Summary Overview

Data Center Hosting Services Market Overview

The global data center hosting services market is undergoing rapid expansion, driven by the increasing adoption of cloud computing, big data analytics, artificial intelligence (AI), and the growing demand for managed hosting solutions. As businesses across various sectors continue to digitize their operations, the need for scalable, secure, and efficient data center hosting services is intensifying. This market is supported by continuous advancements in infrastructure, such as high-performance servers, energy-efficient cooling systems, and robust security protocols.

Our report offers a detailed analysis of emerging procurement trends, opportunities for cost optimization through strategic sourcing, and innovative hosting solutions. Furthermore, it outlines key challenges in the market and highlights the growing role of digital procurement tools in forecasting market needs, allowing businesses to navigate and adapt to market changes. The role of procurement management in the data center hosting services sector has never been more crucial, as companies leverage market intelligence and procure analytics to enhance supply chain management and service delivery.

The outlook for the data center hosting services market is promising, with several trends and projections indicating robust growth through 2032:

-

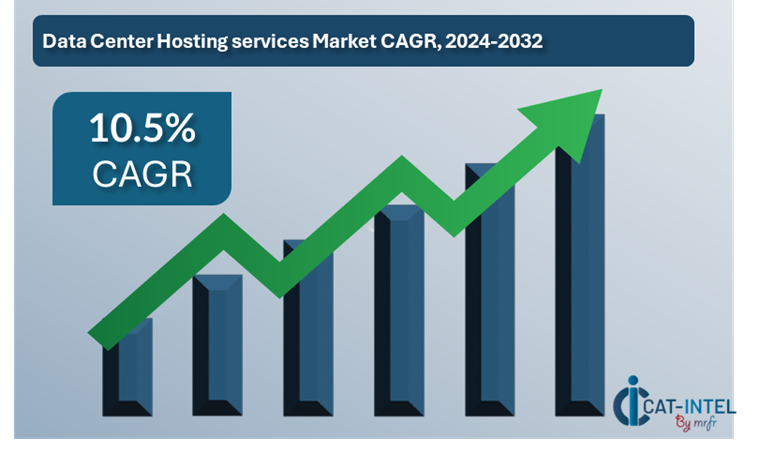

Market Size: The global data center hosting services market is projected to reach USD 103.4 billion by 2032, with a compound annual growth rate (CAGR) of 10.5% from 2024 to 2032.

Key Growth Drivers:

-

Cloud Adoption: The rapid shift to cloud-based services across various industries is a major growth driver for the data center hosting services market. Increased reliance on cloud infrastructure for data storage, backup, and disaster recovery is propelling the demand for hosting services. -

Big Data and AI: As big data analytics and AI technologies become more integral to business operations, the need for high-performance data centers to manage and process massive datasets is on the rise. -

Cybersecurity: The growing number of cyber threats has increased the demand for secure hosting solutions. Companies are investing in data centers with advanced security features to protect sensitive information. -

Edge Computing: The increasing demand for low-latency applications is driving the adoption of edge computing, which is dependent on a distributed network of data centers closer to end-users. -

Sustainability: Energy-efficient data centers, powered by renewable energy sources, are gaining popularity as businesses focus on sustainability. Many providers are investing in green data center technologies, helping reduce environmental impact.

Key Sectors Driving Growth:

-

IT and Telecommunications: Data centers are the backbone of the telecommunications industry, hosting cloud services, data storage, and network management solutions. The telecom sector's move toward 5G and next-gen networks is driving demand for hosting services. -

E-commerce: E-commerce platforms require reliable and scalable hosting solutions to support their large-scale data storage, transaction processing, and real-time data analytics needs. -

Financial Services: With the rise of digital banking and fintech services, financial institutions are increasingly seeking secure and high-performance hosting solutions to manage transaction data and provide uninterrupted services. -

Healthcare: The healthcare industry's shift to digital records and telemedicine is creating new opportunities for data center hosting services providers to support sensitive patient data and ensure HIPAA compliance.

