network of partner consultants.

- Ever-increasing/ Escalating data base with quarterly monitoring of various markets

- Trusted by fortune 500 companies/startups/ universities/organizations

- Large database of 5000+ markets reports.

- Effective and prompt pre- and post-sales support.

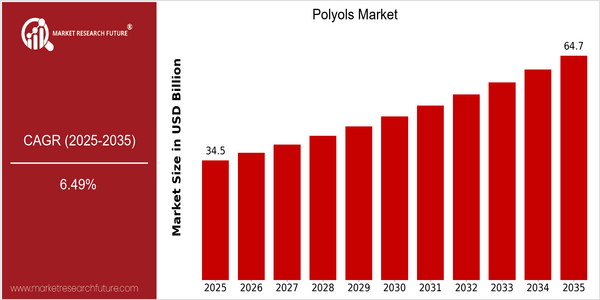

Market Size Snapshot

| Year | Value |

|---|---|

| 2025 | USD 34.47 Billion |

| 2035 | USD 64.66 Billion |

| CAGR (2025-2035) | 6.49 % |

Note – Market size depicts the revenue generated over the financial year

The market for polyols is expected to grow significantly over the coming years. The market is expected to reach a value of $34.75 billion by 2025, and reach a value of $ 64.66 billion by 2035, growing at a CAGR of 6.49% over the next ten years. The market for polyols is expected to grow in line with the growing demand for flexible and rigid foams, which are important in the construction, automotive and consumer goods industries. The growing focus on sustainability and the trend towards biopolyols will also drive the market, as manufacturers seek to reduce their carbon footprint and meet regulatory requirements for environmentally friendly products. The food and beverage industry is also expected to benefit from the growing trend towards low-fat and sugar-free products. As a result, companies such as BASF, Dow and Covestro are investing heavily in research and development and strategic alliances in order to develop new polyol formulations. Product launches aimed at meeting the specific requirements of individual industries will also further strengthen the market position of these companies and contribute to the overall growth of the polyols market.

Regional Market Size

Regional Deep Dive

The Polyols Market is growing at a substantial rate in many regions of the world, driven by the growing demand for polyols from the construction, automobile and consumer goods industries. In North America, the market is characterized by a strong focus on innovation and sustainability. Companies are investing in bio-based polyols to meet the stricter environmental regulations. In Europe, the market is mature with strict regulations promoting the use of sustainable materials. The Asia-Pacific region is growing rapidly due to the increasing industrialization and urbanization. The Middle East and Africa are growing with increasing construction activity. Latin America is slowly but surely adopting polyols in many applications, but at a lower rate than in other regions.

Europe

- The European Union's Green Deal is pushing for a circular economy, which has led to increased investments in recycling technologies for polyols, with companies like Covestro and Reverdia at the forefront.

- Regulatory changes regarding chemical safety have prompted manufacturers to reformulate their products, leading to a rise in demand for non-toxic and sustainable polyols in the region.

Asia Pacific

- China's rapid industrialization has resulted in a surge in demand for polyols in the automotive and construction sectors, with local companies like Wanhua Chemical making significant investments in production capacity.

- The rise of the middle class in countries like India and Indonesia is driving demand for consumer goods that utilize polyols, leading to increased market opportunities for both local and international players.

Latin America

- Brazil's growing automotive industry is increasingly utilizing polyols in the production of lightweight materials, with companies like Braskem focusing on developing bio-based alternatives.

- Regulatory frameworks in countries like Mexico are gradually evolving to support the use of sustainable materials, which is expected to enhance the adoption of polyols in various applications.

North America

- The U.S. Environmental Protection Agency (EPA) has introduced new regulations encouraging the use of bio-based polyols, prompting companies like BASF and Dow to innovate in sustainable product lines.

- Recent advancements in technology have led to the development of high-performance polyols that enhance the properties of polyurethane foams, with companies such as Covestro leading the charge in this innovation.

Middle East And Africa

- The UAE's Vision 2021 initiative is promoting sustainable development, which is influencing the adoption of eco-friendly polyols in construction and insulation applications.

- In South Africa, government programs aimed at boosting local manufacturing are encouraging investments in polyol production, with companies like Sasol exploring new market opportunities.

Did You Know?

“Did you know that polyols are not only used in the production of flexible and rigid foams but also play a crucial role in the manufacturing of food additives and pharmaceuticals?” — Polyurethanes Technical Association

Segmental Market Size

Polyols, especially bio-based polyols, are experiencing considerable growth, driven by increasing demand for sustainable materials. The demand is also driven by a rising awareness of the environment, which is encouraging manufacturers to adopt eco-friendly alternatives, as well as government regulations encouraging the use of renewable resources. Furthermore, technological advances are enabling more efficient production, which is further increasing demand. The bio-based polyols market is now at the stage of commercialization, with BASF and Covestro among the first to integrate these materials into their product portfolios. The main applications are for flexible and rigid foams in the furniture, automotive and construction industries. There are several trends driving the market: the circular economy, sustainable development and the need to reduce the carbon footprint of products. Enzymatic and green chemistry are driving the market, making it more accessible and cost-effective for manufacturers.

Future Outlook

The polyols market is expected to experience a CAGR of 6.49% from 2025 to 2035, with a projected market size of $34.47 billion to $64.66 billion. This growth is due to the increasing demand for polyols in various applications such as flexible and rigid foams, adhesives, and coatings, driven by the growth in the construction and automobile industries. In the coming years, bio-based polyols are expected to increase in market share, with a penetration rate of more than 30% by 2035, as manufacturers focus on reducing their carbon footprint and complying with stricter regulations. Also, key technological advancements, especially in polyol production processes, are expected to enhance efficiency and reduce costs, further driving market growth. Moreover, innovations such as the development of high-performance polyols and the integration of circular economy principles are expected to reshape the competitive landscape. Government policies that encourage the use of green chemistry and sustainable materials will also stimulate market growth. The polyols market is expected to evolve in line with the growing demand for sustainable and smart materials.

Covered Aspects:| Report Attribute/Metric | Details |

|---|---|

| Growth Rate | 8% (2023-2030) |

Polyols Market Highlights:

Leading companies partner with us for data-driven Insights

Kindly complete the form below to receive a free sample of this Report

Tailored for You

- Dedicated Research on any specifics segment or region.

- Focused Research on specific players in the market.

- Custom Report based only on your requirements.

- Flexibility to add or subtract any chapter in the study.

- Historic data from 2014 and forecasts outlook till 2040.

- Flexibility of providing data/insights in formats (PDF, PPT, Excel).

- Provide cross segmentation in applicable scenario/markets.