Global Industrial Roundwood Market Overview

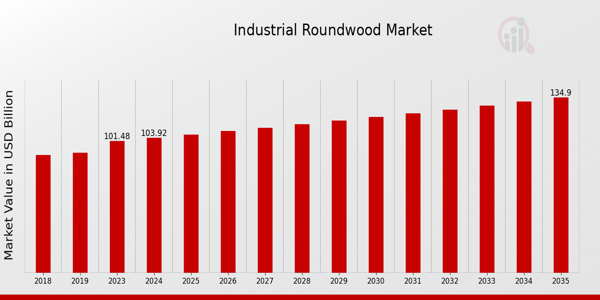

Industrial Roundwood Market Size was estimated at 101.48 (USD Billion) in 2023. The Industrial Roundwood Industry is expected to grow from 103.92 (USD Billion) in 2024 to 135.0 (USD Billion) by 2035. The Industrial Roundwood Market CAGR (growth rate) is expected to be around 2.4% during the forecast period (2025 - 2035).

Industrial Roundwood Market Drivers

Key Industrial Roundwood Market Trends Highlighted

Key market drivers including the increased emphasis on eco-friendly construction methods and the growing demand for sustainable building materials have a substantial impact on the industrial roundwood market. Roundwood is a renewable resource that satisfies the growing need from enterprises to lessen their carbon footprints.

Demand for Roundwood is also influenced by the expansion and recovery of the building industry in different areas, especially in infrastructural and residential projects.

Additionally, Roundwood is becoming increasingly popular as a versatile raw material as a result of the growing use of engineered wood products. Potential technological developments in supply chain management and wood processing are among the market's opportunities.

Innovations in timber production and harvesting methods can improve quality and efficiency, allowing businesses to better satisfy customer expectations. Additionally, companies have an opportunity to stand out in the market thanks to the growing trend toward sustainable forestry certification criteria.

Companies that prioritize responsible sourcing and sustainable practices are likely to capture a more significant share of environmentally conscious consumers.

Recent times have seen a trend towards digitization within the industry, allowing for improved tracking and management of roundwood resources. The adoption of digital tools aids in optimizing logistics and enhancing transparency in supply chains.

Concurrently, urbanization and a demand for greater aesthetic appeal in construction materials are prompting designers and architects to explore varied applications of Roundwood, from furniture to decorative elements.

As these trends continue to evolve, the industrial roundwood market is expected to adapt and thrive, aligning with broader shifts toward sustainability and innovative design.

Sustainable Construction Practices

The growing trend towards sustainable construction practices is a crucial driver of the Industrial Roundwood Market. As environmental concerns become more prominent, industries are increasingly adopting green building techniques that prioritize the use of renewable resources, including Roundwood.

Wood, being a natural and biodegradable material, offers an eco-friendly alternative to concrete and steel in construction processes. The push for sustainability is driving architects, builders, and developers to reconsider their material choices.

With legislation and regulations increasingly favoring eco-friendly materials, the demand for industrial roundwood has seen a significant rise. Moreover, consumers are becoming increasingly aware of their environmental footprint, which further fuels the demand for sustainably sourced materials.

As Roundwood comes from managed forest sources, it can play a pivotal role in reducing emissions and creating a more sustainable construction model. Furthermore, the carbon sequestration capability of trees enhances the attractiveness of roundwood as a construction material in eco-conscious markets.

The advancement of technologies that improve the efficiency of Roundwood harvesting and processing has also led to increased market supply, meeting the growing consumption demands while ensuring sustainability.

Overall, the pivot towards sustainable construction practices enhances the growth prospects of the Industrial Roundwood Market as builders and developers align their projects with environmental responsibility.

Rising Demand from the Furniture and Wood Products Industry

The expanding furniture and wood products industry significantly contributes to the growth of the Industrial Roundwood Market. As consumer preferences shift towards wooden furniture, whether for aesthetic appeal, durability, or sustainability, the demand for high-quality roundwood is on the rise.

Manufacturers are incorporating wooden elements into their products, aligning with modern design trends that favor natural materials. Additionally, the growing middle-class population, especially in emerging economies, has led to increased spending on home furnishing and décor.

This trend has created a robust market for furniture makers that rely heavily on Roundwood as a key raw material. As the preferences for style and eco-friendliness converge, the industrial roundwood market is well-positioned for sustained growth fueled by continual innovation in furniture design and functionality.

Increased Government Support and Regulations

Government policies and regulations supporting the forestry sector greatly influence the Industrial Roundwood Market. Many nations are implementing supportive frameworks to promote sustainable forestry practices, encouraging sustainable harvesting and management of forest resources.

