Leading market players are investing heavily in research and development to expand their product lines, which will help the Asia Pacific Organic Baby Food market grow even more. Market participants are also undertaking various strategic initiatives to expand their global footprint, with important market developments including new product launches, contractual agreements, mergers and acquisitions, higher investments, and collaboration with other organizations. To expand and survive in a more competitive and rising market climate, the Asia Pacific Organic Baby Food industry must offer cost-effective items.

Manufacturing locally to minimize operational costs is one of the key business tactics manufacturers use in the Asia Pacific Organic Baby Food industry to benefit clients and increase the market sector. In recent years, the Asia Pacific Organic Baby Food industry has offered some of the most significant advantages to the baby food market.

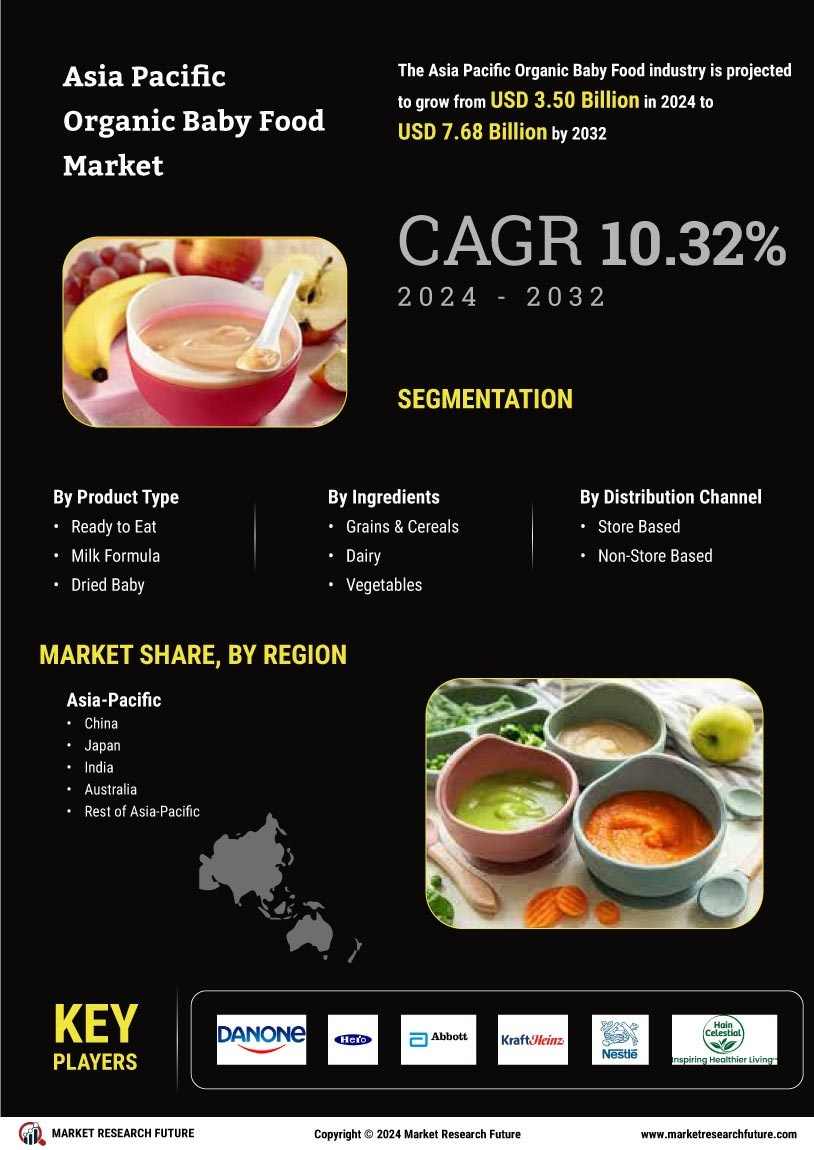

Major players in the Asia Pacific Organic Baby Food market, including Danone SA (France), Hero Group (Switzerland), Nestle S.A. (Switzerland), Abbott Laboratories (U.S.), Kraft Heinz Foods Company (U.S.), Hain Celestial Group (U.S.), Bellamy's Australia (Australia), and others are attempting to increase market demand by investing in research and development operations.

Danone SA, a multinational food company based in France, operates a prominent organic baby food business under its "Specialized Nutrition" division. Committed to promoting health and well-being, Danone offers a range of organic baby food products made from carefully sourced organic ingredients, providing parents with nutritious and natural options for their infants and young children. With a global presence and a focus on quality, safety, sustainability, and responsible practices, Danone's organic baby food offerings cater to the specific nutritional needs of babies and support their growth and development during their early stages.

Nestlé SA, a leading global food and beverage company, includes a robust organic baby food business in its portfolio. Committed to providing safe and nutritious products, Nestle's organic baby food offerings are made from carefully selected organic ingredients, ensuring they are free from synthetic pesticides and GMOs. With a focus on supporting early childhood nutrition, Nestlé offers a diverse range of organic baby cereals, purees, and infant formulas designed to cater to the needs of growing infants and toddlers.

Nestlé's extensive distribution network allows parents worldwide to access organic options for their little ones, backed by the company's commitment to quality, safety, and sustainability in its operations.

Leave a Comment