Key Trends and Sustainability Outlook:

-

Energy Efficiency: Data center providers are adopting energy-efficient designs, using advanced cooling technologies to minimize power consumption. Data centers with high energy ratings are increasingly in demand. -

Modular Data Centers: The rise of modular data centers, which can be expanded as needed, offers flexibility and cost efficiency to organizations with fluctuating hosting needs. -

Hyperscale Data Centers: Large-scale data centers built by tech giants like Amazon, Google, and Microsoft are becoming more prevalent, offering economies of scale and high performance. -

Green Data Centers: Sustainable practices, such as the use of renewable energy, efficient water use, and environmentally friendly building materials, are growing in importance as businesses strive for carbon neutrality.

Overview of Market Intelligence Services for the Data Center Hosting Services Market:

Recent analyses show fluctuations in data center hosting services pricing due to varying energy costs and technological advancements in data center infrastructure. To tackle these challenges, market reports provide detailed cost forecasts, procurement strategies, and vendor performance evaluations to assist stakeholders in making informed decisions. By leveraging these reports, organizations can manage pricing volatility while ensuring access to high-performance, secure, and cost-efficient hosting solutions. Strategic sourcing practices, backed by market intelligence, are vital in managing procurement risks and securing a competitive edge in the rapidly evolving data center hosting services landscape.

Procurement Intelligence for Data Center Hosting Services Market: Category Management and Strategic Sourcing

To stay ahead in the competitive data center hosting services market, businesses are optimizing procurement strategies through spend analysis solutions, focusing on vendor spend analysis, and enhancing supply chain efficiency with market intelligence. Procurement category management and strategic sourcing are critical for ensuring cost-effective procurement and the timely availability of high-quality hosting services. With the increasing importance of data security, scalability, and operational efficiency, leveraging strategic sourcing and supplier performance management is essential for organizations to gain a competitive advantage in the market.

Pricing Outlook for Data Center Hosting Services Market: Spend Analysis

The data center hosting services market is currently navigating a dynamic pricing landscape influenced by factors such as rising operational costs, growing demand for cloud computing, and technological advancements. This evolving market environment reflects changes in data consumption patterns and infrastructure requirements.

Line chart illustrating the pricing outlook for the data center hosting services market from 2024 to 2032. The chart shows the projected price trends, with prices gradually increasing over the years.

Our advanced analysis indicates a steady growth trajectory in data center hosting prices driven by several key factors, including:

-

Rising Operational Costs: Increased expenses related to energy consumption, cooling technologies, and infrastructure maintenance are contributing to overall pricing increases. -

Surge in Demand: The increasing demand for cloud services, data storage, and computing power due to digital transformation and data-intensive applications is significantly impacting the market. -

Technological Advancements: The need for more advanced technologies such as AI, ML, and IoT solutions is driving the demand for scalable and robust data center services, which is influencing pricing models. -

Supply Chain Challenges: Global supply chain disruptions, particularly in critical components like servers and networking equipment, are affecting the cost and availability of infrastructure, leading to potential price increases.

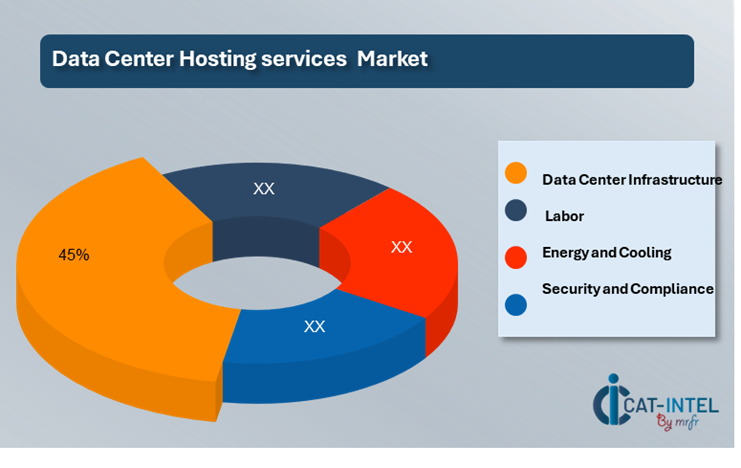

Cost Breakdown for Data Center Hosting Services Market: Cost Saving Opportunities

- Data Center Infrastructure (45%)

-

Description: Represents the bulk cost associated with the physical infrastructure, including servers, storage devices, network equipment, and data center construction. These costs are influenced by factors such as hardware quality, location, and energy efficiency. -

Trends: Data center infrastructure costs have seen gradual increases due to supply chain disruptions, the rising cost of components, and the need for more advanced, scalable systems. The demand for higher capacity data centers driven by the expansion of cloud services and data-intensive applications is expected to further influence infrastructure costs. Energy-efficient technologies are becoming increasingly important to reduce long-term operational expenses.