Initiatives aimed at combating deforestation and preserving biodiversity have led to stricter regulations on the logging processes, which in turn have bolstered the legal roundwood market.

By incentivizing sustainable forestry through subsidies, tax breaks, and investment in infrastructure, governments worldwide are ensuring a steady supply of roundwood while promoting responsible consumption. As a result, the Industrial Roundwood Market stands to benefit from these initiatives that not only enhance the sustainability of forest resources but also drive economic growth in the industry.

Industrial Roundwood Market Segment Insights

Industrial Roundwood Market Application Insights

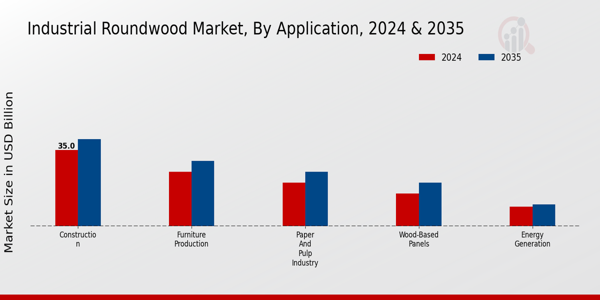

The Industrial Roundwood Market was a diverse sector with significant applications across various industries. In 2024, the market was poised for notable valuations, with Construction leading the way at 35.0 USD Billion, establishing itself as a dominant force due to the continual demand for infrastructure and housing development.

The Furniture Production segment also held a significant position, valued at 25.0 USD Billion in 2024, reflecting consumer trends favoring sustainable and aesthetically pleasing wood products. Coming next, the Paper and Pulp Industry reached 20.0 USD Billion, driven by the ongoing need for paper products in both educational and corporate settings.

The Wood-Based Panels segment contributed 15.0 USD Billion, reflecting its essential role in manufacturing and building applications. Moreover, the Energy Generation segment, valued at 8.92 USD Billion, played an increasingly pivotal role as industries shifted towards renewable energy sources, harnessing wood as a biofuel.

Collectively, these sectors underlined the importance of applications within the Industrial Roundwood Market, showcasing various growth drivers such as urbanization, changing consumer preferences, and sustainability initiatives.

Market trends indicated a shift toward eco-friendly production, creating opportunities for innovation in the manufacturing processes across these segments. While challenges like price fluctuations and sustainable sourcing remain, the overall market is likely to demonstrate resilience and a clear trajectory for expansion into 2035, where all segments are expected to experience growth, evidencing the robust nature of the Industrial Roundwood Market.

This market growth trajectory was supported by consistent demand across diverse applications, reinforcing its critical role in both economic and environmental conversations worldwide.

Industrial Roundwood Market Wood Type Insights

When examining the diverse composition, Softwood dominates the market due to its extensive applications in construction and paper production, facilitating the growing demand for versatile and lightweight materials. Hardwood, on the other hand, is appreciated for its durability and strength, finding its significance in the furniture and flooring industries, as well as in high-quality crafts, making it a staple in the luxury segment of the market.

Tropical Wood also plays a notable role, often sought after for its unique aesthetic appeal and robustness, gaining traction in luxury and sustainable projects. The segmentation of the Industrial Roundwood Market reveals varying demands driven by industry requirements; the growth drivers include a rising construction market, increased consumption of wood-based products, and environmental considerations.

However, challenges such as deforestation regulations and fluctuating timber prices impact the sector's dynamics. With a projected increase in demand, the Industrial Roundwood Market revenue is poised to benefit from these trends and developments as it moves toward 2035

Industrial Roundwood Market Processing Method Insights

The Industrial Roundwood Market, particularly the Processing Method segment, is poised for growth. This segment includes key processing methods such as Sawnwood, Veneer, Plywood, and Laminated Wood, all of which play significant roles in the overall market.

Sawnwood remains a crucial component, dominating due to its versatility in construction and furniture manufacturing. Veneer is recognized for its aesthetic appeal and efficient use of raw materials, thus holding a substantial position within the market.

Plywood stands out for its strength and durability, making it a preferred choice in various applications, including flooring and cabinetry. Laminated Wood is gaining momentum for its innovative uses and environmental benefits.

The demand for eco-friendly products and sustainable practices is a significant driver for this segment, presenting opportunities for growth. Moreover, regional variations in construction trends and preferences will impact market growth across different areas. As a result, the Industrial Roundwood Market revenue is influenced by these processing methods, reflecting broader consumer trends and demands.

Industrial Roundwood Market End Use Industry Insights

Key sectors within this domain, such as Construction, Furniture Manufacturing, Packaging, and the Energy Sector, play a pivotal role in driving demand for industrial roundwood.

The Construction industry, with its reliance on wood for framing, flooring, and finishes, continues to be a major contributor, while Furniture Manufacturing capitalizes on Roundwood for high-quality furniture production. The Packaging sector is significant as it increasingly adopts sustainable materials, with round wood serving as an eco-friendly option.

Additionally, the Energy Sector has embraced biomass from Roundwood as a renewable energy source, demonstrating its versatility. The overall growth is supported by trends towards sustainable practices across industries, although challenges such as supply chain disruptions may impact availability.

With insights reflected in Industrial Roundwood Market statistics, the segmentation of this market underscores the diverse applications and essential nature of Roundwood in these key sectors.

Industrial Roundwood Market Regional Insights

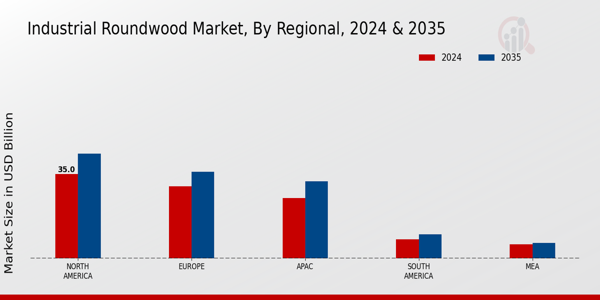

The Industrial Roundwood Market showcased significant regional dynamics, with North America leading the segment due to its valuation of 35.0 USD Billion in 2024 and projected growth to 43.5 USD Billion by 2035, which indicates its strong demand and consumption patterns for roundwood products.

Europe followed closely, valued at 30.0 USD Billion in 2024 and anticipated to reach 36.0 USD Billion in 2035, reflecting a mature market with established industries reliant on Roundwood. The APAC region, valued at 25.0 USD Billion in 2024, showed promising growth potential as it progresses to 32.0 USD Billion by 2035, driven by increased construction and manufacturing activities.

South America and MEA represented smaller yet emerging markets, with South America valued at 8.0 USD Billion in 2024 and growing to 10.0 USD Billion by 2035, while MEA stands at 5.92 USD Billion in 2024 and is expected to reach 6.5 USD Billion by 2035.

Despite their smaller valuations, these regions offered substantial opportunities for expansion and investment as industrial applications of Roundwood continue to evolve. The segmentation illustrated a diverse landscape where North America and Europe dominate, accounting for a majority share of the Industrial Roundwood Market revenue, while APAC presents as a key growth hub.

Market growth in these regions was influenced by factors such as increasing urbanization, construction activities, and sustainable practices driving the demand for industrial roundwood.

Industrial Roundwood Market Key Players and Competitive Insights

The Industrial Roundwood Market is characterized by a dynamic competitive landscape driven by a variety of factors that affect supply and demand. With increasing construction activities and a surge in sustainable building practices, key players within the market constantly adapt to changing consumer preferences and regulatory environments.

The competition is intense, with firms needing to differentiate their offerings while ensuring compliance with environmental standards and sustainable sourcing practices. This market has seen fluctuations in pricing owing to influences like raw material availability, market demand in different regions, and advancements in technology.

Competitive strategies are often centered around product innovation, branding, and distribution channels, in addition to traditional market expansion efforts.

Weyerhaeuser Company stands out within the Industrial Roundwood Market due to its extensive experience and robust operational capabilities. As one of the largest forest products companies, Weyerhaeuser has a strong market presence by leveraging its vast timberland resources and advanced manufacturing processes.

The company has honed its competitive advantages through a commitment to sustainability and responsible forest management, which resonates well with environmentally conscious consumers and businesses. Weyerhaeuser's diverse product portfolio and strategic partnerships further enhance its influence within the market, allowing it to respond adeptly to market demands while maintaining a focus on customer needs.

The company's investment in innovative technologies and efficient supply chain management also positions it favorably amidst competitors, aiding in cost control and product delivery timelines.

Oregon Timber Frame is another notable entity within the Industrial Roundwood Market, specializing in providing high-quality timber products. Known for its craftsmanship and dedication to producing eco-friendly materials, Oregon Timber Frame has carved a niche in the market that attracts both builders and architects looking for sustainable wood options.

The company emphasizes the use of locally sourced timber, which not only supports local economies but also minimizes the environmental impact associated with transportation. Oregon Timber Frame is recognized for its strong customer service and innovative designs that cater to a variety of construction needs.

The company's focus on blending tradition with modern techniques allows it to maintain a competitive edge while continuously adapting to industry trends and customer preferences. Furthermore, its proactive approach to engaging with sustainable practices ensures a loyal customer base that values environmental responsibility.