- Labor (XX%)

- Energy and Cooling (XX%)

- Security and Compliance (XX%)

Cost saving opportunity: Negotiation Lever and Purchasing Negotiation Strategies

In the data center hosting services market, cost savings can be achieved through strategic procurement. Negotiating bulk discounts on hardware and energy, prioritizing energy-efficient technologies, and leveraging cloud optimization for shared infrastructure reduce overall costs. Long-term supplier relationships and competition between vendors can also lead to better pricing. Additionally, focusing on automation and AI integration minimizes labour costs, while sustainable practices can secure favourable terms for renewable energy contracts. These strategies help data centers lower operational costs and improve profitability.

Supply and Demand Overview of the Data Center Hosting Services Market: Demand-Supply Dynamics and Buyer Intelligence for Effective Supplier Relationship Management (SRM)

The data center hosting services market is experiencing rapid growth driven by increased digital transformation, demand for cloud computing, and the rise of data-intensive technologies. The demand is particularly strong due to the growing need for secure data storage, processing power, and high-performance computing for businesses across sectors.

Demand Factors:

-

Digital Transformation: Businesses are increasingly adopting cloud computing, IoT, AI, and big data technologies, significantly boosting demand for data center hosting services to store and process vast amounts of data. -

Cloud Computing Growth: The shift toward cloud-based solutions, driven by cost-efficiency and scalability, is amplifying the need for reliable data center hosting services. -

Data-Intensive Applications: Industries such as finance, healthcare, and e-commerce require powerful data infrastructure to support the growing demand for real-time analytics and services. -

Remote Work and Collaboration Tools: The rise of remote work and digital collaboration tools is driving the need for secure and scalable data storage and hosting solutions.

Supply Factors:

-

Geographic Concentration: A few key regions, particularly in North America, Europe, and Asia, dominate the data center hosting market. These regions have the infrastructure and investment to meet growing global demand. -

Technological Advancements: Innovations in server hardware, cooling technologies, and energy-efficient systems improve supply capacity and reduce operational costs, meeting the demands of modern data center clients. -

Energy Availability: The availability of affordable and renewable energy sources is essential for the cost-effective operation of data centers, impacting supply and pricing. -

Market Competition: The growing competition among cloud providers and third-party hosting services influences pricing strategies and service offerings, directly impacting supply availability and pricing structures.

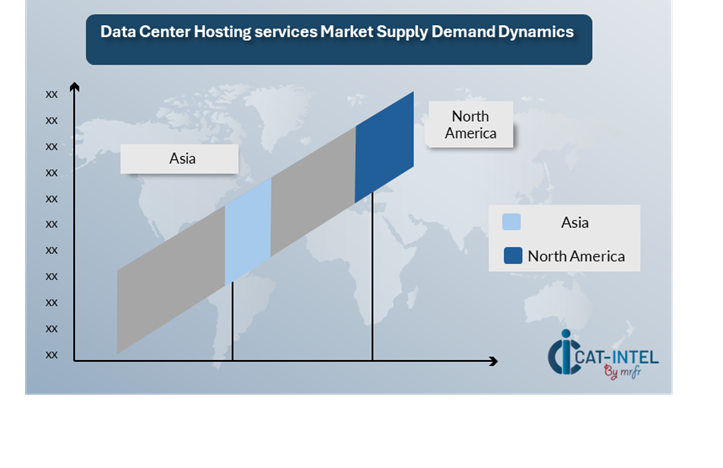

Regional Demand-Supply Outlook: Data Center Hosting Services Market

The image shows growing demand for data center hosting services in both North America and Asia, with potential price increases and increased competition.

North America: A Key Player in the Data Center Hosting Services Market North America, particularly the U.S., plays a pivotal role in the data center hosting services market, characterized by:

-

Leading Providers: Major players in the U.S., such as Amazon Web Services (AWS), Microsoft Azure, and Google Cloud, lead in data center infrastructure, driving the region's dominance in cloud services. -

Strong Cloud Demand: North America has seen a surge in cloud computing, driven by both enterprises and startups, resulting in a high demand for scalable, secure, and efficient data center hosting solutions. -

Innovation in Technology: Advanced data center technologies, including energy-efficient cooling solutions, automation, and AI-driven resource management, enable data centers to meet growing demand while reducing operational costs. -

Focus on Sustainability: Many U.S. data centers are adopting renewable energy sources and sustainable building practices, positioning the region as a leader in environmentally responsible data center management. -

Consumer Trends: The increasing adoption of data-intensive applications, including AI, IoT, and 5G, continues to drive demand for high-performance data centers, ensuring North America's competitive edge in global data hosting services.

North America remains a key hub for Data center hosting services market and its growth

Supplier Landscape: Supplier Negotiations and Strategies in the Data Center Hosting Services Market

The data center hosting services market has a diverse and extensive supplier landscape, comprising global and regional players that supply critical infrastructure and services essential for data center operations. Key suppliers provide various components such as server hardware, storage devices, networking equipment, cooling systems, and power solutions, all contributing to the efficiency, performance, and sustainability of data centers.

Currently, the supplier landscape is characterized by strong relationships between data center providers and suppliers of hardware, energy, and cooling technologies. These collaborations are crucial to maintaining the reliability, energy efficiency, and scalability of data center operations. In addition, suppliers of cloud services, security solutions, and software support the growing demand for data storage and processing, especially in cloud computing and data-intensive applications.

Some of the key suppliers in the data center hosting services market include:

- Dell Technologies

- Hewlett Packard Enterprise (HPE)

- Cisco Systems

- Schneider Electric

- Intel Corporation

- Equinix

- Amazon Web Services (AWS)

- Microsoft Azure

- Google Cloud

- Nvidia Corporation

Key Development: Procurement Category significant development

Market |

Procurement Category |

Significant Development |

Almond Market |

Raw Materials (Fertilizers, Pesticides, Irrigation Equipment) |

Increased focus on sustainable farming practices, adoption of precision agriculture to reduce water usage. |

Almond Market |

Packaging Materials |

Growing demand for eco-friendly and recyclable packaging solutions to meet consumer preferences. |

Almond Market |

Processing Machinery |

Innovations in processing equipment to improve yield, quality, and cost-efficiency, with a focus on automation. |

Data Center Hosting Services |

Server Hardware & Storage |

Integration of high-performance hardware like NVMe SSDs and next-gen GPUs to support data-intensive applications. |

Data Center Hosting Services |

Cooling Solutions |

Adoption of energy-efficient cooling technologies, including liquid cooling and AI-driven temperature control. |

Procurement Attribute/Metric |

Details |

Market Sizing |

The global data center hosting services market is projected to grow from USD 58.2 billion in 2023 to 103.4 billion by 2032, with a CAGR of 10.5% during the forecast period. |

Adoption of Cloud-Based Services |

Growing adoption of cloud computing, edge computing, and hybrid cloud solutions is driving demand for data center hosting services across various industries, especially in finance and healthcare. |

Top Strategies for 2024 |

Focus on energy-efficient data centers, expansion of cloud infrastructure, strategic partnerships, and enhanced security protocols to accommodate rising data processing needs. |

Automation in Data Center Operations |

Over 30% of data centers are implementing AI and automation tools for predictive maintenance, resource allocation, and improving energy efficiency. |

Procurement Challenges |

Key challenges include rising energy costs, supply chain disruptions for hardware, and the need for constant upgrades to meet growing demand for data processing. |

Key Suppliers |

Major players include Amazon Web Services (AWS), Microsoft Azure, Google Cloud, Equinix, and Digital Realty, focusing on high-performance and scalable hosting solutions. |

Key Regions Covered |

Key markets include North America, Europe, and Asia-Pacific, with significant demand from the U.S., Germany, and China. |

Market Drivers and Trends |

Growth is driven by increased adoption of cloud services, digital transformation across industries, the rise of IoT, and the growing need for scalable data storage and processing. |

Frequently Asked Questions (FAQ):

Frequently Asked Questions (FAQ):