Key Companies in the Industrial Roundwood Market Include

- Weyerhaeuser Company

- Oregon Timber Frame

- Canfor Corporation

- APG Inc

- Tolko Industries Ltd

- Resolute Forest Products

- GeorgiaPacific LLC

- Metsä Group

- Setra Group

- Sappi Limited

- West Fraser Timber Co Ltd

- Stora Enso Oyj

- Interfor Corporation

- Energex

- International Paper Company

Industrial Roundwood Market Developments

Recent developments in the Industrial Roundwood Market have highlighted significant activities among key players. Weyerhaeuser Company and Canfor Corporation have been focused on increasing their production capacity to meet rising demand, responding to trends in sustainable building practices.

Additionally, Tolko Industries Ltd and West Fraser Timber Co Ltd reported an increase in their market valuation due to heightened interest in environmentally friendly wood products. Emerging reports about the resilient supply chain strategies of APG Inc. and Resolute Forest Products are indicating a positive outlook for the overall market.

In terms of mergers and acquisitions, Georgia-Pacific LLC has announced the acquisition of a smaller timber firm to expand its operational footprint, enhancing its competitiveness. Stora Enso Oyj has also entered into an agreement to integrate assets from an acquired company, aiming to strengthen its position in the European market.

Current affairs point towards an evolving landscape where companies such as Metsä Group and Interfor Corporation are capitalizing on the need for sustainable timber as key policy changes promote eco-friendly materials. The overall market is witnessing growth driven by increasing investments and strategic partnerships among leading firms, enhancing resilience and adaptability in a fluctuating economic environment.

Industrial Roundwood Market Segmentation Insights

Industrial Roundwood Market Application Outlook

- Construction

- Furniture Production

- Paper and Pulp Industry

- Wood-Based Panels

- Energy Generation

Industrial Roundwood Market Wood Type Outlook

- Softwood

- Hardwood

- Tropical Wood

Industrial Roundwood Market Processing Method Outlook

- Sawnwood

- Veneer

- Plywood

- Laminated Wood

Industrial Roundwood Market End Use Industry Outlook

- Construction

- Furniture Manufacturing

- Packaging

- Energy Sector

Industrial Roundwood Market Regional Outlook

- North America

- Europe

- South America

- Asia Pacific

- Middle East and Africa

|

Report Attribute/Metric

|

Details

|

|

Market Size 2023

|

101.48(USD Billion)

|

|

Market Size 2024

|

103.92(USD Billion)

|

|

Market Size 2035

|

135.0(USD Billion)

|

|

Compound Annual Growth Rate (CAGR)

|

2.4% (2025 - 2035)

|

|

Report Coverage

|

Revenue Forecast, Competitive Landscape, Growth Factors, and Trends

|

|

Base Year

|

2024

|

|

Market Forecast Period

|

2025 - 2035

|

|

Historical Data

|

2019 - 2024

|

|

Market Forecast Units

|

USD Billion

|

|

Key Companies Profiled

|

Weyerhaeuser Company, Oregon Timber Frame, Canfor Corporation, APG Inc, Tolko Industries Ltd, Resolute Forest Products, GeorgiaPacific LLC, Metsä Group, Setra Group, Sappi Limited, West Fraser Timber Co Ltd, Stora Enso Oyj, Interfor Corporation, Energex, International Paper Company

|

|

Segments Covered

|

Application, Wood Type, Processing Method, End Use Industry, Regional

|

|

Key Market Opportunities

|

Sustainable wood sourcing initiatives, Growing demand for eco-friendly materials, Expansion of the construction industry, Increased use of renewable energy, Rise in furniture manufacturing

|

|

Key Market Dynamics

|

supply chain disruptions, environmental regulations, technological advancements, fluctuating demand, sustainable sourcing practices

|

|

Countries Covered

|

North America, Europe, APAC, South America, MEA

|

Frequently Asked Questions (FAQ) :

The Industrial Roundwood Market was valued at 103.92 USD Billion in 2024.

The market is anticipated to reach a value of 135.0 USD Billion by 2035.

The expected CAGR for the market during the forecast period is 2.4%.

North America held the largest market share at 35.0 USD Billion in 2024.

The Construction application segment is expected to be valued at 40.0 USD Billion in 2035.

Weyerhaeuser Company is one of the major players in the Industrial Roundwood Market.

The Furniture Production application segment is projected to grow from 25.0 USD Billion in 2024 to 30.0 USD Billion in 2035.

The APAC region's market size is expected to grow from 25.0 USD Billion in 2024 to 32.0 USD Billion in 2035.

The Energy Generation application was valued at 8.92 USD Billion in the year 2024.

The Paper and Pulp Industry application is expected to be valued at 25.0 USD Billion by 2035.